Sign up today to get the best of our expert insight in your inbox.

Can battery innovation accelerate the energy transition?

Technological progress holds real promise

4 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Julian Kettle

Vice Chairman of Metals and Mining

Julian Kettle

Vice Chairman of Metals and Mining

Latest articles by Julian

-

Opinion

Video | Data centres, copper and the power paradox

-

Opinion

Energy security shocks and coal’s role in a fragmented world

-

Opinion

Answering seven burning client questions on copper supply and demand

-

Opinion

Metals investment: the darkest hour is just before the dawn

-

Opinion

Ebook | How can the Super Region enable the energy transition?

-

The Edge

Can battery innovation accelerate the energy transition?

The mining sector is struggling to meet the future demand requirements of the energy transition. But while most hurdles will involve the extraction, processing and use of critical commodities, technological innovation is too often overlooked as a solution.

Batteries are at the sharp end and their evolution in recent years highlights how innovation can help address shortages of critical minerals and those with unacceptable ESG credentials. Julian Kettle, Vice Chair Metals and Mining, and Max Reid, Senior Research Analyst, Electric Vehicles and Battery Supply Chain Service, pick up the story.

What’s the status of competing battery technologies right now?

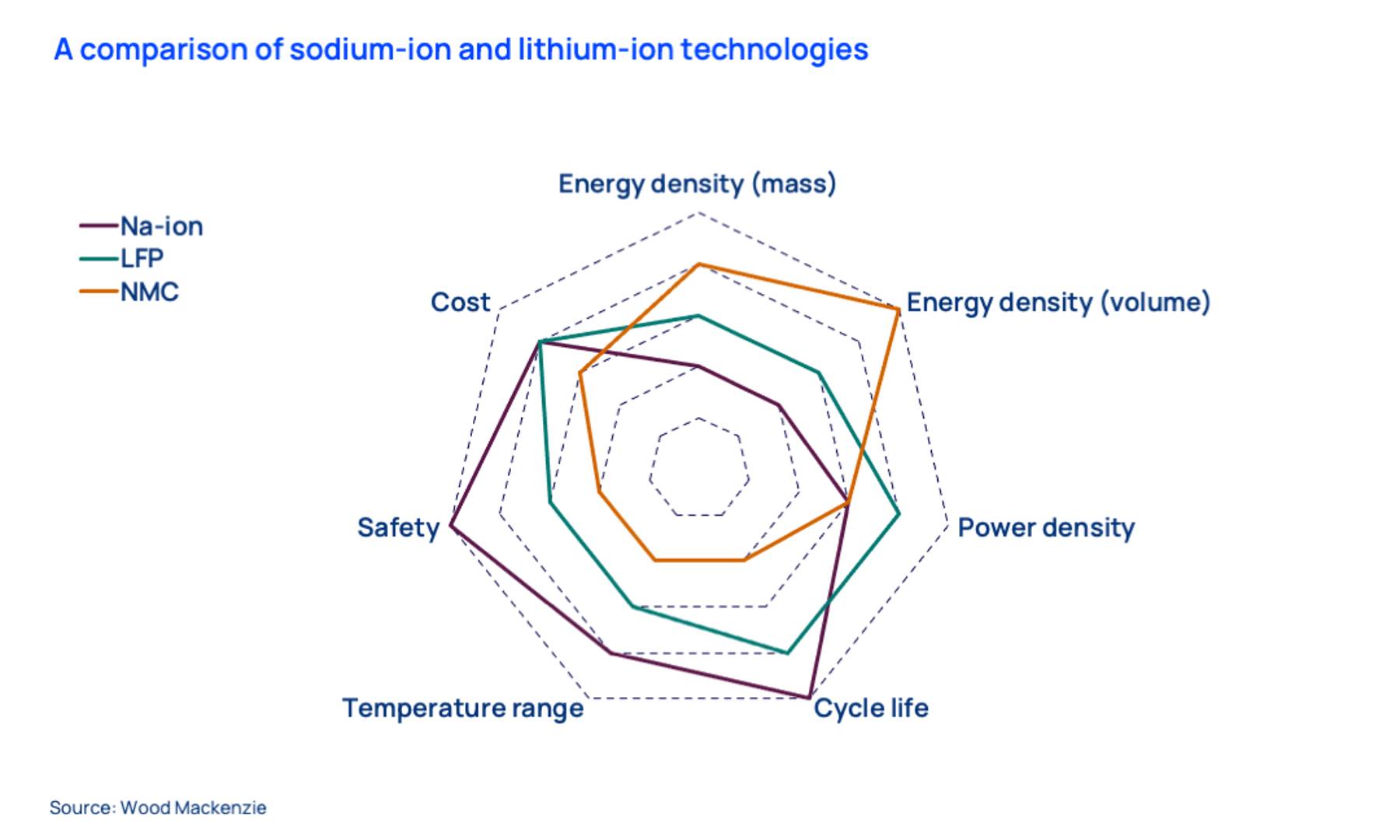

Until recently, most lithium-ion (Li-ion) batteries were available in either lithium iron phosphate (LFP, low-energy density but high safety) or lithium-nickel-cobalt-manganese-oxide (NMC, high performance) chemistries. But today the range of battery products is far more diverse than it was even five years ago as issues around electric vehicle (EV) range, safety and costs drive further innovation.

Replacing some iron content with manganese in LFP cells – dubbed LMFP – has reduced the energy density gap to the NMC chemistries. For the nickel-based chemistries, cobalt is being phased out and even eliminated to the benefit of nickel content. With lithium-based chemistries maturing, the current hype has switched to sodium-ion (Na-ion) technology – a similar technology to lithium-ion without the costly lithium, nickel or cobalt content.

Could sodium-ion battery cells be a game-changer?

The battery industry has continually proven its ability to innovate. Prior to major Chinese investment, there was very little attention paid to LFP chemistries due to their low energy-density, which limited their use in EV applications. But China saw the potential of the low-cost technology and developed large cell formats. This technology will power two-thirds of new EVs in China this year and has encouraged the likes of Tesla and Ford to follow suit.

The emergence of Na-ion has many similarities with the resurgence of LFP. Chinese firms are developing the technology – which contains little or no lithium, nickel or cobalt – to compete with current LFP chemistries for energy density. Fully discharged Na-ion cells can be transported safely, a further benefit compared to lithium-ion technologies. And with growing disquiet over metals supply challenges and ESG concerns in the Li-ion supply chain, Na-ion batteries could steal the march.

