China’s gas demand growth returns and still holds vast LNG import potential

Flexibility is being built into the gas supply chain, having far-reaching implications for the global LNG industry

2 minute read

Miaoru Huang

Research Director, Asia Pacific Gas and LNG

Miaoru Huang

Research Director, Asia Pacific Gas and LNG

Miaoru leads our Northeast Asia gas research.

Latest articles by Miaoru

-

Opinion

Asia Pacific gas & LNG: 5 things to look for in 2026

-

Opinion

China LNG: eyes on the prize for global players

-

Opinion

How Asia will drive global gas and LNG investment to 2050

-

Opinion

Asia Pacific gas & LNG: 5 things to look for in 2025

-

Opinion

Gas & LNG in Asia: the next 10 years

-

The Edge

Getting China back on track

Last year, all sectors of China’s energy market felt the impact of the pandemic, but none more so than LNG. Chinese LNG demand took a hit, with imports down by almost 20% year-on-year. Record LNG prices, economic slowdown and domestic coal supply growth went a long way to keeping Europe’s lights over winter.

Economic activites are recovering

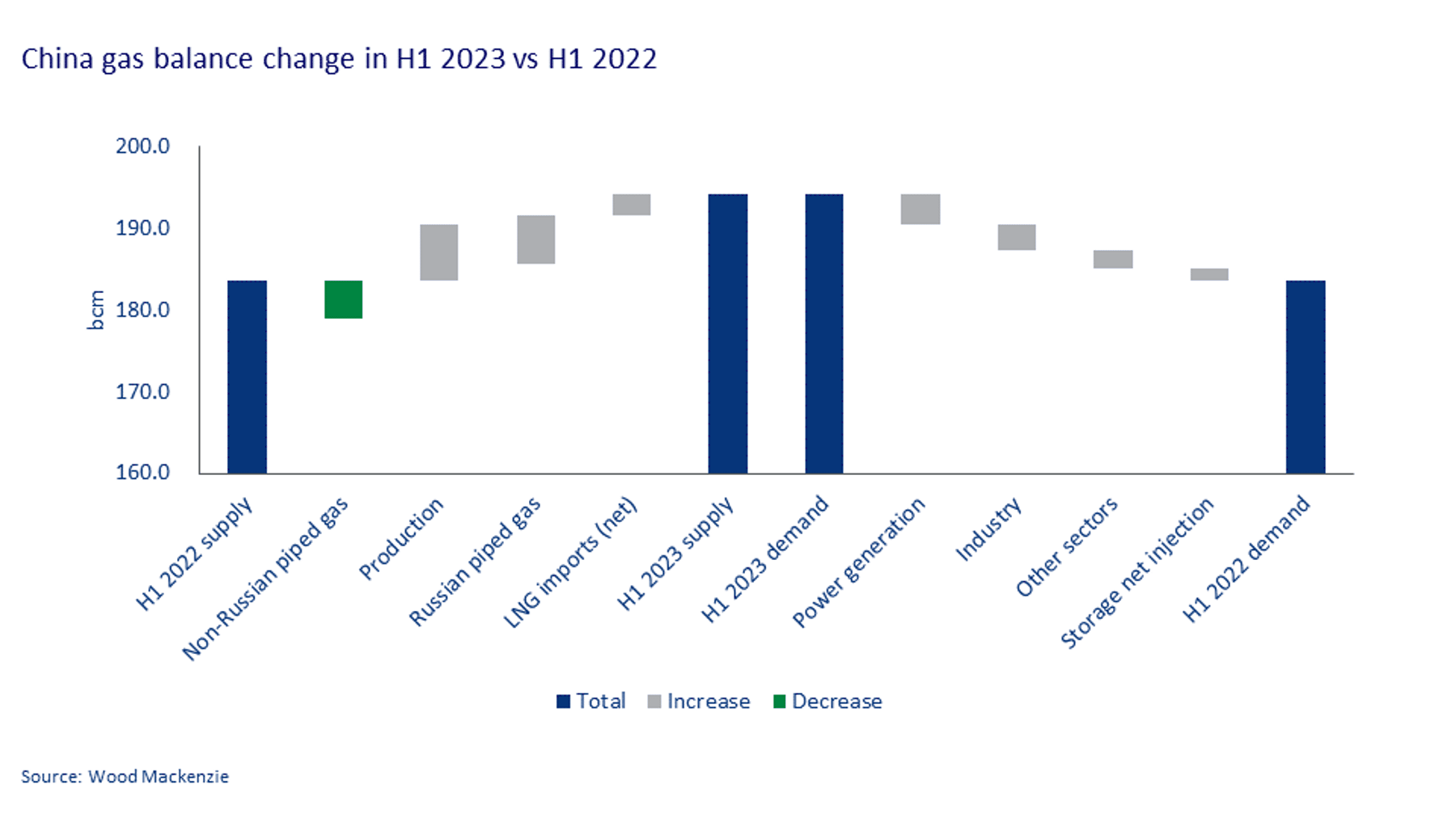

Since China reopened its borders in early January, economic activities are recovering, which supports a recovery in energy demand. Gas demand grew by 5% year-on-year in the first half of 2023, primarily contributed by the power sector and then industrial sector. China added around 10 GW of new gas-fired capacity in the past 12 months. Gas power played a key role in meeting peak power demand during summer heat waves and compensating shortfalls in hydropower output.

While gas production continues the growth momentum and Russian pipeline gas ramps up, LNG net imports in H1 2023 managed to reach 33 Mt, up by 6%, or 2 Mt more compared with imports in H1 2022. Such a pace of growth is not comparable to the boom seen between 2017 and 2021. But put into current global market context, China remains a key source of global LNG demand.

Despite short-term challenges to demand recovery, we expect Chinese LNG imports could reach over 120 mmtpa by the mid-2030s. Both upside and downside risks exist though. On the demand side, coal is the backstop of energy security; China aims to peak and start reducing coal consumptions from the next five-year plan period (2026-2030). How fast coal demand can be slashed, and net-zero fuels can be ramped up, will dictate gas demand creation. On the supply side, the scale of shale gas and potential new pipeline import capacity from Turkmenistan and Russia can swing LNG demand massively. Meanwhile, China’s regas capacity is rising; companies other than the national oil companies are participating in the global LNG market. Those companies have direct access to domestic end-use markets as they’re in the business of power generation, city gas distribution or LNG trucking. They can potentially move the needle in the competitions between LNG imports and pipeline imports.

China builds flexibilities into gas supply chain

Considering the moving parts discussed above, China has been building more flexibilities into its gas supply chain. From upstream exploration and production investment to midstream infrastructure expansions, to improving pricing mechanism and demand-side management in the downstream markets. Notably, China has accelerated underground storage capacity investment. It will add 63 billion cubic meters (bcm) of effective underground capacity in the next ten years, which could potentially flatten the seasonal gas profile. More detailed tier-pricing has been designed and built into domestic wholesale gas contracts and more timely and structured pricing linkages are implemented in end-user tariffs adjustment, potentially making end-use sectors more responsive to gas supply costs.

China's evolving role in the global LNG market

China has signed significant LNG deals in the past two years already. With demand further increasing in the long run, there will be new appetite for term contracting. Meanwhile, flexibility in destinations as well as pricing will become even more important, as Chinese buyers need to coordinate between LNG portfolio and the evolving domestic market landscape. China will seek more influence on LNG pricing, and on the back of improving flexibility in its gas value chain, it could increasingly act as a swing market in the global LNG supply-demand balance.

{kind=link}

Want to keep track of our latest insights into global gas and LNG? Fill in the form to sign up for the Inside Track.