Sign up today to get the best of our expert insight in your inbox

US and Iran agree initial peace deal

The agreement will reopen the Strait of Hormuz, with further details still to be negotiated

1 minute read

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed Crooks

Vice Chair Americas and host of Energy Gang podcast

Ed examines the forces shaping the energy industry globally.

Latest articles by Ed

-

Opinion

Is fusion power here at last?

-

Opinion

Battery storage proves its value in moderating Texas power price volatility

-

Opinion

Can the LA Olympics in 2028 be a catalyst for clean energy?

-

Opinion

Strong El Niño event will have wide-ranging impacts on energy

-

Opinion

Why is it so hard to build big energy projects?

-

Opinion

Carbon capture continues to grow, despite challenges

The conflict in the Middle East began on 28 February, when US and Israeli forces began air and missile strikes against military and government targets in Iran. It was formally ended on Sunday, when the US and Iran electronically signed a memorandum of understanding (MoU) that is intended to lead to a lasting peace.

On Sunday afternoon, US and Iranian sources, and the government of Pakistan, which has been mediating between them, announced that a peace deal had been agreed. The MoU lays a foundation for a comprehensive agreement to be negotiated later. But in the meantime, both sides agree that the Strait of Hormuz should be reopened.

President Donald Trump posted on social media on Sunday: “Ships of the World, start your engines. Let the oil flow!”

Iran’s Mehr News Agency reported that a draft of the MoU, discussed last week, included an end to sanctions on Iranian exports, the unfreezing of US$24 billion of Iranian funds and a reconstruction plan worth at least US$300 billion. The Strait of Hormuz would be reopened “under Iranian arrangements”.

Pete Hegseth, the US secretary of war, said the release of funds would be performance-based, tied to Iran’s compliance with US objectives, including surrendering its enriched uranium and dismantling its nuclear programme. Sanctions would be lifted over time, in tandem with the progress of negotiations over the final peace agreement.

In the meantime, the administration hopes the strait can be reopened quickly. Hegseth suggested it could take two weeks to 30 days.

Differences between the two sides remain. Iran’s foreign ministry said it would be charging fees on vessels passing through the Strait of Hormuz, to cover navigation, environmental protection, insurance and other services.

US Vice President JD Vance said on Monday morning: “Our expectation is that the strait is going to be opened in a toll-free way for the long term.” He added that this was one of the details that needed to be worked out in negotiations between the two sides.

But the markets have already priced in expectations that the peace will last. Front-month Brent crude futures, which were trading at above US$110 a barrel a month ago, dropped to about US$83 a barrel on Monday morning.

The key question now is whether the US and Iran can reach a lasting deal to justify that confidence.

The Wood Mackenzie view

If the negotiations continue to make progress, and the Strait of Hormuz is reopened within a few weeks, the outcome will look most like the Quick Peace scenario that Wood Mackenzie sketched out last month.

In that scenario, the conflict ends up being just a “speed bump” for the world economy and energy markets. Oil supply from the strongest producers in the Gulf region can be restored relatively quickly. In some cases, a pre-emptive ramp-up has already begun. Shipping and logistics are likely to be the bottleneck in the early phases of the recovery, rather than upstream producers.

Countries with more complex assets, particularly Iraq, will take longer to recover, but could still return close to pre-war levels in six to nine months.

In LNG, global markets are likely to be tight until the summer of 2027, despite the return of exports from the Gulf. Global supply growth will be slower than was projected before the war. Some Gulf LNG facilities have been damaged, and there will be delays to projects currently under construction in the region.

However, the oversupply in world LNG markets that we have long been expecting remains inevitable, albeit delayed until 2028. US LNG cargo cancellations are likely to be required to balance the market, more than halving European prices by 2031.

Oil prices have been reflecting expectations about a binary pair of outcomes: either the Strait of Hormuz would be reopened, in which markets would be well-supplied and prices would fall, or it would not, in which case prices would have risen significantly higher.

Releases from strategic reserves and reduced consumption, especially in Asia, enabled the world economy to keep running despite the sharp reduction in global oil supply. But there were limits to how long that process could have continued.

The level in the US Strategic Petroleum Reserve (SPR) has been falling this month at a rate of about 8 million barrels a week. The SPR has a legally mandated minimum level of 252.4 million barrels that it can fall below only in an emergency. At the current rate of withdrawals, it would reach that level in about three months. Other gauges of oil inventories were also on course for historically low levels.

Facing that prospect, and the threat of higher oil prices and much more serious economic disruption, the US had a strong incentive to agree terms. Iran, already under extreme economic pressure, also has a good reason to try to make a peace deal stick.

The other big question for global energy is whether this crisis will have lasting impacts. In the three months since the war began, interest in investments that can reduce dependence on imported oil and gas, particularly from the Gulf, has surged.

Interest in coal, renewables and nuclear power has grown, as has the focus on hydrocarbon assets outside the Middle East, particularly in the Americas.

However, the structural advantages of the Gulf producers as sources of low-cost oil and gas have not changed. When exports can flow freely from the region again, they will be highly competitive in world markets.

Kristy Kramer, Wood Mackenzie’s head of LNG strategy and market development, draws an analogy with the Covid-19 pandemic. Claims were made then about how the world would be changed forever, and many of those claims turned out to be overstated. For example, it was argued that global oil demand would peak in 2019. In reality, it is continuing to grow.

While politics and conflicts can change rapidly, the fundamentals of geology and economics do not. The Gulf can be expected to remain a vital source of the world’s energy supplies for decades to come.

