Discuss your challenges with our solutions experts

Gulf Coast Express expansion begins commissioning

Early Permian takeaway signals begin to shift pricing

1 minute read

Daniel Myers

Senior Research Analyst, North America Gas

Daniel Myers

Senior Research Analyst, North America Gas

Daniel delivers short-term fundamental modelling and regional market analysis.

Latest articles by Daniel

-

Opinion

The Blackcomb question: can the pipeline reach its full 2.5 bcfd capacity at startup?

-

Opinion

Gulf Coast Express expansion begins commissioning

-

Opinion

US gas prices slide as storage expectations tighten: what it means for summer 2026

-

Opinion

Natural gas futures shrug off winter storm impact despite storage drawdown

-

Opinion

Winter Storm Fern shuts in 18.3 bcfd of US gas production at its peak

-

Opinion

US L48 gas: injection season ends

Vania Lara

Research Analyst

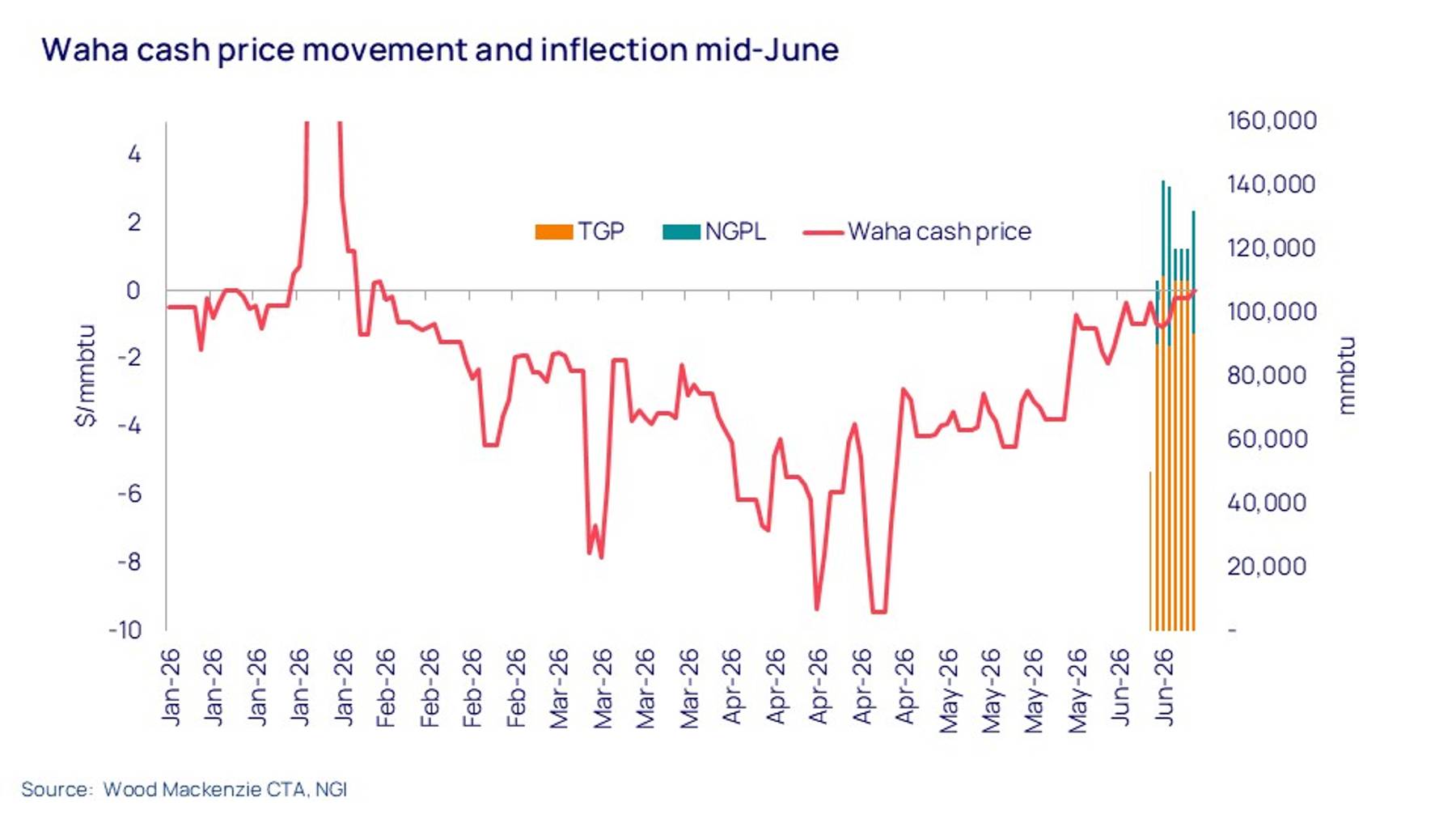

On 9 June 2026, two new nomination points linked to the Gulf Coast Express (GCX) expansion appeared in South Texas near Agua Dulce. Initial nominations were 50,000 MMBtu/d into TGP, followed by 20,000 MMBtu/d into NGPL on 10 June.

The expansion adds 570 mmcfd of incremental capacity, increasing total GCX system capacity to approximately 2.57 bcfd from Waha to Agua Dulce.

At the same time, Waha cash prices responded—rising above zero to $0.315/MMBtu for flow-date 16 June. This follows a prolonged period of weakness, with more than 130 consecutive days of negative pricing in 2026 and a record low of -$9.52/MMBtu on 16 April.

Our take

Early flows are already proving commercially meaningful. Waha prices moved from -$1.03/MMBtu on 8 June to -$0.34/MMBtu on 9 June, reaching positive territory by 16 June for the first time since February.

Nominations into NGPL and TGP confirm that commissioning is underway and point to early signs of wider Permian debottlenecking.

{kind=link}

Relief, but not resolution

Despite the initial price reaction, the underlying imbalance remains. Permian production is currently around 24 Bcf/d and is expected to exceed 29 bcfd by 2030.

While capacity additions are forecast to outpace production growth by 2027, the GCX expansion represents an early step toward closing the takeaway gap rather than a full solution.

What comes next

Further infrastructure will be required to sustain price normalization. The next wave of projects—including Blackcomb Pipeline and Hugh Brinson Phase 1—is expected to add around 4 bcfd of additional takeaway capacity before year-end.

Until then, pricing dynamics are likely to remain sensitive to incremental capacity additions and commissioning progress rather than reflecting a fully rebalanced market.

Looking beyond the expansion

The Gulf Coast Express expansion has delivered immediate relief to the Permian market, but the broader takeaway challenge remains unresolved. While new capacity is beginning to ease constraints, future pricing will continue to depend on commissioning progress, infrastructure delivery and the pace of production growth across the basin.

With projects such as Blackcomb Pipeline and Hugh Brinson Phase 1 still to come, market participants will be watching closely to see whether additional takeaway capacity can keep pace with rising supply.

Understanding how these developments translate into market outcomes requires visibility across infrastructure, flows and fundamentals.

Learn more about Commodity Trading Analytics