Full steam ahead: the changing outlook for global marine fuels to 2050

Global maritime trade set to grow by more than 40% by mid-century.

4 minute read

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan is responsible for formulating our research outlook and cross-sector perspectives on the global downstream sector.

Latest articles by Alan

-

Opinion

The Hormuz shock: what the data reveals about global oil markets in 2026

-

The Edge

Has the oil price bubble burst?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

The Edge

Ceasefire in the Middle East

Iain Mowat

Principal Analyst, EMEARC Refining and Oil Product Markets

Iain Mowat

Principal Analyst, EMEARC Refining and Oil Product Markets

Iain brings extensive knowledge of global energy markets to his analysis of energy and petroleum demand.

Latest articles by Iain

-

Opinion

Flight path to net zero: aviation’s fuel outlook to 2050

-

Opinion

All hands on deck: the challenge of decarbonising international shipping by 2050

-

Opinion

Trump’s tariff plan: implications for the future of global liquids trade

-

Opinion

Full steam ahead: the changing outlook for global marine fuels to 2050

-

Opinion

Will international shipping be net zero by 2050?

-

Opinion

Decarbonising global shipping

Gordon McManus

Research Director, EMEARC Oils and Refining

Gordon McManus

Research Director, EMEARC Oils and Refining

Gordon is responsible for leading our global coverage of the long term oil products markets.

Latest articles by Gordon

-

Opinion

Flight path to net zero: aviation’s fuel outlook to 2050

-

Opinion

All hands on deck: the challenge of decarbonising international shipping by 2050

-

Opinion

Full steam ahead: the changing outlook for global marine fuels to 2050

-

Opinion

Will international shipping be net zero by 2050?

With global maritime trade set to grow by more than 40% by mid-century, we have analysed the outlook for global marine fuels in the context of International Maritime Organization (IMO) commitments to reduce greenhouse gas (GHG) emissions from international shipping to net zero by around 2050. The IMO target remains a major challenge, requiring a far greater shift to low- and zero-carbon fuels by 2050 than we currently forecast in our base-case outlook.

Fill in the form to receive a complimentary copy of IMO 2050: Outlook for global marine fuels and read on for a taster of the contents.

