Turn of the tide? What the entry of Chinese polysilicon to the US means for the American solar supply chain

The US Customs Borders and Protection (CBP)’s release of Astronergy’s modules containing non-Xinjiang Chinese polysilicon will drastically change supply/demand dynamics in the near-term

5 minute read

Sylvia Leyva Martinez

Director, North America Utility-Scale Solar and Host of Interchange Recharged podcast

Sylvia Leyva Martinez

Director, North America Utility-Scale Solar and Host of Interchange Recharged podcast

Sylvia researches market dynamics, business models, market developments and financial strategies of solar PV projects

Latest articles by Sylvia

-

Opinion

As racks scale, power must change

-

Opinion

Six months of data centre reality, from Bragawatts to behind-the-meter

-

Opinion

How are key renewable energies faring at the end of 2025?

-

Opinion

Will energy storage save the grid?

-

Opinion

From capture to storage: inside the full CCUS value chain

-

Opinion

From policy to possibility: How CCUS Is moving from talk to action

Elissa Pierce

Research Analyst, Solar Module Technology and Markets

Elissa Pierce

Research Analyst, Solar Module Technology and Markets

Elissa's research includes solar module markets, technologies and supply chains across the globe.

Latest articles by Elissa

-

Opinion

The state of safe harboring: a strategic outlook for US utility-scale solar development

-

Opinion

RE+ 2024: Our 7 biggest takeaways

-

Opinion

RE+ 2024: Our 7 biggest takeaways

-

Opinion

Turn of the tide? What the entry of Chinese polysilicon to the US means for the American solar supply chain

CBP finally releases solar modules made with non-Xinjiang Chinese polysilicon into the US

Astronergy has confirmed that CBP released a small number of containers with solar modules made with non-Xinjiang Chinese polysilicon into the US last month. It is believed that the raw materials for the polysilicon also came from China. This is a significant turn of events. Since enforcement of the Uyghur Forced Labor Prevention Act (UFLPA) began in mid-2022, CBP has only released modules made with European, US, and Southeast Asian polysilicon from Hemlock, Wacker Chemie, and OCI. Allowing modules made with Chinese polysilicon to be imported into the US has the potential to greatly increase module supply.

The solar supply chain in the US is dramatically different to global dynamics. To understand the relevance of Astronergy’s shipment release, it is required to understand the context specific to the US solar market.

What role does China play in the global solar supply chain?

