Stepping on the gas: the state of global methane policies and regulations

Methane ranks second only to CO2 in its impact on human-induced climate change.

3 minute read

Stephen Vogado

Senior Research Analyst, Carbon Policy

Stephen Vogado

Senior Research Analyst, Carbon Policy

Stephen focuses on carbon policy, taking a data-driven approach to help clients navigate the energy transition.

Latest articles by Stephen

-

Featured

Carbon mitigation: 2026 half-time report

-

Opinion

4 carbon policy developments that impact E&P decision-making

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Featured

Carbon management 2026 outlook

-

Opinion

Carbon policy: 5 things to look for in 2026

-

The Edge

Five key takeaways from COP30

As the world struggles to reduce greenhouse gas (GHG) emissions, international attention has turned to methane.

We recently took a comprehensive look at that state of methane policies and regulations around the world. Fill in the form for a complimentary selection of slides from our presentation, or contact us to buy the full report. In the meantime, read on for a brief introduction to this potent gas.

Why the focus on methane?

Methane has different properties to its better-known contemporary. Its release into the atmosphere is often accidental, stemming from leaky infrastructure, the disruption of mineral resources and the incomplete combustion of fossil fuels. CO2 emissions, in contrast, are primarily from the intentional combustion of fossil fuels.

Solutions to cut methane emissions, therefore, are often readily available, such as updating the technologies used in production and routing the vented gas to markets where it can form part of natural gas supplies. However, many of these solutions are economically difficult to apply at scale.

In addition, methane’s chemical properties make it a far more formidable GHG, with around 28 times the heating potential of CO2 over 100 years and around 80 times its potential over a 20-year timeframe. It also naturally breaks down in the atmosphere in a matter of decades, as opposed to centuries for CO2. Consequently, quickly cutting methane emissions can have a tremendous impact on future temperature increases.

However, no nature-based recovery mechanisms exist for methane emissions as they do for CO2. The only natural sinks for methane are chemical reactions in the atmosphere and a small amount of intake by soils. In contrast, forest and land-use management can increase natural CO2 sinks and counterbalance its emissions. Consequently, avoiding methane emissions is paramount, as removal is impossible once emitted.

