Coronavirus pushes UK gas market to deadlock

4 reasons why UK gas producers are suffering from the summertime blues

1 minute read

Murray Douglas

Vice President, Hydrogen & Derivatives Research

Murray Douglas

Vice President, Hydrogen & Derivatives Research

Murray is responsible for Wood Mackenzie’s global coverage across the hydrogen value chain.

Latest articles by Murray

-

Editorial

Our biggest takeaways from Wood Mackenzie's Hydrogen Conference 2026

-

Featured

Hydrogen: 5 things to look for in 2026

-

Opinion

eBook | Overcoming the challenges around hydrogen deployment

-

The Edge

Securing offtake for green hydrogen

-

Opinion

Hydrogen: the outlook to 2050

-

Opinion

Our top takeaways from the World Hydrogen Summit

Note from the editor: The UK gas balance will continue to evolve rapidly as domestic production falls and the LNG market tightens – explore future dynamics using our H1 2020 Global Gas Model Next Generation.

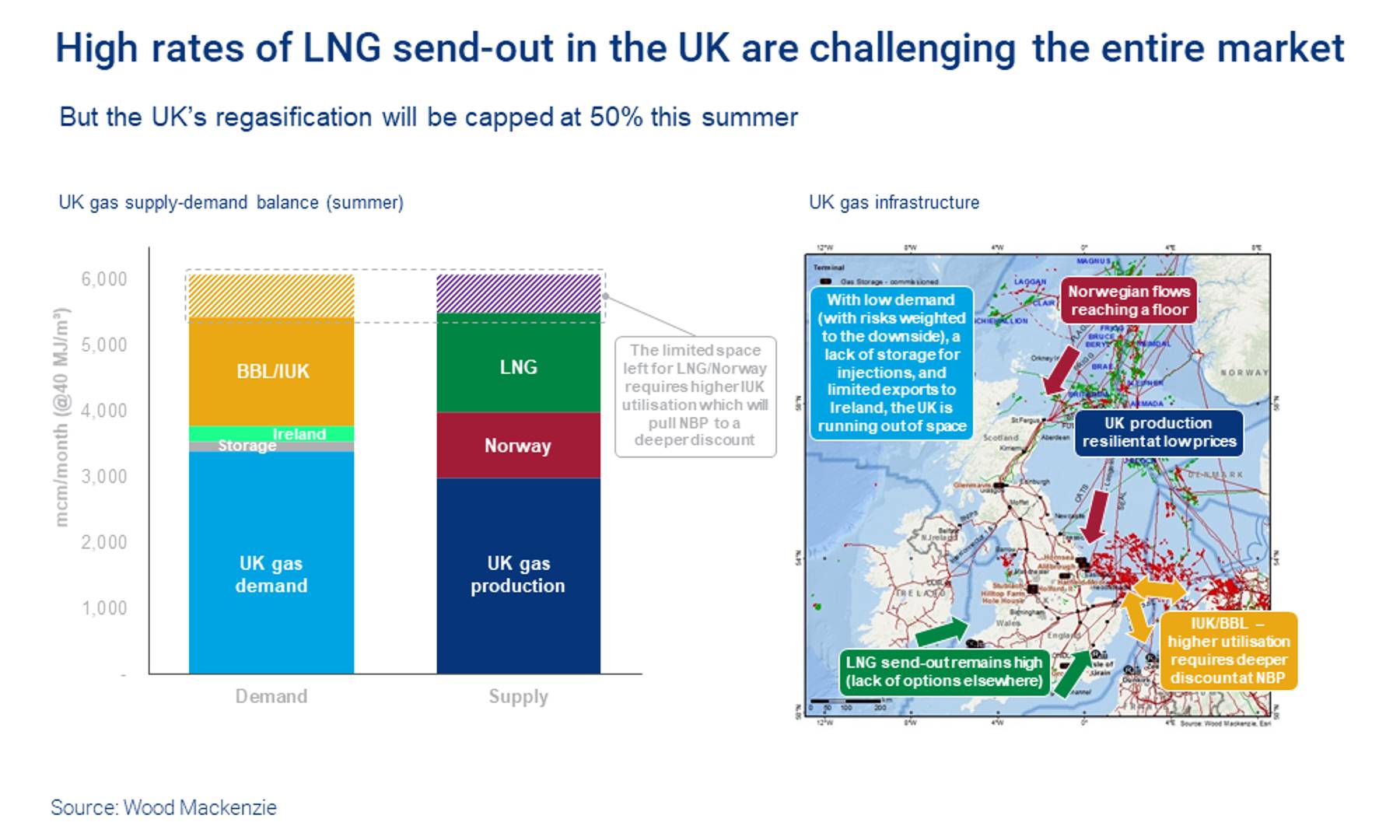

The UK gas balance has reached a deadlock for the summer. Resilient UK production, Norwegian piped imports and baseload LNG imports are all overwhelming the market with supply. And with lockdown placing huge pressure on electricity and fuel markets, demand will be weak throughout the summer.

Compounding matters, the UK has very limited storage capacity for injections and is approaching the limits on its ability to export volumes into neighbouring markets. Put simply, the UK market is running out of space.

Murray Douglas, Research Director for Europe Gas, explains why summer is crunch time and what’s challenging UK producers most.

{kind=link}

1. Falling demand will be most acute in summer

The industry and power sectors account for most of the UK’s summer gas demand. And both of those sectors have been hit hard by the lockdown measures. Although restrictions have started to ease, it will be a slow process. Gas demand will take time to recover. With current lockdown measures now continuing throughout May, we expect that demand will come in 18% below its five-year average. Demand will remain weak through the summer, regularly testing a floor of just 3,000 mcm/month.

2. For now, UK domestic production remains strong

UK gas production has been resilient, exceeding 2019 levels year-to-date by 3%. While UK producers are suffering from low gas prices, we don’t expect any material production shut-ins. Operators are likely to delay non-essential spring and summer maintenance where possible. This could add additional volumes to the market through to July, but potentially ease the pressure in late-summer.

3. Exports nearing capacity; LNG imports ramping up

