Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Brazil’s industrial gas migration reaches 13.3 Mcmd as market liberalisation accelerates

Ceramics and steel sectors lead unprecedented industrial migration wave, with top three suppliers capturing 68% market share

1 minute read

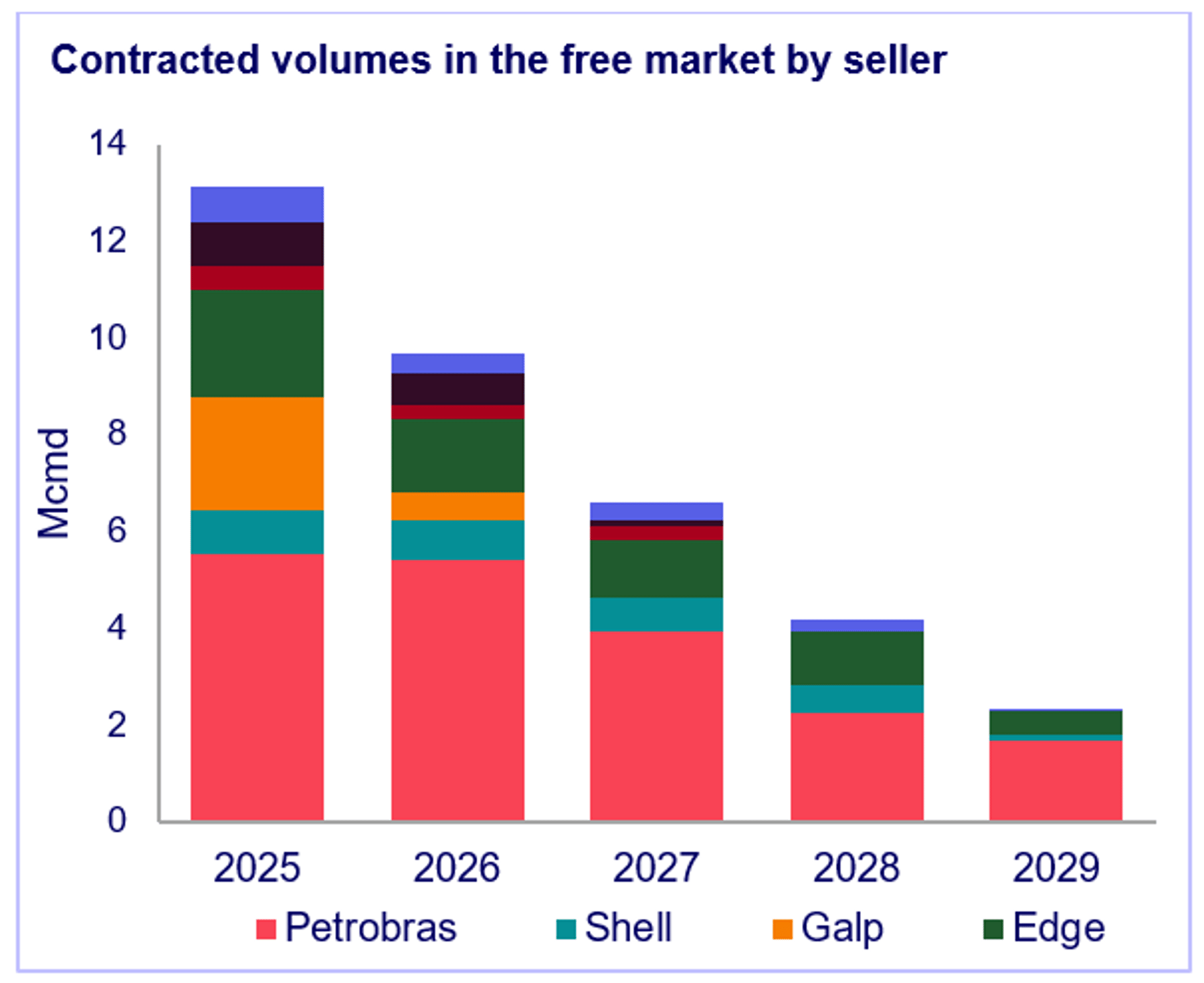

Brazil's free gas market has reached a milestone with 13.3 million cubic meters per day (Mcmd) migrating from traditional distribution channels through September 2025, driven by market liberalisation that is fundamentally reshaping the country's energy landscape, according to a recent report by Wood Mackenzie.

According to the report, “Still accelerating? Brazil's industrial free gas market pushes new boundaries”, the migration wave, which encompasses 68 industrial players, represents an unprecedented shift in Brazil's natural gas sector. Large industrial players account for over 8.7 Mcmd, highlighting significant concentration among major consumers.

“Brazil demonstrates how market liberalisation can catalyse rapid structural change," said Lucas Rego, gas analyst at Wood Mackenzie. "Migration gained significant traction in Q4 2024 and Q1 2025, when the largest industrial consumers began their transition. Volumes surged dramatically during this period before settling into a steady rhythm of approximately 0.6 Mcmd per month."

{kind=link}

The ceramics sector has emerged as the migration leader, representing 40% of all companies that have transitioned to the free gas market and commanding 3.3 Mcmd of demand. The steel sector matches this volume at 3.3 Mcmd. Together, these two industries account for half of all volumes migrated from Local Distribution Companies (LDCs) to the free market.

Three dominant players have defined the competitive landscape. Petrobras leads with 25 contracts strategically targeting large industrial clients. Galp has captured 21 contracts with a focus on small and medium-sized companies. Edge has positioned itself with a balanced portfolio of 18 contracts across different consumer segments. Together, these three suppliers command 67% of the market share.

Regional dynamics reveal stark disparities in market penetration. The Southeast region has captured 89% of free-market volumes migrating from LDCs, cementing its position as the primary battleground for supplier competition. Industry observers expect the South region to become the next strategic focus for suppliers. The Northeast presents higher barriers to entry due to structurally more competitive price levels.

"With most contracts currently running up to three years and customer migration continuing, supplier competition is poised to intensify significantly," Rego added. "This is still a maturing market, and we expect to see increasingly sophisticated strategies as suppliers vie for long-term customer relationships."

The analysis highlights a notable concentration pattern: while most contracts fall within the range of up to 0.1 Mcmd, these smaller agreements represent only a fraction of the total 13.3 Mcmd free market volume. This underscores that large industrial consumers are the primary drivers of market transformation. The breadth of participation expands across diverse sectors, including construction, mining, refining, fertilisers, paper, chemicals, and glass manufacturing.