Is Japan’s grid-scale storage market getting a move on?

Market restructuring is required to balance the books in Japan. Could new ancillary and capacity services close the viability gap?

3 minute read

With strong ambitions towards the energy transition and a liberalised power market structure, Japan is one of the most promising markets for grid-scale storage in Asia Pacific. The country’s electricity consumption per capita is twice the Asia Pacific average, and there is a race to keep up.

A grid expansion master plan was announced in March 2023 at an estimated cost of ¥6 to ¥7 trillion (US$45 billion to US$55 billion) by 2050, and peak load will be largely managed by solar and wind power in the coming decades. Confidence in nuclear power is returning after 2011’s Fukushima, with coil, oil and LNG are expected to dip as a result.

With multiple revenue streams to support renewables, and an extremely high demand for electricity, it’s perhaps unsurprising that the country is now investing more seriously in energy storage. Japan’s planned grid-scale battery storage system (BESS) will also need multiple revenue streams to remain viable, however, and a series of market reforms have been designed to sustain it.

Drawing on data from our Global Energy Data Hub, our research takes a detailed look at Japan’s grid-scale storage market reform. Fill in the form on the right to download an extract from the report and learn about the country’s power market cost dynamics and pricing, supply and demand patterns, emissions, market structure and more. Read on for a summary.

The limits of energy arbitrage

Japan Electric Power Exchange (JEPX) is one of the most mature wholesale energy markets in APAC, operational since 2005. More than 40% of the country’s total electricity demand is executed through this spot market, which incentivises low cost use by placing a time-of-day usage value on electricity. This makes it worthwhile to charge grid batteries during periods of low prices, and discharge at peak times when demand, and subsequently prices, are higher. This process enables batteries to earn revenue through energy arbitrage.

The amount of revenue possible for the wholesale market is dependent on intraday prices, and these have been extremely volatile in Japan over the last few years thanks to limited supply and high fuel prices. In the first quarter of 2021, prices rose to unprecedented highs due to a tight LNG supply, during cold weather conditions. From the third quarter of 2021 to the last quarter of 2022, power prices again hit record peaks, this time due to the global inflation of fuel prices. Looking ahead to 2032, we expect a lot of uncertainty in energy arbitrage revenues. It will be essential to engage in ancillary services and explore the capacity market, to bridge the revenue gap and meet the return on investment targets.

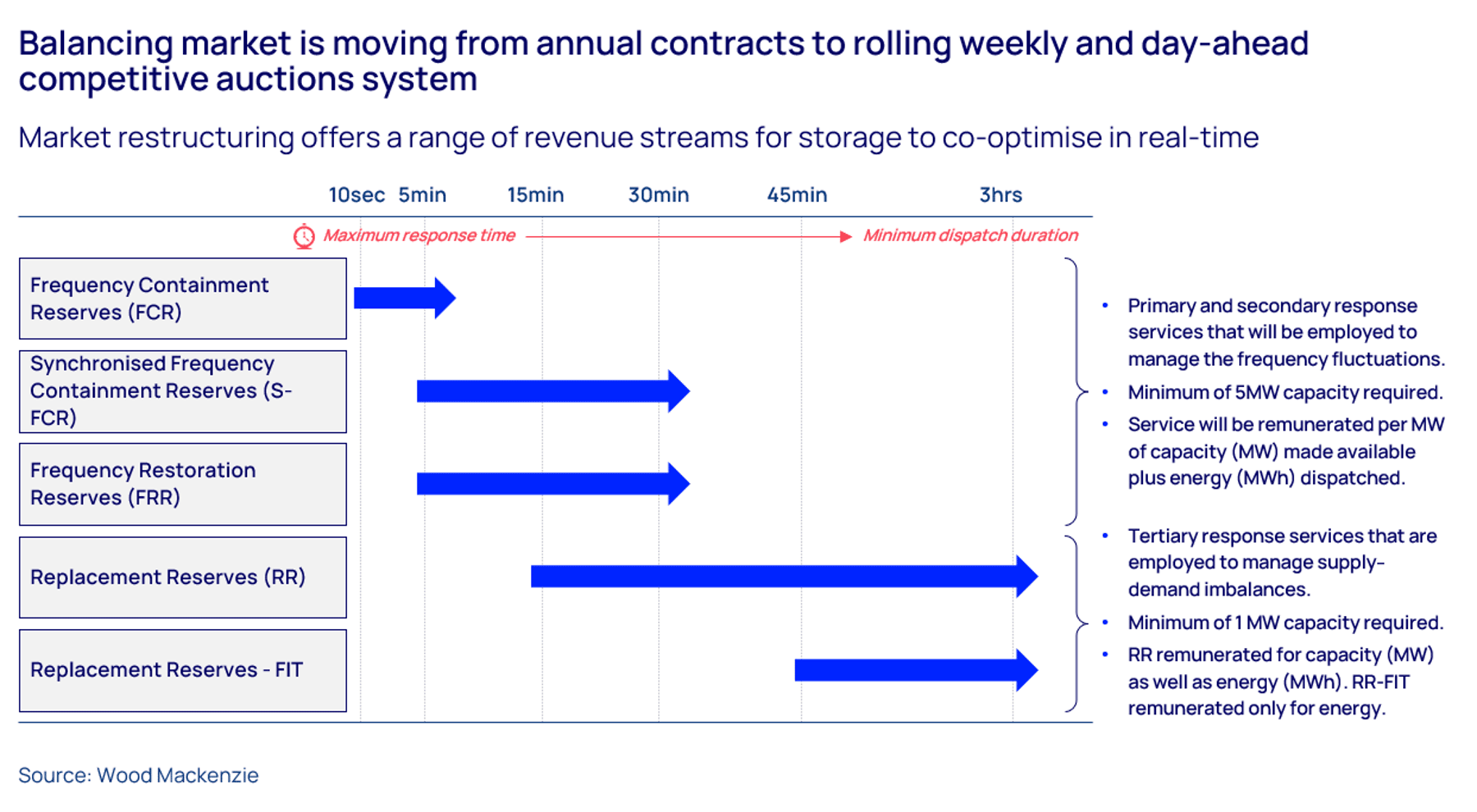

Balancing the market with new revenue streams

A range of revenue streams for storage should allow frequency fluctuations to be managed more effectively. These products are intended to incentivise fast dispatch and absorption of power, a key capability differentiating batteries from traditional generators.

