Positioning for global LNG’s next big growth phase

How developers can be more competitive

4 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Dulles Wang

Director, Americas Gas and LNG Research

Dulles Wang

Director, Americas Gas and LNG Research

Expertise North America Gas markets Upstream oil and gas

Latest articles by Dulles

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

Opinion

How gas and power markets are inextricably linked in 2026

-

Opinion

North America gas: 4 things to look for in 2026

-

Opinion

How LNG and power are shaping US gas pipeline development

-

Opinion

Green gains: inside the rise of North American renewable natural gas

-

Opinion

4 things you should know about North American gas to 2050

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo Di Odoardo

Vice President, Gas and LNG Research

Massimo brings extensive knowledge of the entire gas industry value chain to his role leading gas and LNG consulting.

Latest articles by Massimo

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

LNG: why a resilient portfolio is increasingly key to success

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How power markets can adapt to energy crises

-

The Edge

Ceasefire in the Middle East

Giles Farrer

Vice President Research, Commodities, Gas & LNG

Giles Farrer

Vice President Research, Commodities, Gas & LNG

Giles heads our LNG and gas asset research and manages our market-leading LNG Service & Tool and LNG Corporate Service.

Latest articles by Giles

-

The Edge

Ten takeaways from WoodMac’s LNG Conference

-

Opinion

Five key takeaways from our Gastech 2025 Leadership Roundtables

-

The Edge

Gastech 2025: when will the music stop for US LNG?

