Sign up today to get the best of our expert insight in your inbox.

What different scenarios tell us about the future of oil and gas

Demand, supply and price in a 2-degree world

1 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

Can US success in tight oil and shale gas go global?

What does a net-zero pathway mean for the oil and gas industry? As capital markets and an ever-widening stakeholder community demand clarity and action on decarbonisation, more of our customers are talking to us about how they should incorporate such scenarios into their planning.

In our April Horizons, three of Wood Mackenzie’s senior analysts, Ann-Louise Hittle, Massimo Di Odoardo and Alan Gelder, present a view of that future, based on our 2 °C ‘accelerated energy transition’ scenario – AET-2.

The team used Wood Mackenzie’s proprietary models to forecast oil and gas demand, supply and prices through to 2050 in a world that aims to limit the average rise in global temperatures to 2 °C by the end of this century compared with pre-industrial times. Their analysis has profound implications for the industry and has stoked up a great deal of interest.

This week, the IEA published its own scenario, Net Zero by 2050 (NZE). The IEA NZE is aligned with the even more challenging 1.5-degree pathway and is closer in substance to our AET-1.5 scenario (which is also Paris-compliant and achieves global net zero by 2050).

There are strong similarities between AET-2, AET-1.5 and the IEA NZE – not least, in advocating the world needs to move fast if it’s to slow global warming. But there are also significant differences. We’ve drawn out some of the key messages from our Horizons analysis and IEA NZE’s on oil and gas.

The future of oil

There’s close alignment across the scenarios. In our AET-2 scenario, oil demand falls by 70% to 35 million b/d by 2050, decline setting in as electric vehicles and hydrogen disrupt road transportation, while recycling limits the feedstock demand growth for plastics. Both IEA NZE (no new ICE sales after 2035) and AET-1.5 are more aggressive – the decline starts almost immediately, and demand falls below 30 million b/d by 2050.