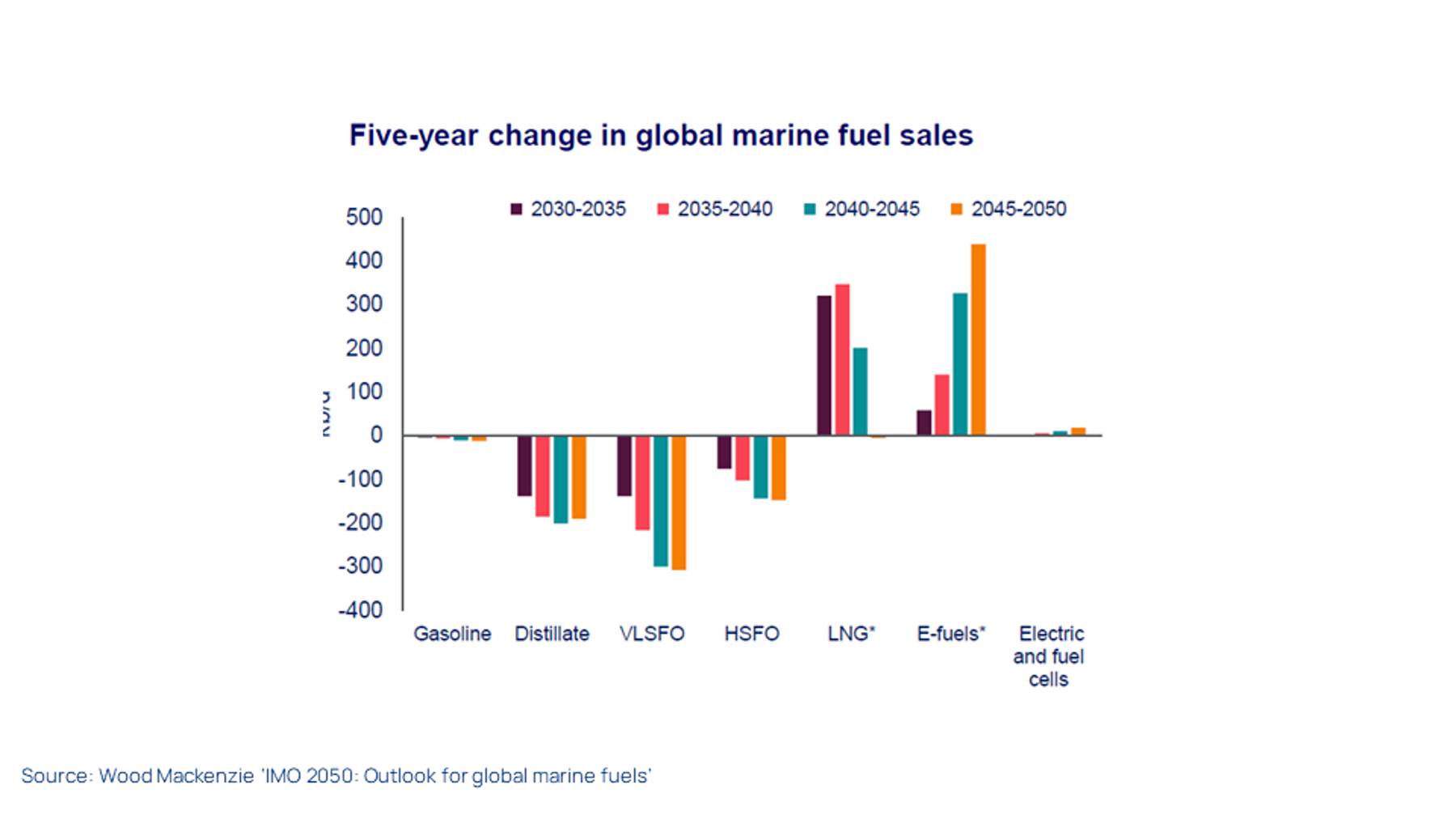

Marine LNG to dominate growth in the coming years

Total global marine fuel sales are expected to grow by 2% between now and 2030, significantly lagging the growth in international maritime trade due to efficiency gains. Marine bunkering in Asia Pacific is set to grow 3 percentage points between now and 2030, increasing its share of the global marine bunker market to 51%.

The global marine fuel market is expected to start declining by the early 2030s as improving fuel efficiency continues to erode demand, despite a forecast 13% increase in maritime trade between now and the end of the decade. International trade in LNG is expected to grow at a much faster rate, although gas carriers will account for a lower volume of trade growth than most other sectors.

Global oil marine bunkers are expected to peak by the mid-2020s at just over 5.3 million barrels per day (b/d). Marine liquified natural gas (LNG) will be the main source of growth over the next few years, displacing just under 0.6 million b/d of oil by 2030.

Growth in marine LNG will slow after 2040 as synthetic fuels, or e-fuels, become more widespread, displacing nearly 1.0 million b/d by 2050, supported by the increasing availability and lower cost of green hydrogen.

