Discuss your challenges with our solutions experts

Bioenergy: a US$500 billion market opportunity

Policy support is key to unlocking the potential for bioenergy by de-risking aspects of the value chain

4 minute read

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom works on scenario modelling for country and global-level energy mixes across all major energy commodities

Latest articles by Jom

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Middle East

-

Opinion

Energy evolution: navigating the path to a sustainable future

The energy transition is a story of electrification. But rapid electrification can pose huge challenges to heavy industry, reliant on fossil fuels to provide high-temperature heat; and to grid operators, beginning to buckle under the weight of transmission bottlenecks and variable renewables. At the same time, advanced battery technologies are still far from capable of satisfying the stringent performance requirements for the aviation and marine sectors. Bioenergy has emerged as the leading drop-in solution to decarbonise sectors resistant to electrification.

Right now, the bioenergy market is valued at US$44 billion. By 2050, it’s expected to grow to US$125 billion, according to our base case (current trajectory). If the world meets net zero targets by 2050, our energy transition outlook shows that bioenergy could increase to US$500 billion.

{kind=link}

Traditional uses of bioenergy are centred around burning fuelwood for cooking and heating, and producing liquid biofuels for road transport – with possible detrimental effects to the environment and food supply. In contrast, modern bioenergy relies on waste. New technologies can harness residues from farming and forestry to municipal and industrial waste, turning what was once thought to be worthless refuse into renewable, carbon neutral and versatile energy resources.

