COP28: a metals and mining stocktake

Metals have a crucial role to play in providing materials for low carbon technologies that will reduce fossil fuel use

3 minute read

Daniel Carvalho

Director, Metals & Mining Consulting

Daniel Carvalho

Director, Metals & Mining Consulting

Daniel brings over 18 years of experience as a global operations, process and technology leader.

Latest articles by Daniel

-

Featured

Metals & mining 2025 outlook

-

Opinion

Four key takeaways from LME 2024

-

Opinion

Grey area: can steel really go green?

-

Opinion

How do Western sanctions on Russia impact the global metals, mining and coal markets?

-

Opinion

What’s next for green steel technologies?

-

Featured

Metals and mining 2024 outlook

Negotiations at this year’s COP28 gathering are centred around the Global Stock Take (GST) which, two years in the making, provides a basis upon which to reset emission goals, and reignite global ambition.

Although not a focus of discussions in the UAE, the mining sector has a crucial role to play in providing the materials for low carbon technologies that will enable the necessary deep reductions in fossil fuel use.

Our latest report COP28: a metals and mining stocktake provides a chance to reflect on how the mining sector has responded since global emissions targets were first enshrined at the Paris COP21 in 2015. In the full report we explore what have miners and investors achieved, how have markets changed and what needs to be done to enable ambition to become reality.

Fill in the form to download the full report and read on for a brief introduction to some of these discussions.

How has the metals and mining sector responded since Paris in 2015?

Transport electrification and renewable power generation, core components of the zero-carbon pathway, are inherently metals intensive. We have witnessed a remarkable surge in the manufacturing of electric vehicles since the COP21 Paris agreement eight years ago, now constituting a quarter of new car sales—a substantial increase from less than 1% in 2015. The mass production of Li-ion batteries has evolved from conception to a tangible reality. Concurrently, the global addition of 165 GW of solar and wind capacity annually since 2015 underscores the expanding footprint of renewable power.

