Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

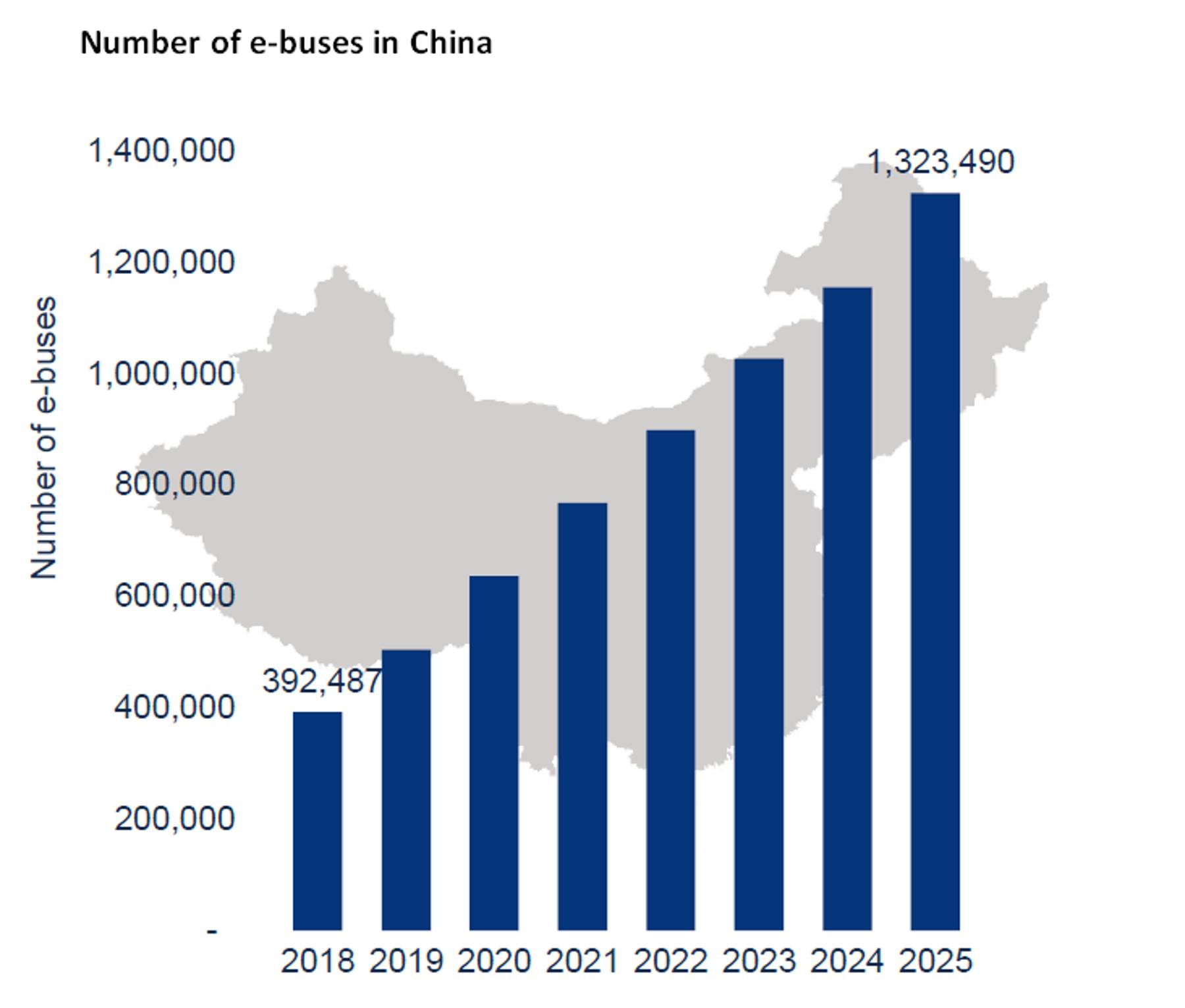

Fuelled by public policy and declining battery costs, global electric bus adoption is set to triple by 2025. The Chinese market - the most promising in this sector - will surpass the 1 million e-bus mark by 2023 and reach 1.3 million by 2025, according to new research from Wood Mackenzie.