New ancillary services markets are set to launch in 2024, with rolling weekly and day-ahead markets offering additional revenue streams for storage. A new, low carbon capacity market will allow battery storage of three hours to participate in auctions scheduled in 2023 and 2024 for delivery in 2027 or sooner. The hope is that these capacity contracts should reduce merchant risk and improve bankability.

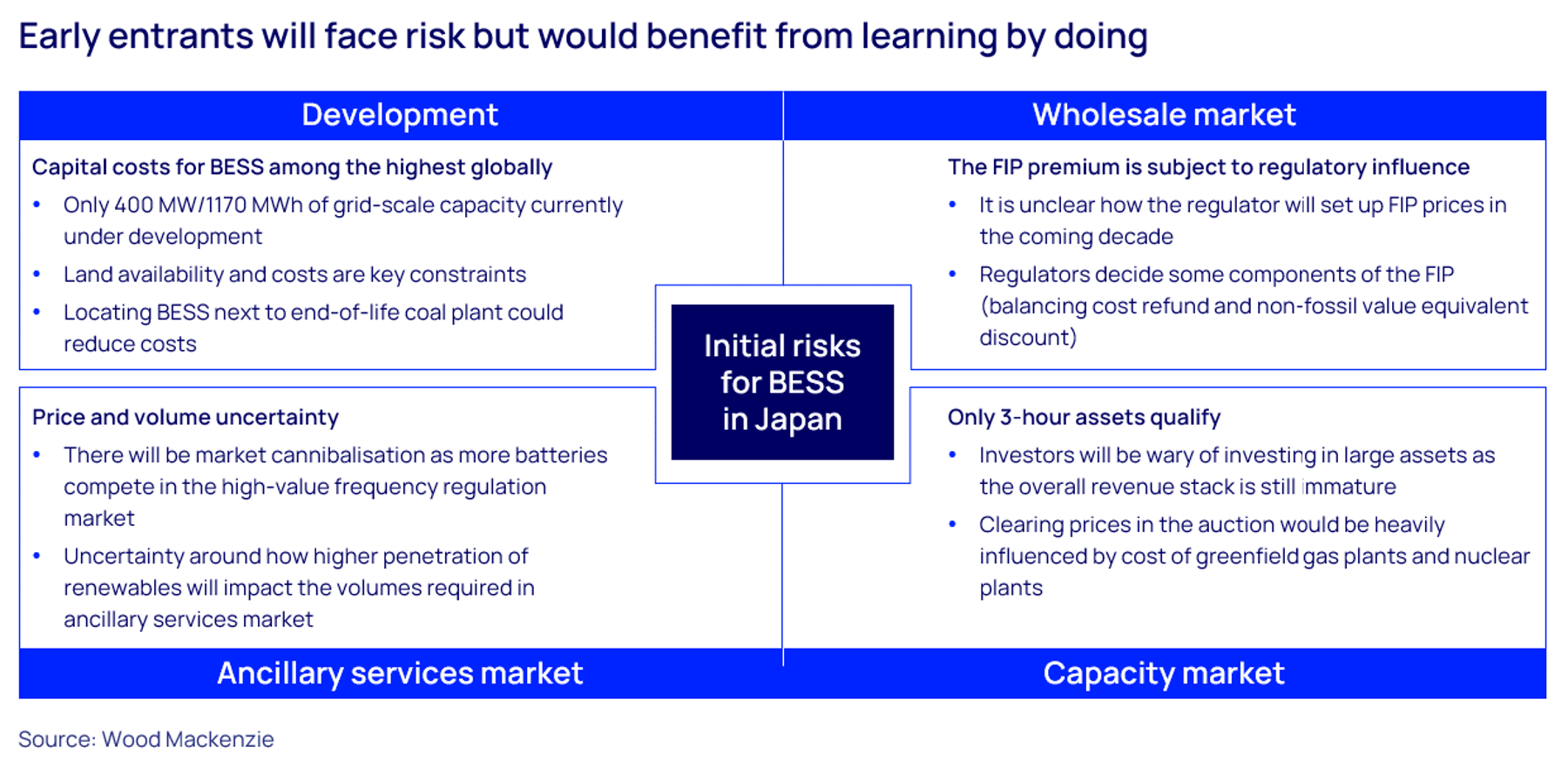

Risks and uncertainties

{kind=link}

{kind=link}

Each market category still suffers some uncertainty around regulations, long-term prices and volumes, with particular impact on early entrants. For example, the ancillary services market could see volumes and price cannibalisation, as more batteries enter the market, shrinking the most valuable revenue stream in the long term.

There are several risks in the wholesale market, too. The FIP premium is subject to regulatory influence, and it is still unclear how the regulator will set up FIP prices in the coming decade.

Additionally, the capacity market is currently limited to 3-hour assets, and the overall revenue stack’s immaturity may make investors wary of buying into large assets.

Learn more

Learn more about developments in Japan’s grid-scale storage market by filling out the form at the top of the page. You’ll also get access to our charts tracking energy arbitrage and more.