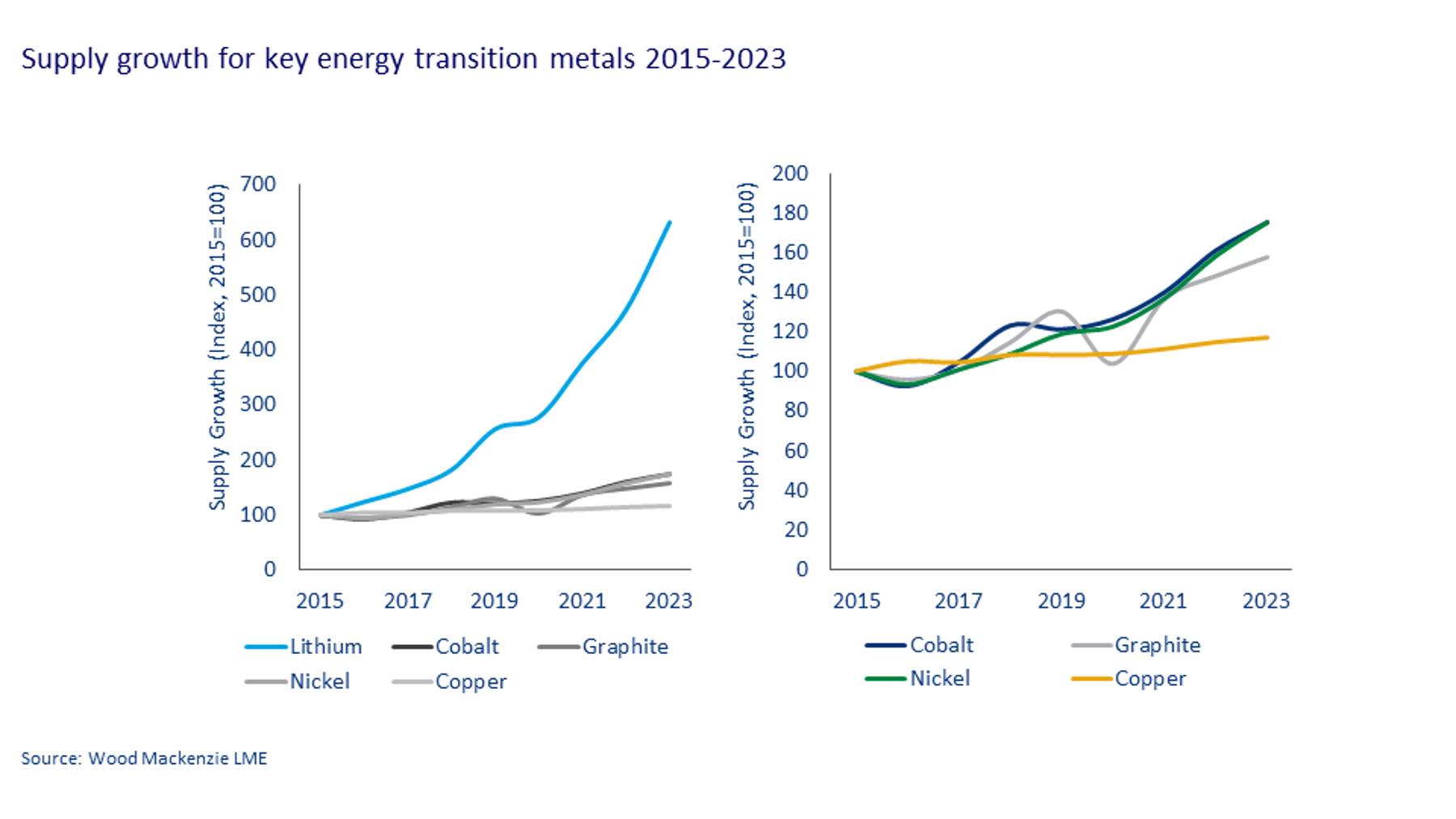

Considering the challenges of financing and developing mining projects, investment rates and supply growth since 2015 have been impressive. Much of this new supply coming in the last two to three years, as investment decisions made in the mid-2010s have come to fruition. Refined lithium supply – at ~1.0 Mtpa - is now six times larger than in 2015, while cobalt and graphite markets have nearly doubled in size over the same period. More mature markets such as nickel and copper have also gone through an energy transition supply boost.

The challenge for miners grows every year, but the sector has come a long way.

{kind=link}

In 2015, few major diversified miners had definitive plans to decarbonise, and almost no visibility on the technologies that would be used to achieve it.

Fast forward to today and almost all diversified miners have committed to net-zero operational emissions by 2050, some leading with very aggressive timelines (e.g. Fortescue by 2030).

Policies are expanding to bolster the development of domestic supply chains, partly aiming to decrease reliance on China.

Notably, the US Inflation Reduction Act (IRA) and Europe's REPowerEU have introduced direct incentives and specific policies to encourage the adoption of new technologies. Japan, South Korea, China, Canada, and India are aligning with this trend through strategic initiatives. Their policy shifts and critical mineral acts indicate a heightened awareness among decision-makers regarding metals' pivotal role in the energy transition.

It is clear there has been significant progress, but has it been fast enough?

What else is needed to deliver Paris agreement goals?

Despite the evident progress, we anticipate that the upcoming COP28 global stocktake (GST) will underscore the need for greater efforts. We hope that participants acknowledge the vital role of metals in achieving climate targets and resolve to aggressively facilitate metals supply. The task has hardened amid a less favourable geopolitical landscape and a weak pricing environment that could shift miners’ focus away from growth.

Wood Mackenzie’s energy transition team has identified four of the biggest changes needed to deliver on Paris Agreement goals, across the commodities spectrum: Investment into clean energy infrastructure, new financing mechanisms, oil and gas company contributions, and global cooperation. We have reviewed what this could mean for metals and mining specifically and have added a fifth measure – the development of the circular economy and recycling, full details on these five challenges are available in the full report.

Fill in the form at the top of the page download the full report.