Sign up today to get the best of our expert insight in your inbox.

Could US data centres and AI shake up the global LNG market?

US gas demand growth threatens to push up the Henry Hub gas price

3 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

Eugene Kim

Research Director, Americas Gas

Eugene Kim

Research Director, Americas Gas

Eugene Kim is a Research Director on Wood Mackenzie’s Americas Gas Research team.

Latest articles by Eugene

-

Opinion

US gas prices slide as storage expectations tighten: what it means for summer 2026

-

Opinion

North America gas: 4 things to look for in 2026

-

Opinion

How LNG and power are shaping US gas pipeline development

-

Opinion

Summer 2025 wrap-up: gas generation falls despite higher power loads

-

Opinion

Permian basin gas outlook: Eiger Express FID adds to outbound build momentum

-

Opinion

LNG Canada makes historic first export shipment

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo brings extensive knowledge of the entire gas industry value chain to his role leading gas and LNG consulting.

Latest articles by Massimo

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

LNG: why a resilient portfolio is increasingly key to success

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How power markets can adapt to energy crises

-

The Edge

Ceasefire in the Middle East

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Shale gas has revolutionised the US gas industry over the last 15 years. Huge volumes of low-cost upstream gas have helped push coal out of the power generation mix and underpinned the burgeoning global trade in US LNG exports. The sheer scale of the resource had forged our view that Henry Hub prices would stay cheap as chips for the foreseeable future, underpinning US LNG’s competitiveness.

However, changing dynamics in US power and gas markets have led our team to take a more bullish view of how gas prices develop. I asked Eugene Kim, Massimo Di Odoardo from our Global Gas team and Gavin Thompson about their thinking and the implications for the LNG market.

What’s changed our view about US power and gas markets?

We’re forecasting much higher gas demand from power compared with two years ago. We raised our forecast for gas demand from the power sector from 2022 to reflect the difficulty the US faces in achieving its very challenging renewables build-out targets. We also edged up our forecasts for LNG exports, easily the biggest growth segment for US gas demand.