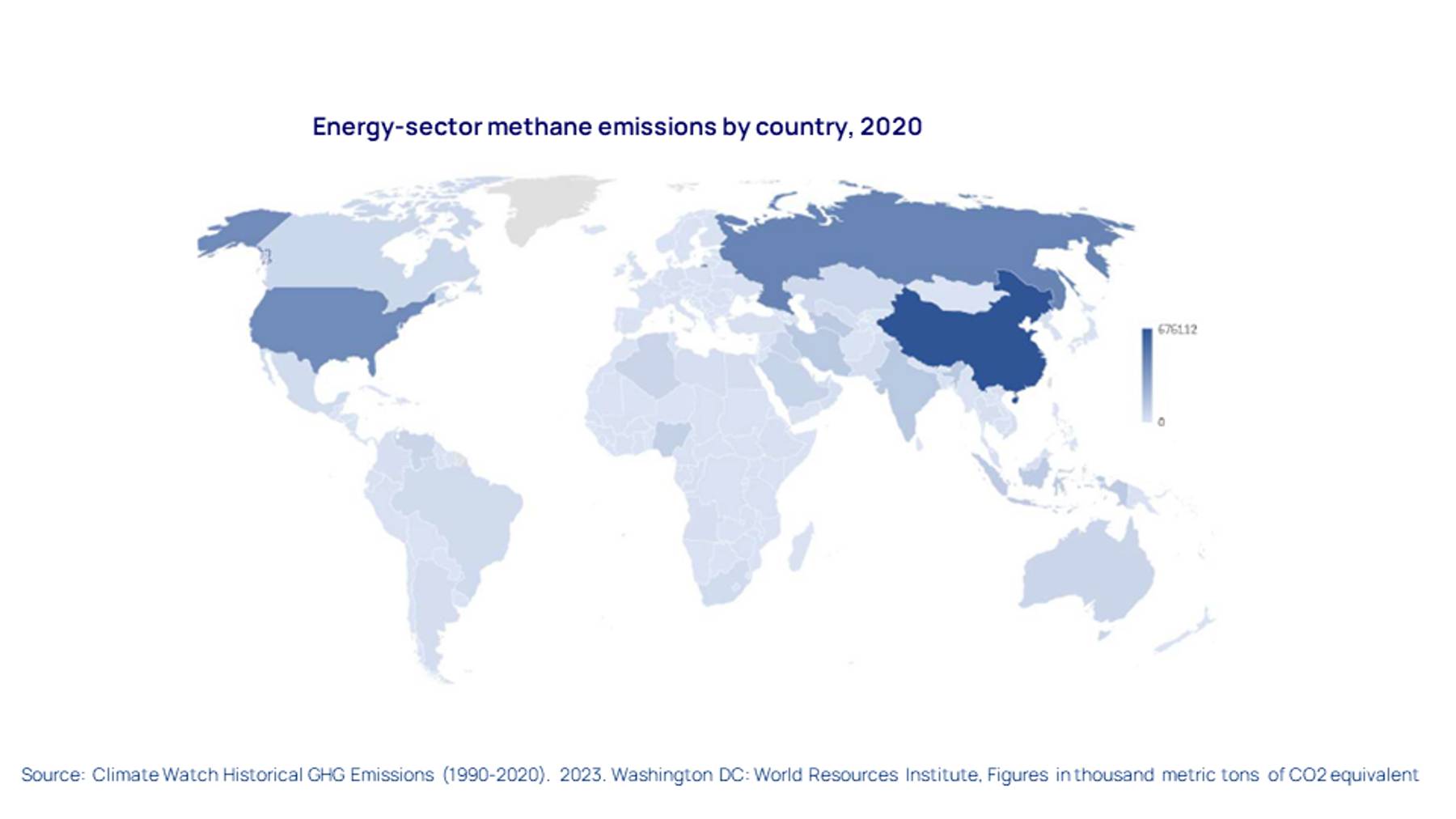

Who are the biggest methane emitters?

Countries with large levels of unconventional, onshore oil and gas production are considered to be large emitters of methane, but without improved detection and data accuracy and better reporting standards around methane, it is difficult to gain a clear picture of where the main sources of methane are occurring on a country basis.

Facility operators are also key determinants of methane emissions. Two operators in the same country can have very different production methane intensities, reflecting disparities in operational standards and focus on climate-related issues.

Unconventional production and associated pipeline networks can have significantly higher methane emissions intensities. Areas such as the Permian basin have large numbers of small facilities distributed widely across a huge area, each with infrastructure and technologies that are prone to leaks.

Here it is not economically viable to capture fugitive gas or feasible to link every facility to gas distribution networks. The costs of abating methane outweigh the economic losses associated with gas leaks, so companies have no inherent financial incentive to cut methane emissions.

This explains why the US is such a heavy emitter of methane, while China’s metals and mining sector contributes significantly to its status as the world’s top emitter of methane.