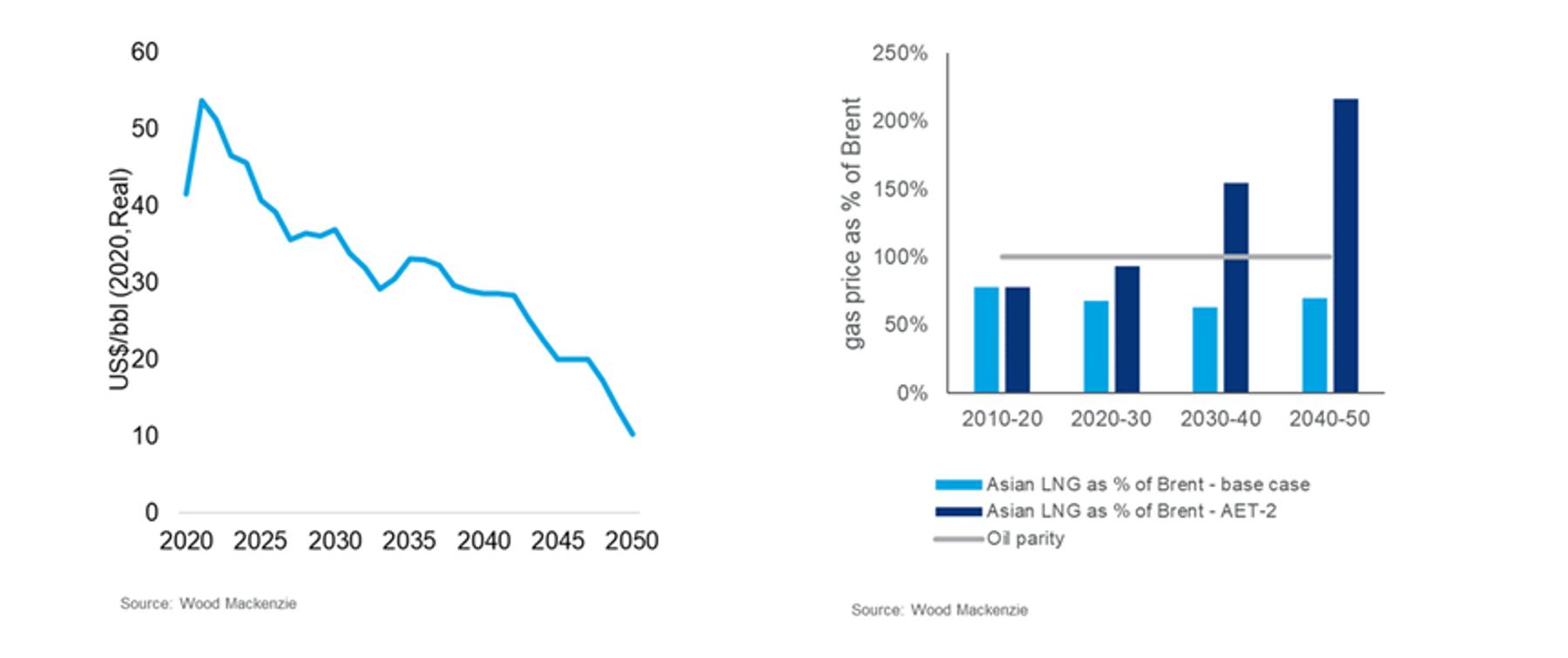

Both AET-2 and IEA NZE predict oil prices much lower than today’s – but AET-2 is materially lower in 2050. In AET-2, OPEC gains market share from 37% today to over 50% in 2050 (which IEA NZE concurs with) but loses its market power, with oil demand falling by 2 million b/d every year. By 2030 in AET-2, Brent averages US$37 to US$42/bbl (IEA NZE* US$35/bbl), by 2040, US$28 to US$32/bbl and by 2050, US$10 to US$18/bbl (IEA NZE* US$25/bbl).

The world needs no new oil supply in AET-2 – existing resources are sufficient to meet future demand. All three scenarios agree. However, in Wood Mackenzie’s view, exploration and production will play a role in this future, albeit a diminishing one. New projects and new exploration can come into the supply stack if the new resource is lower cost and has lower carbon intensity.

Refining faces continued rationalisation as oil demand collapses in all three scenarios. Changing product demand exerts huge pressure on refineries with gasoline and diesel demand dwindling but at different rates of decline. In AET-2, our current global gross refining margin indicators are all negative by 2050. Survivors in this shrinking market for refined products are coastal, primarily NOC-owned integrated refinery/petrochemical facilities located in industrial clusters with low-carbon operations (electrified processes, low-carbon hydrogen and CCS).

The future of natural gas

There are major differences between Wood Mackenzie’s scenarios and IEA NZE. In AET-2 we see a big window of opportunity for gas producers in the next 15 years. In AET-2, gas demand is much more resilient than oil, playing a central role in the transition. Gas demand in AET-2 is at similar levels to today in AET-2.

A key assumption in AET-2 is that a number of big Asian gas consuming countries don’t achieve net zero until a decade or two after 2050. Gas displaces coal in power generation due to its lower carbon intensity; combines with CCS/CCUS in power and industry; and is the feedstock for burgeoning blue hydrogen production. These opportunities provide support for gas demand while mitigating global emissions, including in AET-1.5 where gas demand is 18% lower than today’s levels.

A key message of AET-2 is that natural gas becomes more valuable than oil over the next two decades – a ‘Reversal of fortune’. Resilient demand pushes LNG and Henry Hub prices to a premium to oil, having traded at a discount through history. Capital shifts to gas, and US$1 trillion of investment is needed for new gas and LNG projects to meet future demand.

The biggest global producers, Qatar and Russia, can dominate the growing gas market as OPEC loses its grip over oil. But the gas business model has to adapt to prioritise management of carbon emissions across the value chain. The gas market of the future is carbon neutral, and one in which natural gas is combined with CCS or transformed into blue hydrogen to fuel the industrial and power sectors.

The IEA NZE is much more pessimistic on gas, forecasting 55% lower gas demand by 2050 compared with 2020. IEA NZE assumes gas demand is disrupted by higher energy efficiency, more rapid penetration of hydrogen and a wider use of bioenergy combined with CCS.

IEA NZE sees no need for investment in new gas supply. While it expects LNG prices eventually to trade at a premium to oil by 2050, the shift is nowhere near the ‘Reversal of Fortune’ for global gas prices in our AET-2.

The future of oil and gas companies

No oil company is preparing for the scale of decline envisioned in any of these scenarios. The decline in oil output in AET-2 would lead to asset impairments and bankruptcy or restructuring; those long in refining face a double whammy. Portfolios of Majors and most NOCs today are largely out of step with a switch to gas.

Big Energy outperforms Big Oil in AET-2. Cash generation from oil and gas this decade will be re-invested in renewables, hydrogen and CCS to build a sustainable business. Most IOCs and NOCs though do not have the scale or capability to follow this new path.

Resource-holding NOCs face pressure to bolster government income; revenue optimisation turns from price support to maximising volume and avoiding stranded assets.

One final point on investment. E&P spend today is already at a 15-year low and would fall rapidly if these scenarios unfold. With pressure on the industry to reduce investment, there’s a risk of higher oil and gas prices this decade should the transition take longer to gain traction.

Our May Horizons looks in detail and the implications of a 2 °C world for upstream oil and gas.

* IEA NZE oil prices 2019 real, AET-2 2020 real

{kind=link}