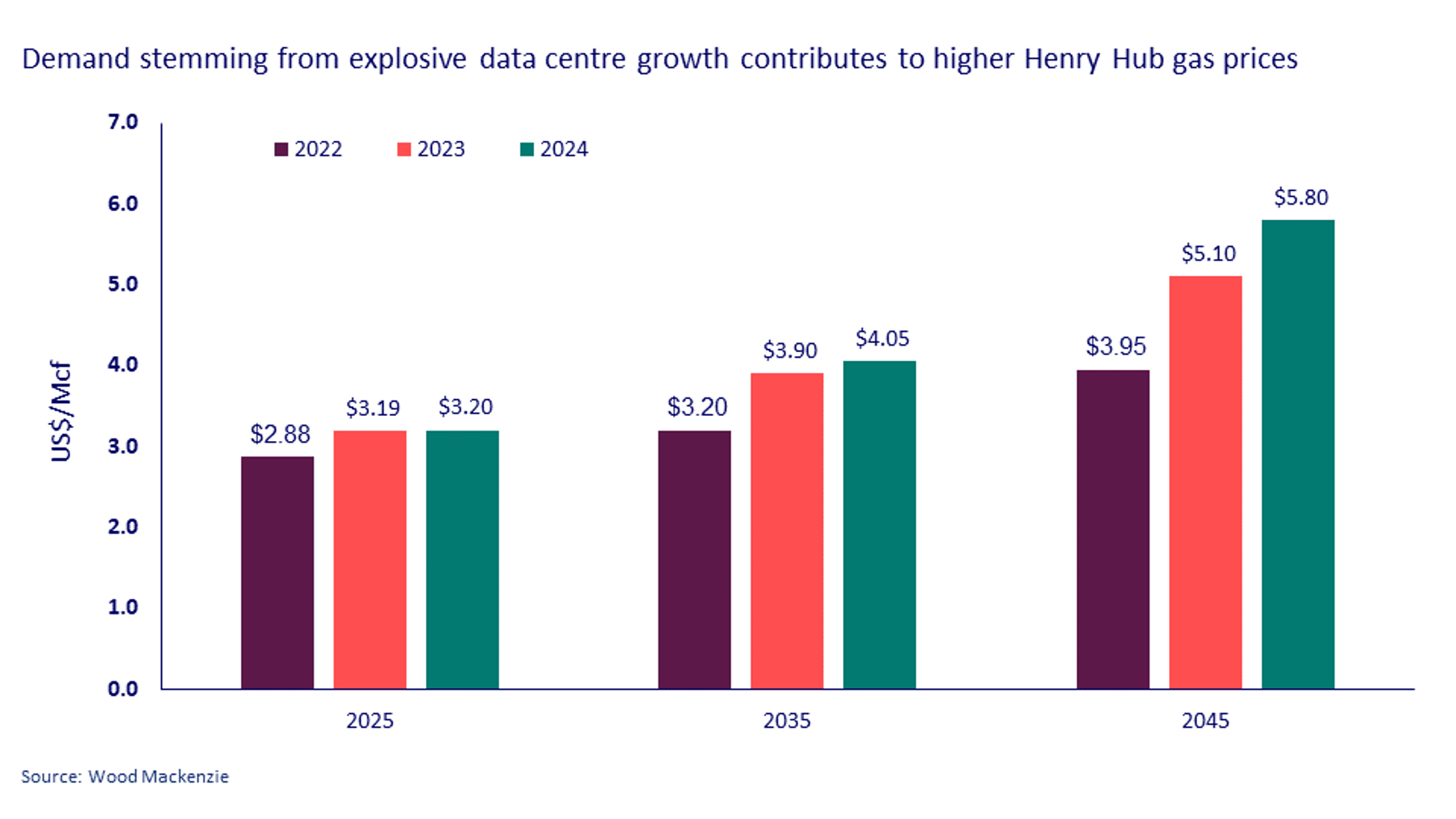

The second big upgrade came last month in our latest North America gas strategic planning outlook. It takes into account the explosive growth in datacentres and AI that’s unfolding, along with the reshoring of power-intensive industries such as chip manufacturing.

We now expect total US gas demand to increase by 30 bcfd (300 bcm) by the early 2040s compared with 13 bcfd (130 bcm) previously.

Is there enough supply?

Plenty, but the issue will be at what cost. The incremental gas demand will lead to the earlier exhaustion of low-cost resources, both from liquids-associated plays and the dry gas basins of the US Lower 48. A key assumption is the decline of associated gas from tight oil towards the end of the next decade with even the Permian hitting the wall in the mid-2040s.

As a result, Henry Hub prices are likely to experience upward pressure from the mid-2030s as higher cost plays are tapped, from the Marcellus in the Northeast to supply demand centres along the Atlantic seaboard.

How have our price forecasts changed?

Our ‘old view’ was that Henry Hub would be range-bound between US$3/mcf and US$4/mcf (in real terms) through 2045. We’re now expecting prices to hit US$4/mcf more than a decade earlier – good news for upstream producers who have experienced years of modest prices in a well-supplied market.

Beyond 2035, our modelling suggests the market gets progressively tighter, lifting Henry Hub closer to US$6/Mcf (in real terms) through the 2040s. That’s up to 45% above our forecasts of two years ago.

What are the implications for LNG markets?

First and foremost, there’s a huge global appetite for LNG. We forecast 230 Mtpa of new supply will be needed to meet demand growth to 2050, adding 30% more volumes to capacity already onstream or under development. The US will have a big part to play in delivering that supply. While price is critically important, US LNG has other advantages including flexibility for buyers on cargo destination, lower cost cargo cancellation options and swift project build times that conventional projects can’t match.

Most Asian buyers, including those in price-sensitive markets newer to LNG, will continue buying LNG on 15-to-20-year contracts and look at the economics over the life of the deal. For most of that contract exposure, Henry Hub-indexed LNG looks a pretty safe bet. The risk, based on WoodMac forecasts, is skewed towards the back end of a long-term contract.

Asian buyers will, as ever, compare Henry Hub-linked contract prices with oil-indexed contracts from conventional LNG projects. Today, the former is cheaper, based on US$80/bbl Brent and a 12% slope. But should Henry Hub prices drift upwards in the longer term, oil-indexed contracts from conventional projects will become a more attractive option, assuming the same Brent price or lower, and the same indexation. Over time, though, that arbitrage would close as higher Henry Hub prices would provide headroom for sellers to increase oil-indexation levels.

It’s also worth bearing in mind that buyers lament the lack of new, competitive sources of supply other than the US and Qatar. One potential positive that could emerge is that higher Henry Hub prices spur investment in new conventional sources of LNG outside these two countries.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.