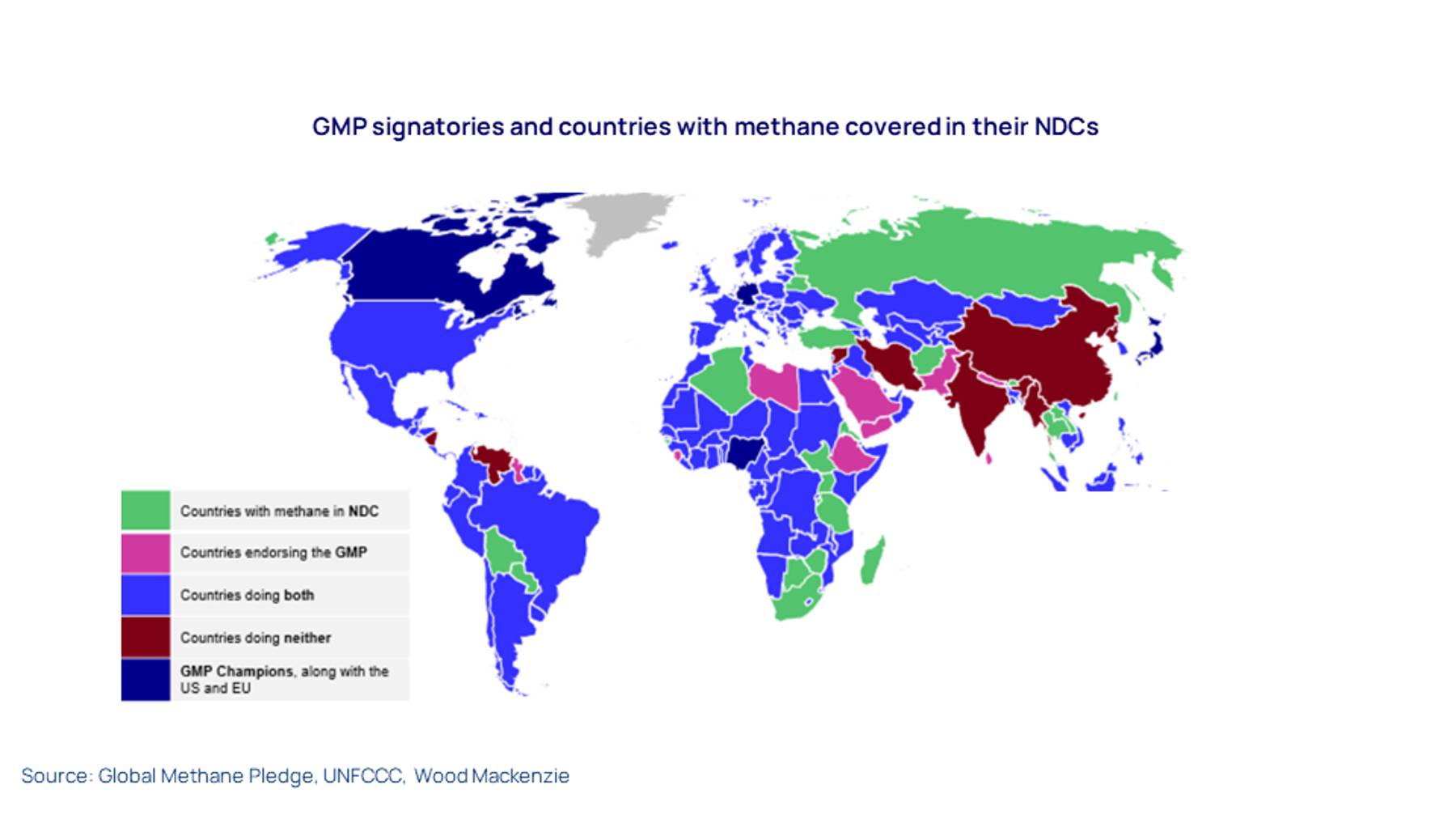

Methane abatement initiatives

There are several national, jurisdictional and company-level initiatives in place to reduce methane emissions.

Foremost is the Global Methane Pledge (GMP), signed by over 150 countries and launched a few years ago by the EU and US. Methane is also widely – but not completely – recognised in countries’ Paris-aligned domestic climate change mitigation measures and outlined in their nationally determined contributions (NDCs).

More recently, countries have written into law specific methane abatement requirements focused on the oil and gas sector. In many cases, this can be seen as a legally binding manifestation of the GMP’s aims and is something we expect to see occurring more frequently in future.

{kind=link}

{kind=link}

{kind=link}

At the company level, methane reduction efforts come from various pledges, schemes, disclosure requirements and reporting frameworks.

Fossil-fuel companies are a particular focus due to their sizeable contribution to anthropogenic methane emissions and the relative cost-effectiveness of abatement measures. Schemes typically have between 20 and 50 signatories, many of which are repeat signatories across multiple initiatives.

These numbers, therefore, mean the vast majority of oil and gas companies have yet to sign up to any methane abatement pledge or scheme, and most global fossil fuel-related methane emissions fall outside of the scope of these schemes.

Please contact us to purchase our report, which includes a breakdown of methane actions and policies at country level and a more detailed overview of corporate measures, or fill in the form above to receive some complimentary slides.