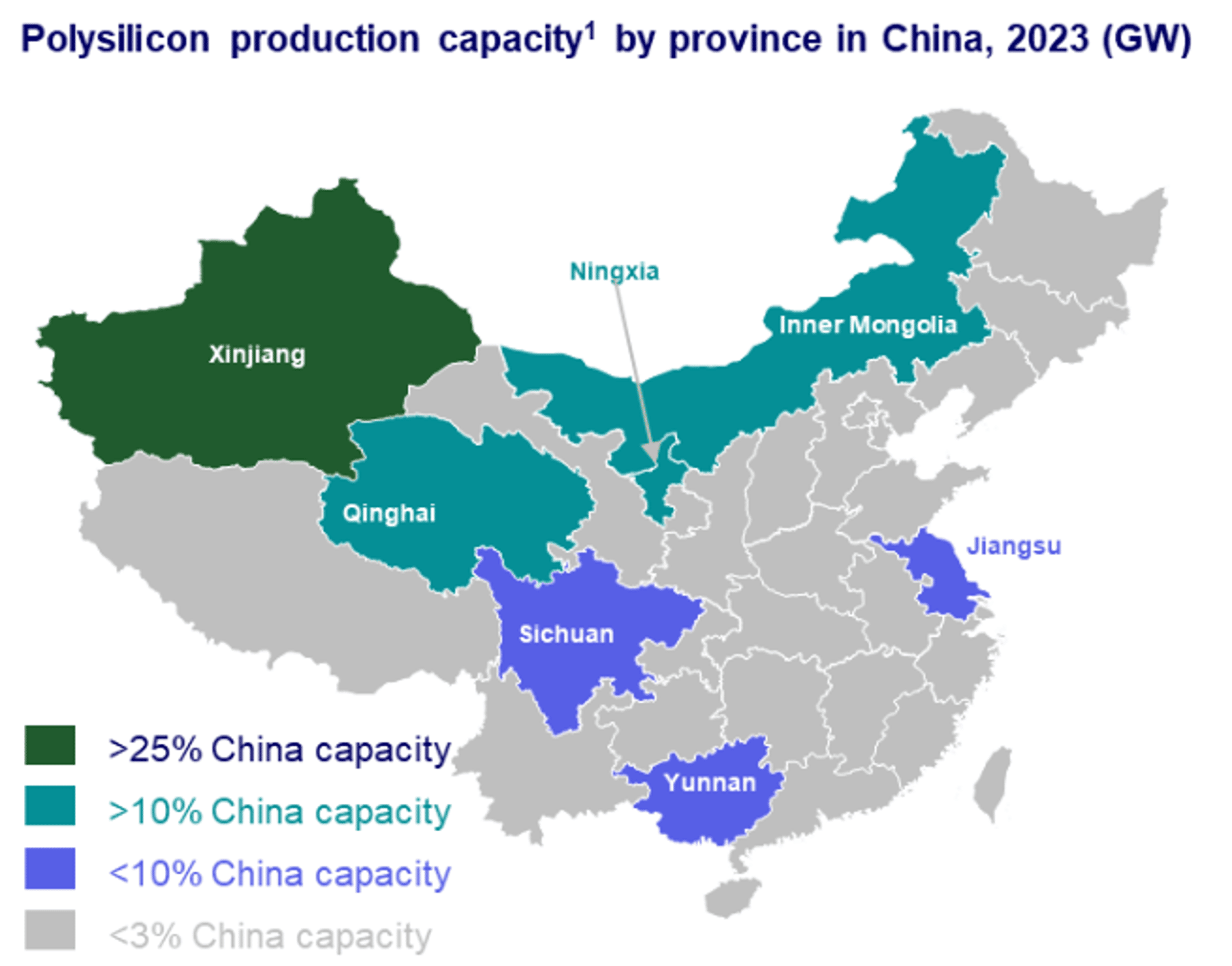

China dominates solar manufacturing across the value chain. While domestic wafer, cell, and module production capacity are expanding in the US and other countries, there are few plans for new polysilicon factories outside of China. Polysilicon production is extremely energy-intensive and creates hazardous waste, so manufacturers who wish to build such a factory in the US face long development timelines and high capital expenditures.

China is unique in that strong government incentives and low energy costs have facilitated the growth of the polysilicon industry. Thus, the country now accounts for 85% of the world’s 1,177 GW of polysilicon capacity, and this domination will increase further over the next few years. The rest of the world’s share of polysilicon capacity will shrink from 15% in 2023 to 12% by 2026, and much of this capacity is dedicated to the electronics industry rather than solar.

{kind=link}

When the UFLPA became effective in mid-2022, 57% of Chinese polysilicon was made in Xinjiang. However, following allegations of forced labor in that region, production rapidly shifted to other parts of the country, particularly to Ningxia and Inner Mongolia. In 2023, only 27% of Chinese polysilicon was produced in Xinjiang.

What prevented Chinese polysilicon from entering the US?

Policies aimed at preventing the importation of goods potentially made with forced labor have prevented solar modules made with Chinese polysilicon from entering the US. This began in 2021 when the US Department of Commerce issued a Withhold Release Order (WRO) against Hoshine Silicon Industry Co. (HSI). The order banned any silica-based products from HSI in all raw materials, intermediate goods, and finished goods imported to the US.

In 2022, the implementation of the UFLPA expanded the scope of the WRO to all goods with ties to the Xinjiang region, as it presumes all goods from this region are made with forced labor unless proven otherwise.

The Hoshine WRO and UFLPA severely limited the modules and cells that could enter the US, as the vast majority of these components used polysilicon from Xinjiang. Soon after the passage of the UFLPA, CBP started detaining module shipments.

Manufacturers then faced the complex tasks of modifying their polysilicon procurement strategy and proving polysilicon and quartzite traceability. Modules with European polysilicon were the first to clear customs successfully, but the road has been more complex for modules containing non-Xinjiang Chinese polysilicon.

Why is the entry of modules with Chinese polysilicon relevant to the US solar industry?

The news of the Astronergy shipment passing through customs is notable because it could result in cheaper pricing for US solar modules. Trade sanctions aside, one of the main factors driving higher module prices for the US since mid-2022 is the low availability of modules made with non-Chinese polysilicon. The UFLPA and various other trade policy measures have prevented the nation from leveraging the low solar component prices observed globally.

Non-Chinese polysilicon is priced $7-10 US$/kg higher than Chinese polysilicon, equivalent to double the price. While it is only one shipment, the release of these Astronergy modules bodes well for future shipments of modules containing non-Xinjiang Chinese polysilicon. Assuming that more shipments of these types of modules start entering the country, the US will have access to a greater supply of modules made with cheaper polysilicon. Using Chinese polysilicon would decrease module manufacturing costs by $0.02-$0.04 US$/W, a 10-20% decrease. If cost savings are directly passed on to customers in final prices, some delivered Tier 1 modules from Southeast Asia could fall below the $0.30 US$/W threshold soon.

How will US solar manufacturers be able to compete with imports?

It’s too early to tell whether the release of the Astronergy’s shipment will result in a steady influx of Chinese polysilicon in the US. However, if more Chinese polysilicon were to enter the country, the growing US manufacturing base would need to find ways to adapt to the potential arrival of cheaper imports.

Companies could increase their cost competitiveness by sourcing components with low-cost Chinese polysilicon. However, a few different layers of tariffs apply to Chinese components. Section 301 tariffs still apply to Chinese wafers and cells. Additionally, cells made with Chinese wafers in Cambodia, Malaysia, Thailand, and Vietnam will be subject to anti-dumping and countervailing duties from June 2024 onwards, unless suppliers are able to certify that they are not circumventing the orders. Therefore, manufacturers unable to procure non-Chinese wafers (by themselves or within cells) will have limited ability to reduce costs, even if the wafers and cells use Chinese polysilicon. Only a few companies can produce wafers outside of China and they typically use these in their own downstream products. These manufacturers will likely be able to produce the most cost-competitive domestic modules.

Other manufacturers will remain dedicated to using a non-Chinese supply chain to the extent possible, including using non-Chinese polysilicon. These suppliers are positioning themselves as the most reliable rather than the lowest-cost suppliers. These companies will have to educate customers that mitigating trade policy risk vastly exceeds the cost premium associated with sourcing domestically.

Follow supply chain trends

To learn more about global solar module supply-demand dynamics and pricing, subscribe to our Solar Module Supply Chain Service.

Our detailed coverage of the global solar supply chain can help guide your investment decisions and corporate strategy, while helping you identify the primary drivers that are influencing trade and price dynamics.