EU ETS and FEUM to hike the cost of marine fossil fuels

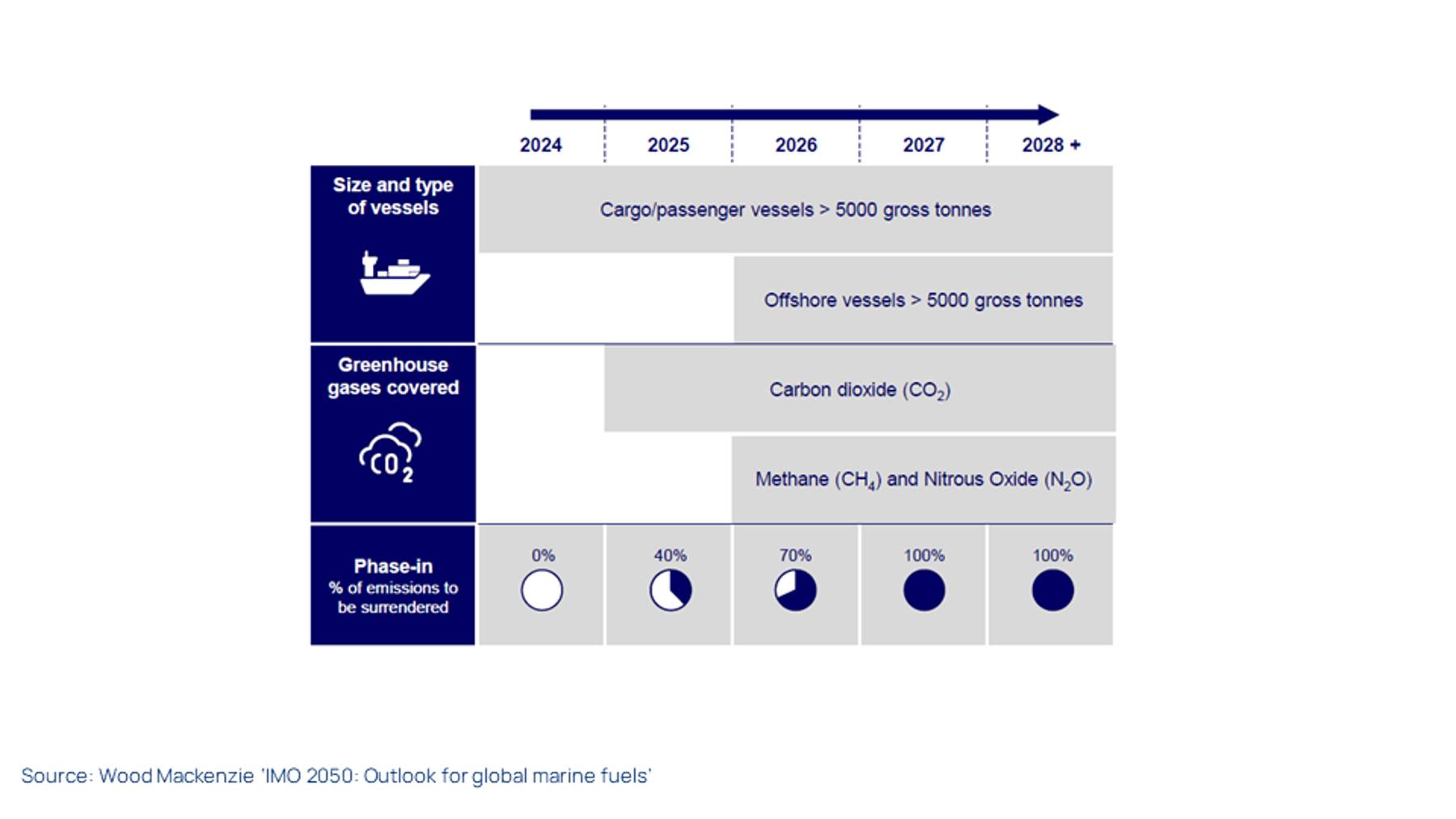

The ramp-up in renewable fuels of a non-biological origin (RFNBOs) will primarily be in Europe, where the inclusion of shipping in the European Union (EU) Emissions Trading Scheme (ETS) and the introduction of the Fuel EU Maritime (FEUM) regulation, will substantially raise the cost of fossil marine fuels.

From 2024, shipping companies operating in the EU are subject to emissions allowances under the EU ETS Directive. Emissions from maritime transport are now included in the overall ETS cap, which indicates the maximum amount of GHG gases permitted under the cap-and-trade scheme. This means that the operating costs of marine transport will increasingly be exposed to emission allowance prices and availability.

The scope of ships and GHGs covered under the ETS will be extended during a phasing-in period that will end in 2028. The system is flag neutral and route based, covering 100% of the tank-to-wake emissions from ships undertaking voyages within EU/EEA member states. Ships travelling between non-EU/EEA states and EU/EEA member states will have to surrender allowances for 50% of their emissions.

{kind=link}

{kind=link}

From 2025, the FEUM regulation will impose a limit on the GHG intensity of the energy used on board ships above 5,000 gross tonnes. GHG intensity limits are defined by a reduction factor applied to the average GHG intensity registered in 2020. The reduction factor increases progressively every five years, from -2% in 2025 to -80% in 2050.

The regulation applies to the average well-to-wake GHG intensity of fleets operating within European ports (EU and EEA). Only 50% of the energy intensity of ships operating between a European and non-European port will be covered. A pooling mechanism forms part of the regulation, so that shipowners can pool the balances of several vessels to comply with the regulation.

Green liquid fuels to gain traction towards mid-century

Of the new generation of low and zero carbon marine fuels, green methanol is the most commercially advanced in terms of supply availability, handling and engine technology for marine applications. E-diesel is attractive as a drop-in fuel, but high costs and limited investment are likely to constrain its availability until the late 2040s. By 2050, the price of green ammonia will be able to displace very low sulphur fuel oil (VLSFO) for all voyages starting or leaving a port in the European Economic Area (EEA).

In our forecast, we prefer e-methanol to e-ammonia due to its easier and less expensive handling and the better alignment with the existing global marine bunkers infrastructure. Research and development in ammonia engines is underway, but global adoption is expected to be slower, as investment in new handling infrastructure is also required. Safety and regulatory hurdles are also much greater for ammonia, something that is likely to slow the adoption of e-ammonia-fuelled vessels.

Be sure to fill in the above form to receive your complimentary copy of our full report.