Can the EU and US hit EV targets amid supply chain shake up?

We examine whether both markets can meet their production and sales targets for electric vehicles while de-risking supply chains

4 minute read

With the introduction of new legislation in both the EU and the US — the Critical Raw Materials Act (EU) and the Inflation Reduction Act (US) — both regions are taking big steps to improve supply chain security and resilience. But with electric vehicle sales falling short, our electric vehicle and battery supply chain service explores if either market can realistically achieve its targets.

We’ve detailed our key findings in this article, but to download the full slide deck and watch the webinar replay, fill out the form at the top of the page.

A landscape for growth?

The EV transportation sector is driven almost entirely by policy, with the stringency of these policies being a critical factor for EV adoption and supply chain resilience. In the US, consumer tax credits are currently the primary driver of EV adoption. However, the long-term growth of this market will depend heavily on the rigour of federal emission norms, such as the EPA Tailpipe Emission Standard and the NHTSA Fuel Economy Standard.

Tax credits like the Clean Vehicle Credit and Domestic Manufacturing Conversion Grants are essential to bridging the cost gap. The availability of these credits will determine EV sales until manufacturing costs decrease enough to balance production expenses and profit margins. Similarly, in the EU, tax incentives such as road tax and registration exemptions play a crucial role in enhancing the affordability of EV ownership.

In both regions, supply chain security is a critical focal area for policy. The US is laser-focused on reducing its dependence on countries like China, which dominate the market for certain critical materials. The Minerals Security Partnership (MSP) is one of the initiatives aimed at securing collaborative investments in critical mineral projects. The EU’s approach is to forge strategic partnerships with other nations to diversify its supply chain and ensure EU companies have access to vital battery minerals by easing investment rules.

Despite these proactive measures, challenges remain. Strategic partnerships and new trade agreements are promising steps toward reducing dependence on China, yet it's unlikely that EV sales in either region will hit post-2030 emissions reduction targets. Pricing issues, consumer acceptance, inadequate charging infrastructure, and mineral supply constraints are problems that could limit actual sales.

Balancing consumer demands with commercial viability

Since 2010 the automotive market has experienced a significant shift to SUV vehicle segments that has been driven by a growing consumer preference for these vehicles. Leading automakers in the three major automotive regions of China, Europe, North America now face the challenges of meeting the required emissions reduction targets and electrification rates.

The trend towards plug-in EVs is seen across the overall automotive market, but while battery pack sizes for SUVs and A-F segments overlap, SUVs are generally less energy efficient. As a consequence for the preference for SUVs there’s growing demand for bigger batteries.

The repercussions of these trends means the EU and US will have to rely heavily on international allies to address a looming shortfall in battery raw material supply. China has a high concentration of battery supply chain capacity and market share but with the Critical Raw Materials Act and the Inflation Reduction Act focusing on decoupling with China, both regions will depend on ‘friendly’ imports from other countries owing to the lack of domestic extraction and processing capacity in both regions.