Exports are reaching their limits: Space in the Irish market is very limited and offers no upside. Meanwhile, the UK is making full use of its export capacity to Continental Europe through the two pipelines – IUK and BBL – that connect UK to Belgium and the Netherlands, respectively. Typically flowing towards the UK during winters, these pipelines offer a safety valve into Europe during periods of oversupply. Flows on both pipelines has been high. But increased utilisation comes at a cost, which would require a deeper discount on the UK’s NBP versus continental benchmarks.

Norwegian piped suppliers are adapting to a changing market: Norway’s gas exports to the UK dropped by more than half in April in response to the limited market space. But we believe the low levels of Norwegian imports through summer won’t drop lower than 1,000 mcm/month.

But LNG has shifted in the opposite direction: Utilisation of the UK’s South Hook terminal has ramped up significantly as it absorbs more Qatari LNG that cannot find a home in premium Asian markets.

4. Storage could fill up by early June

The UK’s largest and only long-range storage facility, Rough, closed in June 2017. The field contained over two-thirds of the UK’s total storage volumes. Without it, it is more difficult for the UK to meet peak winter demand. It also makes it more difficult to absorb excess volumes through the summer months. And for this year’s summer season, storage is already very limited, with inventories more than 60% full. With less than 600 mcm of space for storage injections this summer, there’s a risk that storage could be full by early June.

Has all the UK market space already run out?

With UK summer demand expected to be lower than average and with limits on storage capacity, it’s clear that there is very little space for any additional supplies. LNG exporters hoping to place cargoes into the UK market have the most to lose. There simply won’t be space.

Consequently, the UK’s effective regasification capacity will be capped at 2,000 mcm/month through the summer – or just under 50% of total UK regasification capacity. LNG exporters desperately looking for market are fast approaching another brick wall.

Could gas prices fall into negative territory?

Speculation is mounting that Europe will deliver some negative gas prices this summer. Such a scenario is less likely on the continent but if it were to occur anywhere, the UK would appear most at risk. Indeed, all the way back in October 2006, the UK’s NBP experienced some negative within-day trades. Of course, the traded market was far less developed then and liquidity was limited with the European market still in the early stages of liberalisation. The cause of the negative prices was triggered by commissioning flows on Norway’s Langeled pipeline. It seems unlikely that Norwegian exports would increase sufficiently to deliver such an outcome once again.

Build your view of the global gas market

Look out for the H1 2020 global gas update, powered by our Global Gas Model Next Generation.