Insights from the World Hydrogen Summit 2024

From winning auction bids to maximising project economics, here are our key insights into the development of low-carbon hydrogen from our experts’ presentations at the recent industry showcase

5 minute read

Greig Boulstridge

Research Analyst - Hydrogen & Derivatives

Greig Boulstridge

Research Analyst - Hydrogen & Derivatives

Greig is responsible for market tracking and ensuring data quality in Wood Mackenzie’s Lens Hydrogen platform.

Latest articles by Greig

-

Editorial

Our biggest takeaways from Wood Mackenzie's Hydrogen Conference 2026

-

Opinion

The 5 key takeaways from Wood Mackenzie's Hydrogen Conference 2025

-

Opinion

Enforcement and investment: how RED III is shaping the hydrogen market in the EU

-

Opinion

Hydrogen conference 2024: our biggest takeaways

-

Opinion

Hydrogen costs in 2024: what you need to know

-

Opinion

Insights from the World Hydrogen Summit 2024

Bridget van Dorsten

Principal Analyst, Hydrogen

Bridget van Dorsten

Principal Analyst, Hydrogen

Bridget is a hydrogen-focused principal analyst on our Energy Transition Practice.

Latest articles by Bridget

-

Opinion

Six months of data centre reality, from Bragawatts to behind-the-meter

-

Opinion

The grid's missing operating system

-

Opinion

The grid's immune system is retiring: Synchronous condensers, AI data centers and the physics gap that software alone can't close

-

Opinion

Beyond combustion

-

Opinion

Flexibility as a service: Can Octopus's acquisition of Uplight finally make US residential VPPs work?

-

Opinion

The muscle we forgot: SMRs, hyperscalers and why this nuclear renaissance might actually be different

Monica Trilho

Research Analyst – Hydrogen & Derivatives

Monica Trilho

Research Analyst – Hydrogen & Derivatives

Mónica is a hydrogen-focused research analyst for the Power & Renewables department.

Latest articles by Monica

-

Opinion

Enforcement and investment: how RED III is shaping the hydrogen market in the EU

-

Opinion

Hydrogen: the outlook to 2050

-

Opinion

Our top takeaways from the World Hydrogen Summit

-

Opinion

Hydrogen conference 2024: our biggest takeaways

-

Opinion

Our key takeaways from the Lisbon Energy Summit 2024

-

Opinion

Hydrogen costs in 2024: what you need to know

As a highly versatile energy carrier with exceptional energy density, hydrogen has the potential to play a critical role in the energy transition. Interest in hydrogen is rapidly moving from debate and aspiration to energy transition planning and policy. So, what do you need to know about the how the hydrogen economy is shaping up?

Our hydrogen analysts presented a range of proprietary research at the World Hydrogen Summit, which took place in Rotterdam from 13-15 May. Fill out the form at the top of the page to download a selection of slides from their presentations – or read on for a summary of some of the insights they shared:

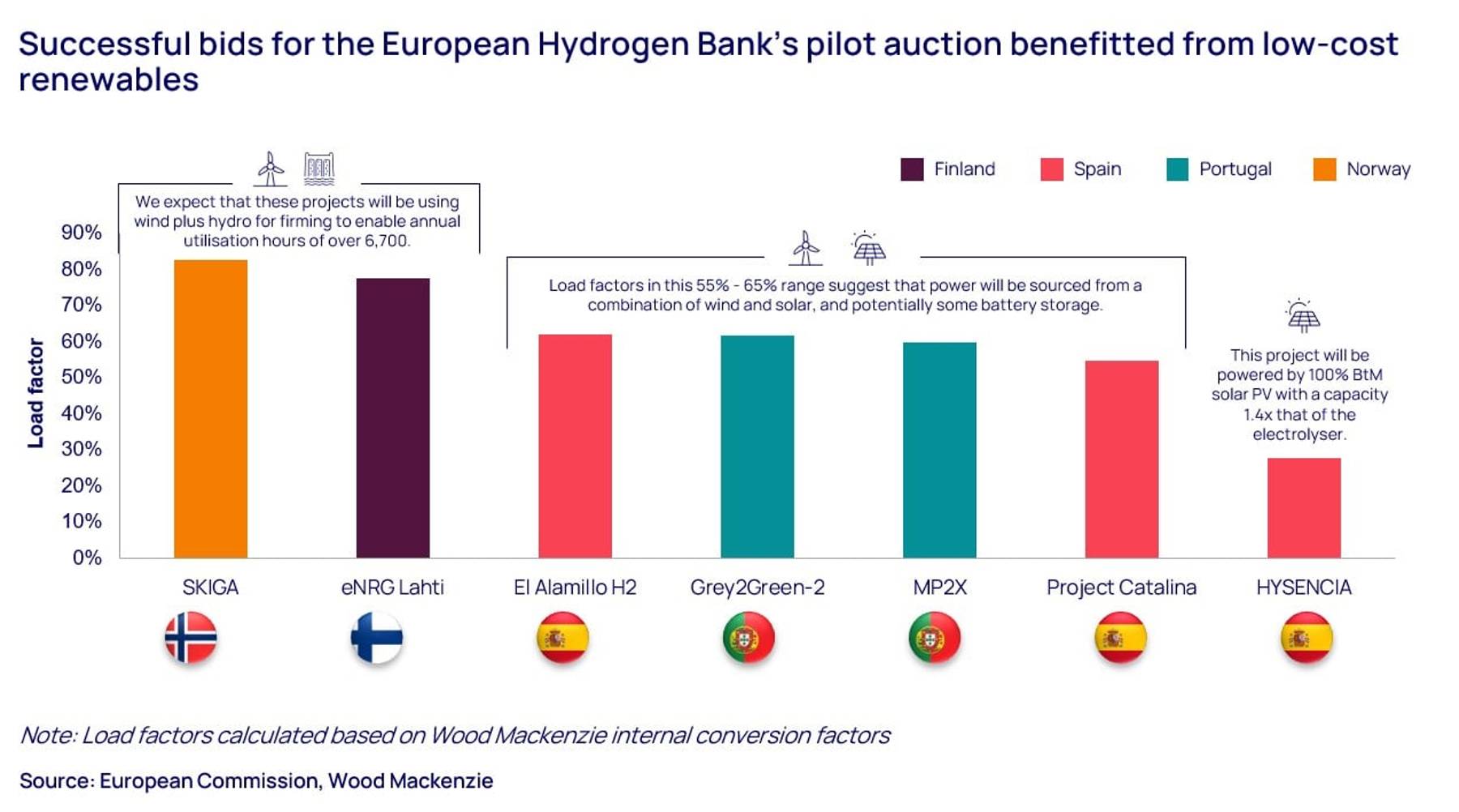

1. European Hydrogen Bank: pilot round complete, second round imminent

Announced by the European Commission in March 2023, the European Hydrogen Bank aims to establish a full hydrogen value chain in the European Union by stimulating and supporting investment in sustainable hydrogen production. Results of the Bank’s pilot auction were announced at the end of April, with seven projects across the EU receiving a total of €720 million.

As expected, successful projects had access to the lowest cost renewable generation mix, with southern European and Nordic markets significantly more competitive than northwest Europe (see chart below). The Nordic projects will use wind and hydro energy to achieve load factors of up to 80%. Most of the remaining successful bids have load factors in the 55-65% range, suggesting power will be sourced from a combination of wind and solar, possibly with some use of battery storage.

Despite ambitious government targets, well-developed projects and willing offtakers, average production costs for French and German projects are up to double those of their most competitive peers, preventing successful bids.

A second auction round will be launched in Autumn 2024. The maximum subsidy will be one euro lower, at €3.50, while the budget will rise to €2.2 billion. Meanwhile, the time to operation will be reduced from five to three years. A separate basket for supplying hydrogen to the maritime sector has also been suggested.

