Energy transition outlook: Asia Pacific

With its scale, diversity, and rapid change, Asia Pacific is driving the future of global energy markets

2 minute read

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash Sharma

Vice President, Head of Scenarios and Technologies

Prakash leads a team of analysts designing research for the energy transition.

Latest articles by Prakash

-

The Edge

Will falling populations reshape energy demand?

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

Energy transition outlook: Middle East

Roshna N

Research Analyst, Energy Transition

Roshna N

Research Analyst, Energy Transition

Roshna N specialises in integrated energy and emission models for Asia-Pacific and African markets.

Latest articles by Roshna

-

Opinion

How is energy transition investment evolving in 2026?

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Africa

-

Opinion

What are the energy transition technologies to watch in 2025?

-

Opinion

Energy transition outlook: Africa

-

The Edge

How the world gets onto a 1.5 °C pathway

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom works on scenario modelling for country and global-level energy mixes across all major energy commodities

Latest articles by Jom

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Middle East

-

Opinion

Energy evolution: navigating the path to a sustainable future

Tan Jun Yeang

Research Analyst, Scenarios & Technologies

Tan Jun Yeang

Research Analyst, Scenarios & Technologies

Latest articles by Tan Jun

View Tan Jun Yeang's full profileAsia Pacific faces an energy transition that will define global climate outcomes. Home to more than half the world’s population and over one-third of global GDP, the region must power unprecedented economic growth while decarbonising at speed and scale. Will the region reconcile these competing demands fast enough to meet global climate goals?

Our energy transition outlook (ETO), part of our Energy Transition Service, maps four different routes through the global energy transition with increasing levels of ambition. And our regional updates delve into the detail at country-level. The Asia Pacific report considers pathways for nine major markets: Australia, China, India, Indonesia, Japan, South Korea, Malaysia, Thailand and Vietnam.

You can access a complimentary extract from the Asia Pacific 2026 update by filling in the form at the top of this page. Read on for an introduction to some of the key themes.