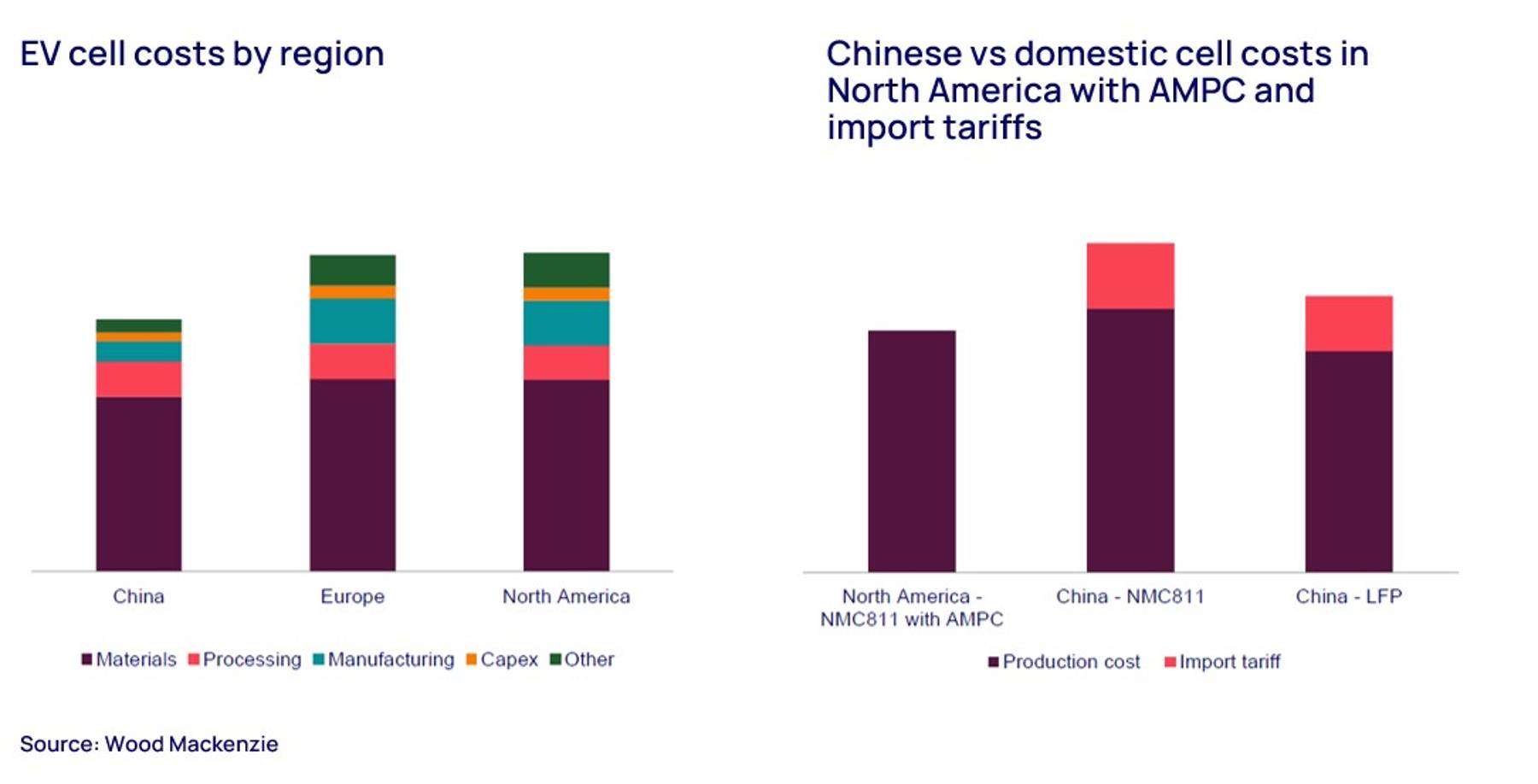

Are selective battery supply chains robust enough?

Higher average manufacturing costs in the EU and the US present significant challenges for domestic manufacturers seeking to scale up their operations rapidly. Several key factors contribute to these elevated costs.

In the EU, specialised labour expenses have an impact on driving up overall manufacturing costs. To address this, the US has implemented strategic measures in the form of its Advanced Manufacturing Production Credit (AMPC) to provide incentive to domestic manufacturing and have placed tariffs on Chinese cells to lower costs.

{kind=link}

Decarbonising road transport

So, can the EU and US decarbonise by 2035 and achieve their targets? Non-battery powertrains are feasible, transitional solutions to decarbonise road transport but are difficult to commercialise in the time available. Both regions are showing support for alternative vehicles but the technology capabilities vary widely. For example, fuel cell electric vehicles (FCEVs) at present are too expensive and lack suitable access to infrastructure, but they have good range and carbon offset potential. Biodiesel (B-20) vehicles are more cost effective and already have a manufacturing maturity but lack the same access to infrastructure.

Automakers are seeing the potential of alternatives with GMC and Chevrolet already underway with the deployment of B-20 vehicles. However to fully decarbonise heavy duty transportation, automakers in both regions might need to wait until 2035.

Learn more

If you would like to download the full slide deck and watch the webinar this article summarises, fill out the form at the top of the page.