We’ve tracked announcements of over 150 GWh of Na-ion production capacity, enough to power three million EVs each year. And while that capacity figure is 10 times smaller than for lithium-ion, we’re still only at the starting line of the sodium-ion story.

What challenges remain?

While competitive with LFP chemistries, sodium-ion’s energy density can’t yet compete with the nickel-based Li-ion chemistries. At typically half that of current NMCs, range anxiety will hamper the adoption of Na-ion batteries for a large portion of the EV market unless energy density can be improved and sufficient high-density charging infrastructure is installed.

Na-ion also lacks Li-ion's established supply chains and production processes. Matching this will require billions of dollars of investment in gigafactories alone, with more still to build out cathode, anode and chemical production capacity. Given its track record of funding massive investments and driving down costs, China is again likely to take the lead.

But this isn’t only about China. Indian conglomerate Reliance Industries’ 2021 acquisition of Faradion – a UK sodium-ion developer – fits into India’s plans to join the battery scene this decade. Two factors – Na-ion’s suitability for stationary storage and the electric two- and three-wheeler market – should help to relieve pressure on Li-ion demand and its associated supply chain.

Does ExxonMobil’s acquisition of a second lithium project indicate Big Oil is getting serious about mining and batteries?

The lithium market neatly captures the challenges and opportunities for energy transition technologies. Demand for the alkali metal will triple in the 2020s; ExxonMobil has duly seen the potential to disrupt what is now only a 200-kt market. Furthermore, current high lithium prices present an opportunity to extract additional value from oil field brines containing low lithium concentrations.

ExxonMobil’s recent investment is small change for Big Oil as it looks to provide solutions to the energy transition. But more importantly, it could boost critical mineral production in the US to help reduce China’s manufacturing dominance. Challenges remain, but it may be that the relative unproven technology used for oil field lithium extraction requires companies of ExxonMobil’s scale and technical know-how to manage the downside risks.

How confident is the industry that it can keep delivering battery technology breakthroughs?

It’s clear that innovation in battery technologies is necessary to be in with a fighting chance of achieving net-zero. There is no one-size-fits-all solution, with vastly different demands to electrify the transport sector alone. Using different technologies where they’re best suited is the optimal method to meet the varying demands from the many applications that require batteries. Properly funded, the battery industry is confident it can continue to deliver.

{kind=link}