-

Opinion

Debating the future direction of the LNG market

-

The Edge

Positioning for global LNG’s next big growth phase

-

Opinion

Third wave US LNG: a $100 billion opportunity

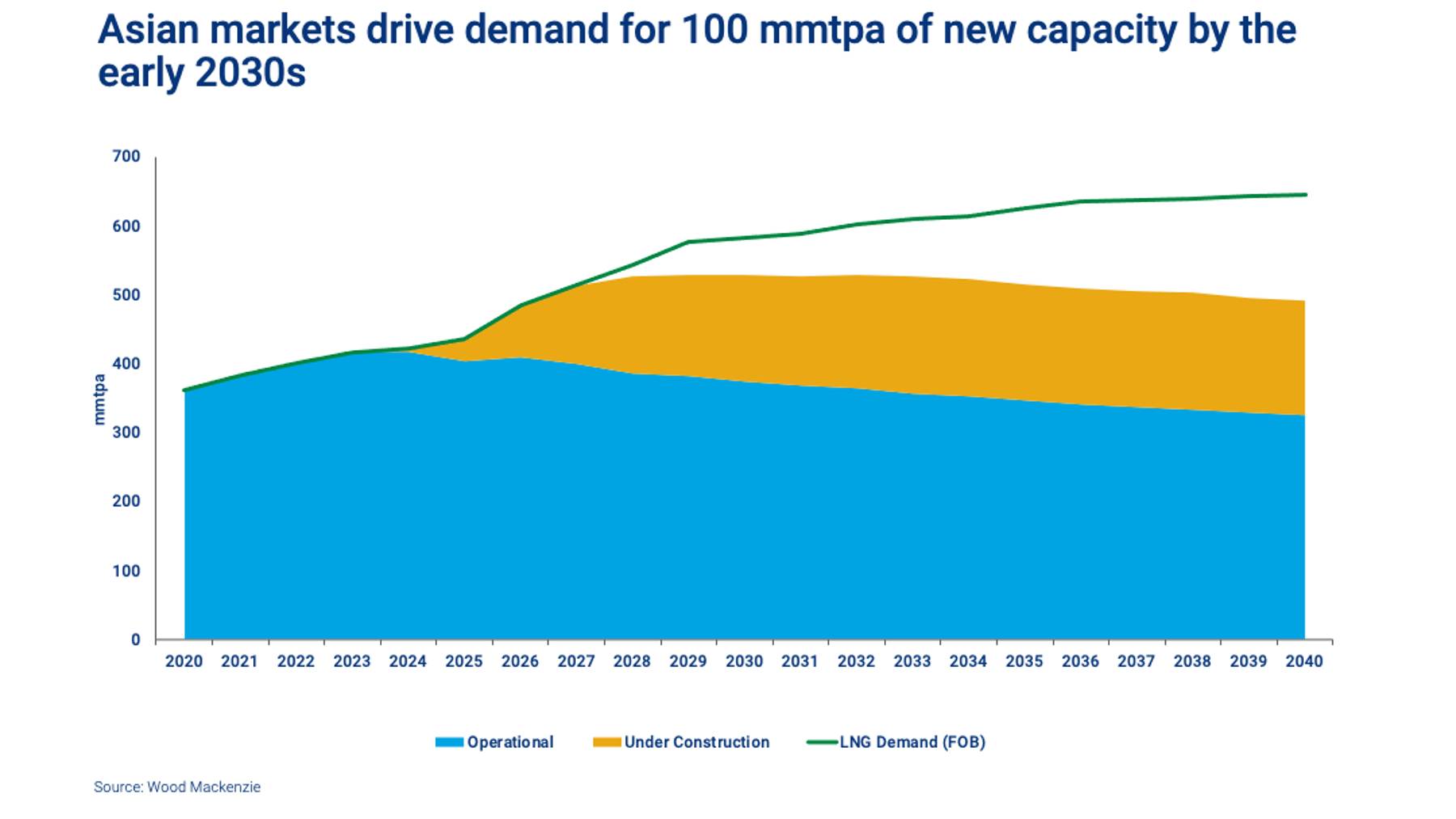

What a difference a year makes. Last July, sellers and developers of new LNG projects seemed to hold all the cards as European buyers fought to access volumes to cover the huge hole left by cuts to Russian pipe gas. Today, it’s a completely different story. Spot prices have dropped 90% since the peak of 2022 and a wave of new LNG supply is set to hit the market from 2025. While contract prices are still relatively high, the balance of power is quickly shifting back towards the buyers.

Developers must stay focused on the longer-term prize. The outlook for LNG is bullish, with another 100 mmtpa of capacity required to meet demand growth by the mid-2030s, a 25% uplift to current supply and on top of what’s already sanctioned. Ahead of next week’s LNG2023 Conference in Vancouver, our gas and LNG experts – Massimo Di-Odoardo, Giles Farrer and Dulles Wang – identify three of the challenges developers face and assess which suppliers are best placed to capture market growth.

First, protecting margins from cost inflation. The LNG industry isn’t immune to the global supply chain crunch and the flood of FIDs in the past two years is driving competition for labour and specialised materials. US LNG project development costs, below US$600/tonne pre-pandemic, have shot up to nearer US$1,000/tonne today. Qatar is set to pay 30% more to build its new mega-trains at North Field South than it did at North Field East, sanctioned only two years ago. Rising build costs are exacerbated by spiralling interest rates.

Developers will need to be innovative and look for low-cost solutions to develop liquefaction – among them, FLNG and smaller-scale modularisation. Alternatively, they can look for revenue upside through augmenting capacity via train rerating and debottlenecking. Increasing spot sales exposure is another way of boosting returns but comes with downside risk.

Second, meeting the growing demand for low-carbon-footprint LNG. As security of supply concerns fade, buyers and governments are refocusing on lowering CO2 emissions. The industry must seize this opportunity: reducing upstream, liquefaction and shipping emissions will prolong LNG demand through the energy transition.

Progress is being made. US LNG projects are looking to source certified RSG (responsibly sourced gas) to reduce upstream emissions, QatarEnergy and NextDecade plan to fit carbon capture and storage to liquefaction plants and many developers are considering electric-drive turbines sourced from renewables.

Lower-carbon LNG will command a premium price but comes at a cost. For the most carbon-intensive projects, this could be as much as an additional US$2/mmbtu on the delivered cost to jurisdictions that impose a carbon price on imports (assuming US$100/t).

An unintended consequence of governments that are serious about reducing CO2 emissions could be the emergence of a two-tier market. On the one hand, premium-priced, low-carbon LNG sold by lower-cost developers, such as Qatar and the US and, on the other, higher-carbon LNG from suppliers under less government pressure and that avoid investing in decarbonisation. The latter is only likely to be a short-lived option.

Third, doubling-down on Asian markets. Europe’s policy pivot away from gas limits upside for LNG suppliers beyond 2030. Thereafter, it’s all about Asia as the region’s developing economies lean more heavily on gas while striving to move away from coal.

China has been the primary target over the past two years, signing multiple long-term contracts. But the wider opportunity is now spread across multiple Asian markets, most with high growth potential. However, with limited existing infrastructure and, for the most part, sensitive to price, developers will have to work hard to crack these. Partnering with buyers from the region – as Shell is with Petronas, Mitsubishi, PetroChina and KOGAS in LNG Canada – can help unlock the opportunity.

Who is best positioned to deliver the next wave of LNG growth? Competition will be fierce, though Qatar and the US, already with 40% of global supply between them, will be the front-runners by a mile. Both have an abundance of low-cost gas, competitive pricing and astute commercial partnering. We forecast their combined market share will exceed 60% by 2040.

In contrast, Russia and Mozambique have slipped back down the field, unlikely to make headway anytime soon.

West Canada is a dark horse. The challenges for building out new capacity are clear. Construction costs are high in Canada, not least for new pipelines across the Rockies. Support from Canadian First Nations is critical to secure social licences.

But Canada also has much in its favour. There are huge RSG resources, multiple producers (including Asian companies) eager to monetise and a local benchmark, AECO, that trades at a healthy discount to Henry Hub. Another key competitive advantage is the proximity to North Asian markets, avoiding the constraints of the Panama Canal and cutting shipping costs by more than US$2/mmbtu compared with US Gulf Coast projects.

The LNG2023 hosts will be hoping these can move Canada from an also ran in global LNG supply into contention.

{kind=link}