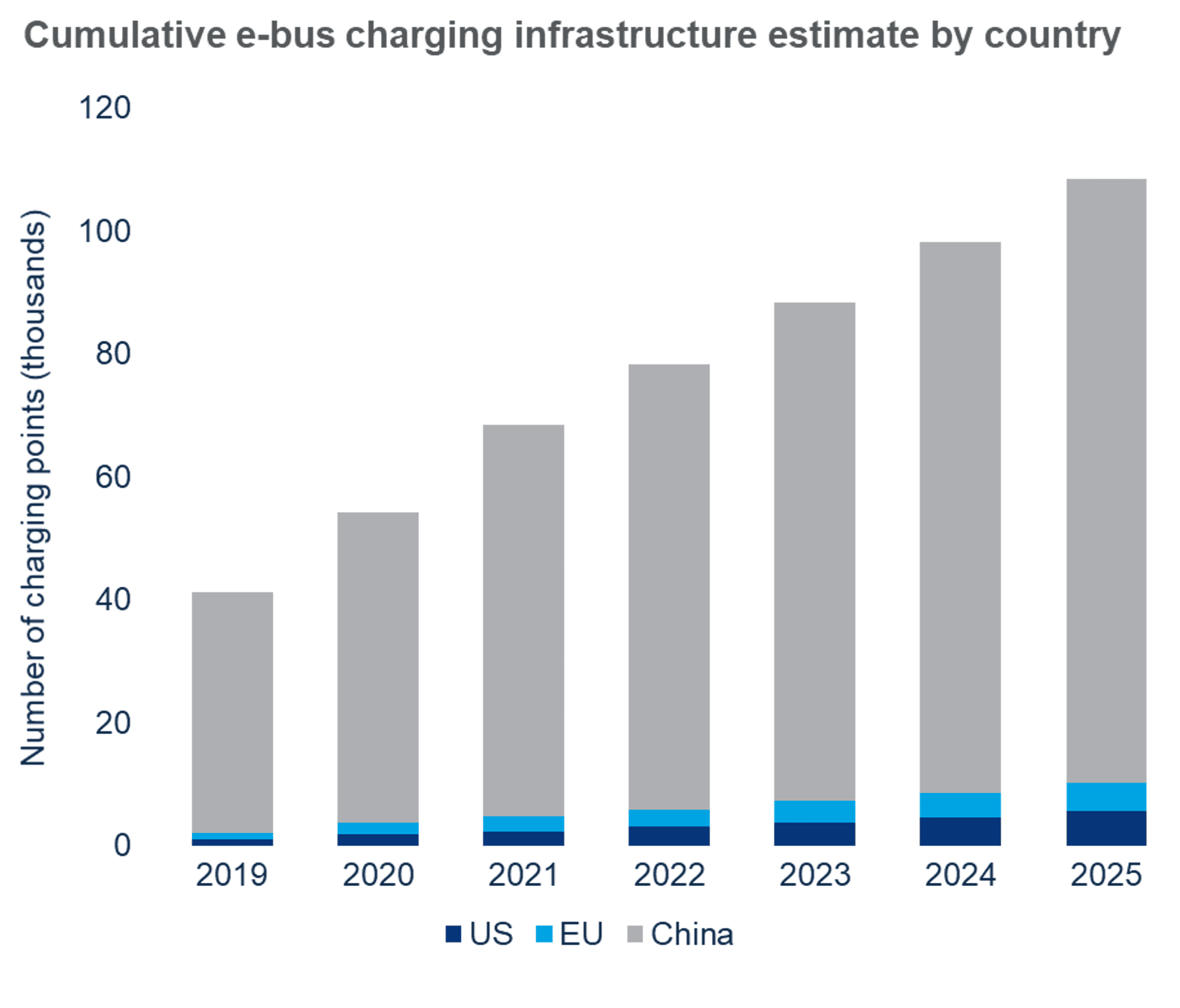

China dominates the heavy-duty electric vehicle (EV) segment, accounting for 98% of the global e-bus market through 2018. To support this high concentration of e-buses, a total of more than 50,000 e-bus charging points will be installed by the end of 2019. This figure is set to more than double by the end of 2025.

Timotej Gavrilovic, Wood Mackenzie Contributing Research Analyst, said: "In 2018, 23% of bus purchases in China were electric. Overall bus purchases in the country are expected to remain stable, with 420,000 new purchases by 2025. Electric bus purchases are expected to increase along with further market growth and continuing government support, reaching 40% of new bus purchases globally in 2040.”

US and Europe e-bus markets to see growth post-2025

According to the Wood Mackenzie report, a combined 40,000 electric heavy-duty vehicles will be on the roads in the US and Europe by 2025. The current market will expand to 7,300 e-buses by the end of 2019, representing pilot schemes across both regions that will add up to nearly $6 billion in market value.

“Most transit and school bus operators are still wary of e-buses as a new technology and will continue testing the equipment prior to investing in scaling current deployments. However, government and transit agencies have clean transportation targets that should accelerate growth beyond 2025. Long-haul e-buses are not expected to enter the market before 2023 and will likely be limited to 1% of new sales through 2025. European e-bus growth is driven by urban bus deployments, while the US market is driven by transit and school e-buses.

"Government, school bus operators and transit agencies are not the only organisations impacting and influencing electrification. US and European utilities are beginning to examine new models to support clustered charging at depots and encourage operators to manage charging for the benefit of the grid. Dominion Virginia Power offered the most aggressive proposal yet, to develop the charging infrastructure and pay the cost difference between a diesel bus and an electric bus for 100% of all diesel bus replacements in their service territory by 2030, ” added Mr. Gavrilovic.

Charging infrastructure deployment limited in US and Europe

The deployment of e-bus charging infrastructure has already started to surge in China. However, growth in the US and Europe is limited by the size of existing pilots – where one to five charging points are typically enough to support several buses. Despite this, the total number of charging points for all three regions will more than double to a total of 108,000 charging points by 2025.

“Over 68,000 depot chargers will be installed globally from 2019 to 2025 to meet EV bus charging demand, with more than 9,000 located in Europe and the US. Following larger deployments of e-buses beyond 2025, and potential synergies with e-truck and e-fleet charging, a higher e-bus-to-EVSE ratio can be expected. This would lead to a slower rate of growth for infrastructure in relation to bus demand.

{kind=link}

{kind=link}

“Our forecast assumes all e-bus chargers are depot chargers. In practice this is not always the case, as on-route charging will represent a fraction of the chargers deployed. On-route charging will most commonly be used in intracity transit applications, as their routes are pre-determined. A higher percentage of on-route chargers will increase the number of charging points deployed per bus and lower the battery size required for buses to operate,” added Mr. Gavrilovic.