Other views

Is Argentina’s giant shale play the next Midland Basin? – Simon Flowers and others

Cushing crude stocks sit less than 2 mmbbls above operational floor amid global supply crisis

The US solar industry has a robust pipeline. So why is 2026 looking flat? – Zoë Gaston

Where global gas markets are mispricing risk – David Lewis

Video | Copper demand in an electrifying and digitising world – Charles Cooper

The ‘new joule order’ is here. The west is last to realise – Jeffrey Currie

The mysterious woman behind the Nord Stream explosion – Bojan Pancevski

Quote of the week

“The incident solar energy on the cross-section of the Earth is roughly a half-billionth of the Sun’s power output. And the vast majority of that we cannot use, because 70% of Earth is water… And then of the 30% that land, a bunch of it is Antarctica or Siberia-type of thing… not places people typically want to live… So the actual usable area of land where you can get solar power is quite small… In order to get to any meaningful percentage of the Sun’s energy harnessed, you have to go to space.”

Elon Musk spoke on the Brighter With Herbert podcast about why he thought the solar industry would have to go into space to realise its full potential.

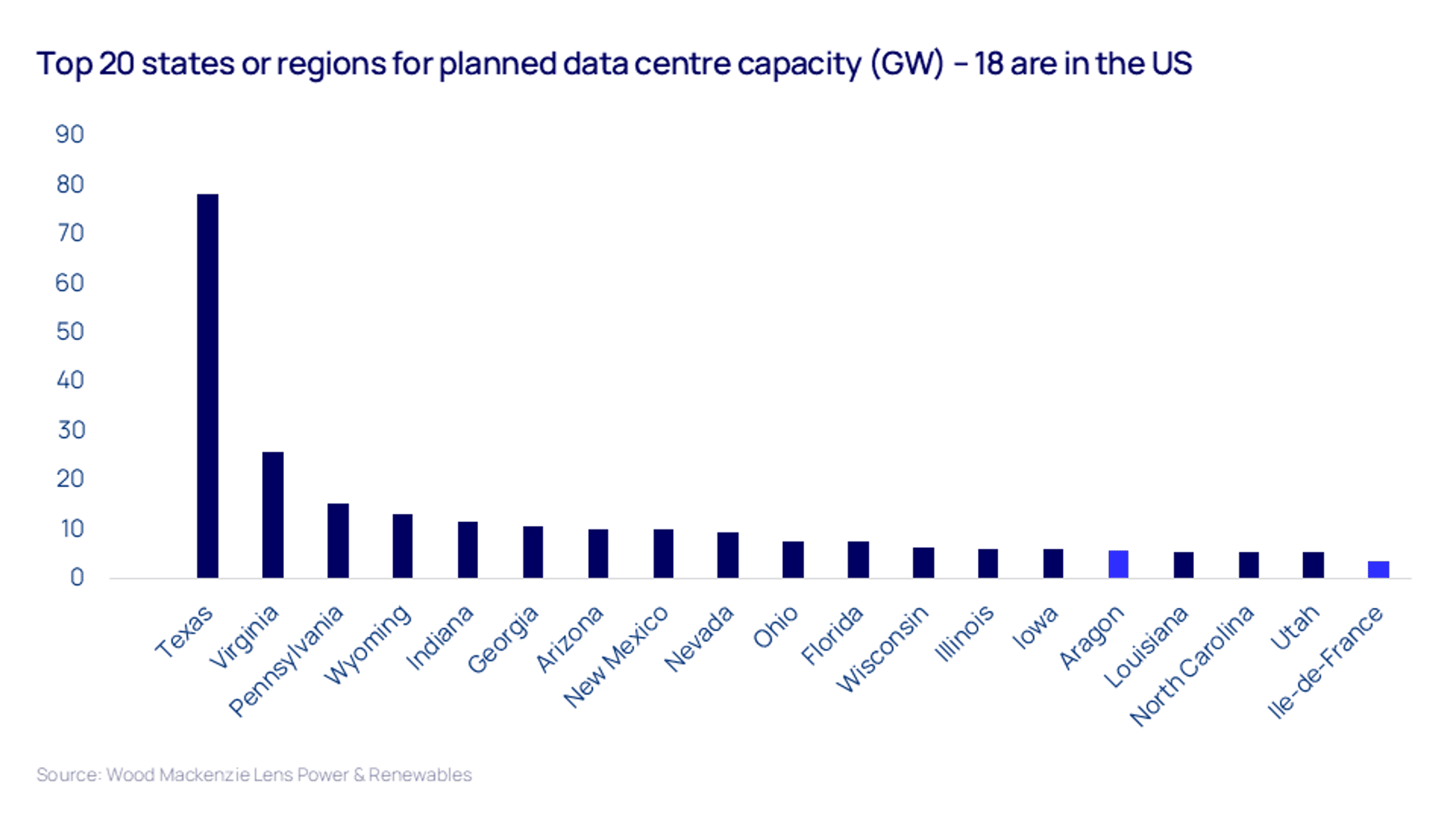

Chart of the week

This comes from Wood Mackenzie’s Lens Power & Renewables platform, which includes information on data centre projects around the world. It shows the world’s 20 most active states or regions for data centre development, of which 18 are in the US, and just two in the EU.

For insight into what the US data centre boom means for energy, take a look at our recent Horizons report: Breaking the speed limit: can US data centre development outpace grid development?

{kind=link}