A tale of two trajectories

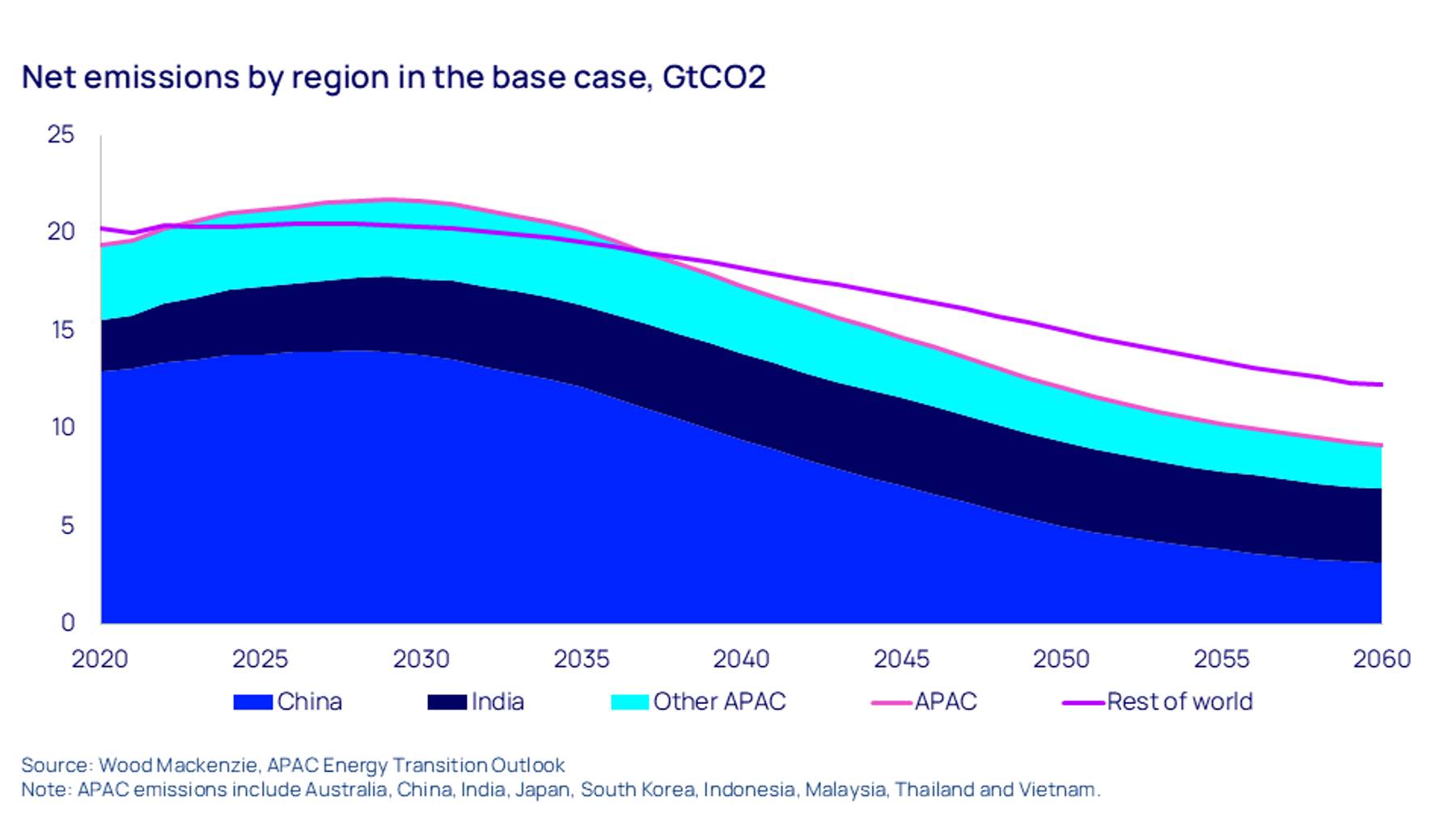

Rising demand makes Asia Pacific the world’s largest carbon-emitting region today, accounting for more than half of global emissions in 2025. Emissions are expected to peak in the late 2020s, later than in other regions, before declining at a pace that ultimately outstrips global averages. China’s leadership and APAC’s energy dominance will shape global climate outcomes, while government policies increasingly focus inward on domestic energy, materials, and security. Tariffs and geopolitical shifts are reshaping clean energy supply chains, gradually easing China’s dominance as other markets gain ground.

{kind=link}

By the late 2030s, regional emissions fall below those of other major regions, with the gap widening thereafter. China drives much of this shift, though its share of regional emissions declines from around 60% today to 40% by 2060. Developed economies including Japan, South Korea, and Australia cut emissions by more than half, while emerging markets such as India, Indonesia, and Vietnam continue to see growth as demand rises.

The power and industrial sectors, which together account for 78% of Asia Pacific’s emissions, follow diverging paths. Electricity generation cuts emissions by more than two-thirds by 2060, driven by domestic capacity growth and regional collaboration as renewables scale rapidly. In contrast, hard-to-abate industries such as steel and cement achieve only limited reductions, highlighting the challenge of deep industrial decarbonisation.

Yet the region presents enormous opportunities. Transition investments could reach US$54–72 trillion through 2060, driven by emerging technologies, infrastructure expansion, and new manufacturing hubs across batteries, hydrogen, solar, and critical minerals. Achieving deeper decarbonisation will require stronger policy support and carbon prices up to 1.7 times higher than the base case.

Power supply expands faster than decarbonisation

Asia Pacific now drives more than half of global power demand, fueled by population growth, industrialisation, and rising incomes. Demand is surging faster here than anywhere else, prompting countries to deploy every available technology — from coal and gas to nuclear and renewables — while keeping the lights on for more people with higher energy needs.

China already leads global renewable capacity, and India is accelerating solar and wind installations. Yet fossil fuels remain critical for system reliability, with coal and gas continuing to underpin the system as new capacity comes online in several major economies.

The result is a complex power mix. Renewables are scaling rapidly, but traditional sources remain essential to meet growing demand. These dynamics illustrate why the choices made now will shape Asia Pacific’s energy future for decades to come.

Get a closer look at APAC’s energy transition scenarios

Looking ahead to 2060, Asia Pacific’s energy transition could follow multiple pathways, from current policies to ambitious net zero commitments or delayed progress. How countries navigate these choices will shape not only regional energy systems but also global climate outcomes.

The full APAC Energy Transition Outlook extends this analysis, covering multiple scenarios and exploring key themes in depth:

- Energy security and independence as dominant priorities

- Diversification in clean-tech manufacturing as China’s lead narrows

- The decisive role of capital flows in determining the pace of the transition

- The widening gap between power supply growth and decarbonisation

Fill in the form at the top of the page to access your complimentary extract.