2. Ammonia: the most promising hydrogen carrier for seaborne trade

Despite considerable emissions, for practical reasons ammonia is the most promising hydrogen carrier for maritime trade. Firstly, it can leverage the existing vessel fleet and export/import infrastructure; secondly, hydrogen conversion to ammonia is a well-established process; and thirdly, ammonia can be employed directly in some end-use sectors. As a result, around 65% of low-carbon hydrogen projects targeting exports are aiming to use ammonia as a carrier.

The development of maritime trade in hydrogen remains uncertain; however, we expect seaborne traded volumes of hydrogen and carriers to reach 2.6 million tonnes per annum (Mtpa) by 2030. The use of larger capacity vessels will be preferred, as shipping ammonia in small vessels can more than double costs.

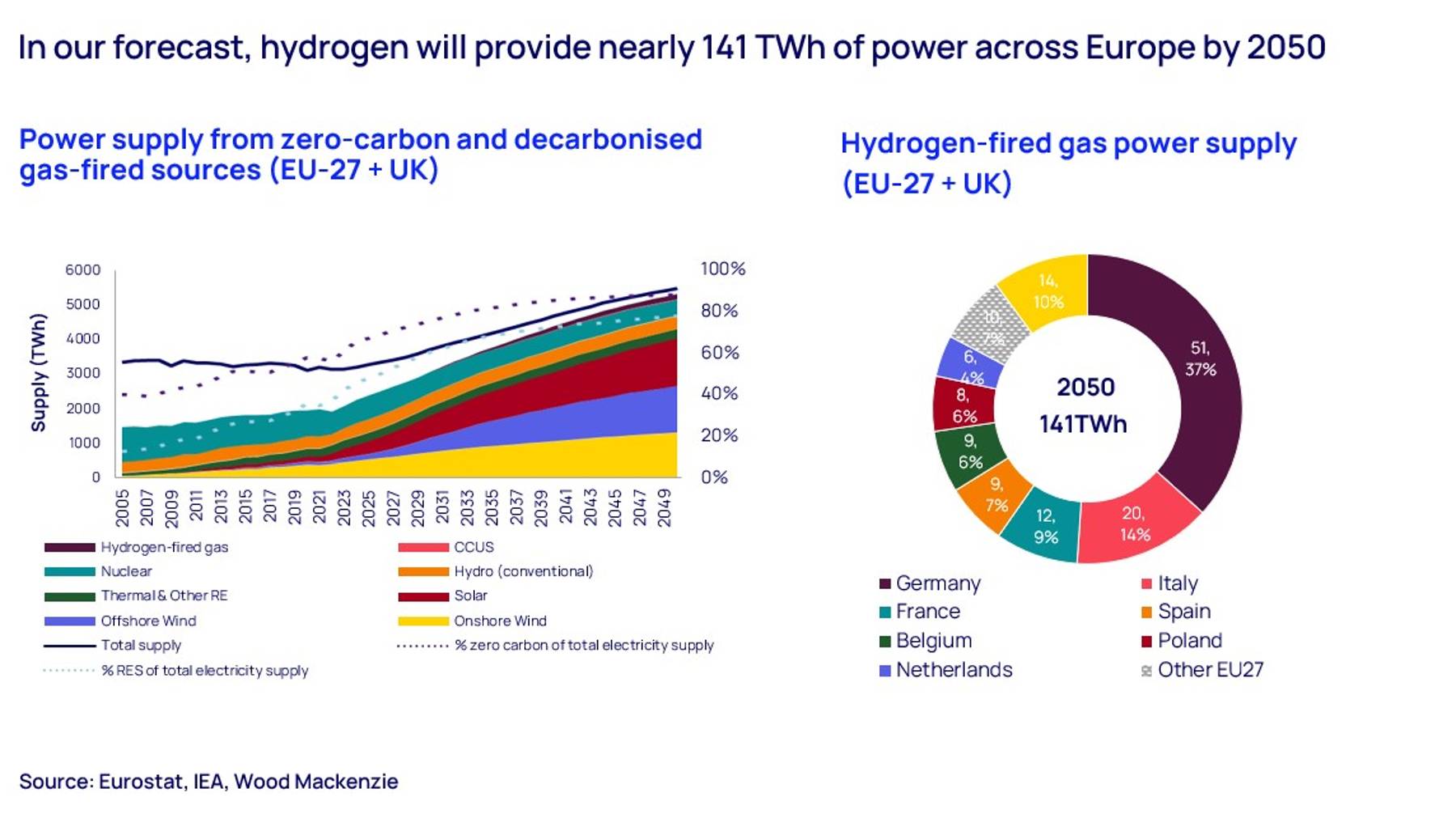

3. European power: The case for hydrogen-fired generation

Most European countries are progressing reasonably well towards sustainable power generation, with low-carbon generation exceeding 50% of supply in the majority of power markets. However, with oversupply increasingly frequent, low and even sub-zero prices are becoming more common.

This presents an issue for hydrogen-fired generation in terms of cost. However, in our forecast view, supportive mechanisms bridge the hydrogen cost gap; by 2050 hydrogen-fired power supply approaches 141 terawatt hours (TWh) in the 27 EU member states plus the UK, with Germany leading market take-up (see chart below).

{kind=link}

{kind=link}

4. Hydrogen project economics: opportunities to gain an advantage

There are a range of ways in which developers of low-carbon hydrogen projects can gain an economic advantage over their peers:

Target end-use sector: Industrial heating offers limited price premium; selling into mobility and power sectors may offer higher prices since costs can more easily be passed on to consumers.

Electrolyser choice: Opting for Chinese technology could significantly lower capital costs; however, governments wary of overreliance on overseas manufacturing could introduce regulations to prevent this.

Power sourcing: Behind-the-meter power improves security of supply and reduces exposure to price volatility, while co-locating with renewables minimises transmission losses, allowing a higher load factor.

Local gas supply: For blue hydrogen projects, locating the plant close to natural gas supplies can significantly cut the carbon emissions of the output.

Integrating end use: Co-locating the hydrogen plant with offtake facilities can cut operating costs and increase overall efficiency by minimising transport costs and losses.

Credible technology suppliers: Lowering technological risk by sourcing technology from credible suppliers with strong track records will improve bankability and may afford more favourable financing terms.

5. US hydrogen: what next for the US$3 per kilo incentive?

Under the US Inflation Reduction Act (IRA), 45V production tax credits for low-carbon hydrogen can reach up to US$3 per kilo. However, ongoing uncertainty is causing paralysis for project development as rules wait to be passed into law.

Many think the US Treasury’s proposal is too strict and could stifle the industry’s growth. Namely the requirement for green hydrogen to be produced within the same hour as the renewable energy used (‘hourly matching’), which could vastly reduce the number of hours an electrolyser can run.

The market is socializing a selection of amendments with the US Treasury in hopes to achieve middle ground on the tight hourly matching guidance:

- Allowing 100% annual matching for projects online before a given date,

- Delaying the phase-in date of the hourly matching requirement,

- Giving a number of years of exemption for facilities built prior to the hourly matching phase-in date,

- Flexibility to match a percentage of power supply to annual EACs,

- Hourly RECs would allow producers to operate at higher capacity factors.

Rules are rumoured to become statute between June and July. The Biden Administration will target rule finalization before early summer to avoid repeal via the Congressional Review Act. The November election also poses uncertainty and risk for the 18Mtpa of low-carbon hydrogen projects announced in the US.

Learn more

Don’t forget to fill out the form to download your complimentary slides from the presentations. These examine the themes in greater detail and include a range of key charts and data.

You may also want to learn more about how our Lens Hydrogen service can help you plan for the future of the hydrogen economy.