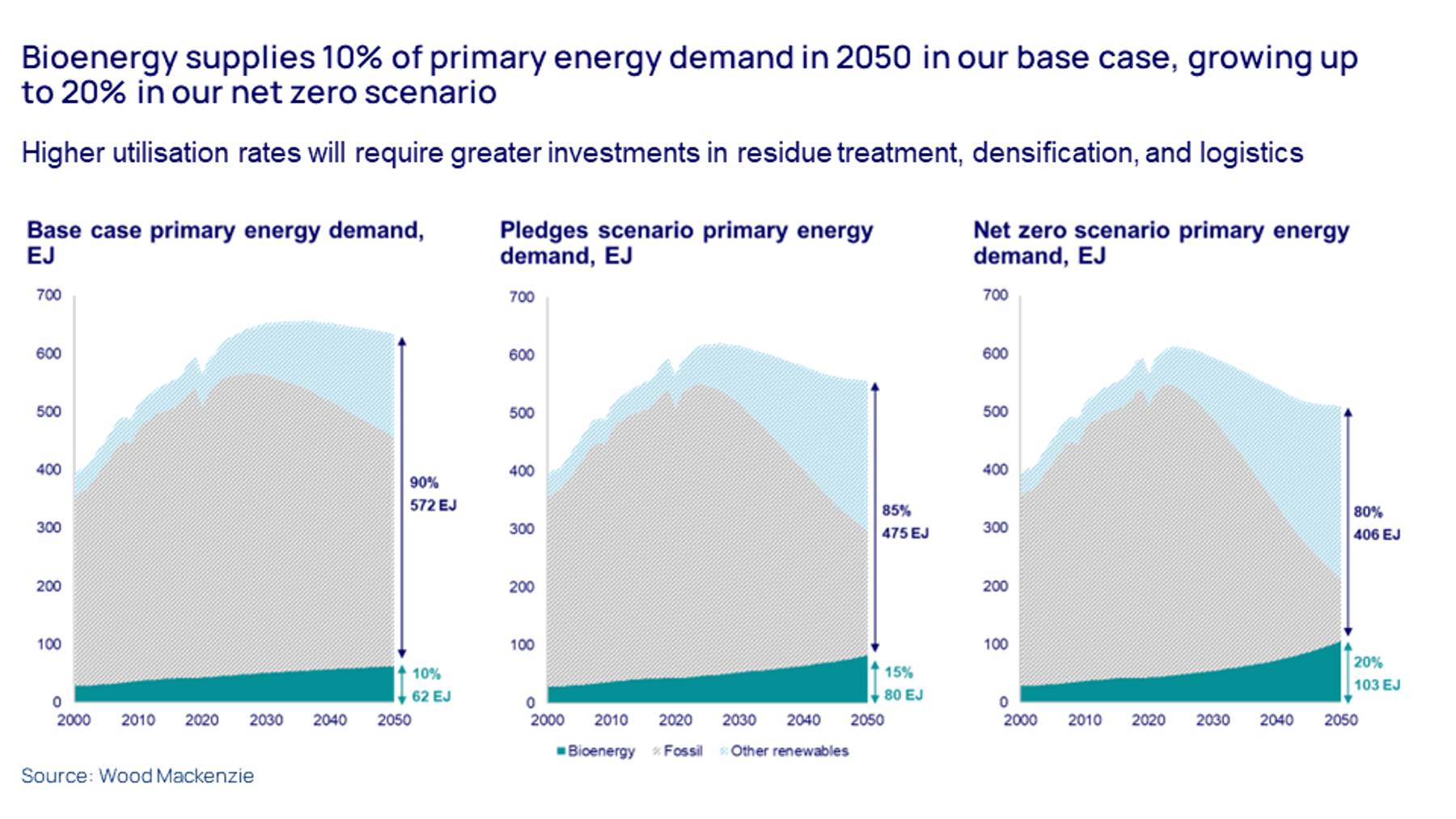

The world currently uses a third of the available resource – 45 exajoules (EJ), equivalent to 7% of global primary energy supply – leaving the remainder unutilised and instead, filling the gap with fossil fuels. In our net zero scenario, we expect it to increase to 103 EJ by 2050, equivalent to 20% of global energy supply, and 59% of the total available bioenergy potential of 175 EJ. That will reduce global emissions by 8.3 Bt CO2, equivalent to 22% of emissions today.

Each source of waste is suited for conversion to different fuels. Solid residues are versatile and allow for the extraction of syngas (a mixture of carbon monoxide and hydrogen); biocrude (a precursor to liquid biofuels); or simply high-temperature heat for use in heavy industry and power generation.

Liquid wastes are suitable for conversion to biogas through anaerobic digestion of livestock waste and wastewater. The biogas can be further upgraded into biomethane, a carbon-neutral fuel chemically identical to its fossil counterpart, natural gas.

Lastly, fat and oil residues alongside energy crops are already commonly converted to bioethanol and biodiesel. These liquid biofuels are usually blended into gasoline and diesel, making up around 10% of global transport fuel supply today.

The problem lies not so much in the demand for these fuels, but rather in the supply. And therein lies the rub

Unlocking bioenergy at scale relies less on technological advances – many pathways are already mature and commercially viable – but primarily on the economics of getting the raw materials delivered in the first place. The bulk of raw residue has little value in its unprocessed state; high transportation costs can often exceed the cargo value. The supply source of these feedstocks is also generally not adjacent to the industries that utilise them.

With solid residues making up 86% of theoretical bioenergy supply, the solution is simple: lower the unit transport cost by removing the air and water fractions in each shipment. These processing technologies are already mature; whether or not it is economically viable depends on local market conditions.

Liquid waste presents a different issue. Any liquids transport would end up hauling mostly water. Instead, liquids-to-energy conversions rely exclusively on existing wastewater infrastructure by building biodigesters near livestock farms or within water treatment facilities.

While renewables are secure in the knowledge that wind will blow and the sun will shine, bioenergy facilities’ reliance on residues leaves it at the mercy of wider headwinds.

Jom Madan

Principal Analyst, Scenarios & Technologies

Jom works on scenario modelling for country and global-level energy mixes across all major energy commodities

Latest articles by Jom

-

Opinion

Energy transition outlook: Americas

-

Opinion

How is energy transition investment evolving in 2026?

-

The Edge

How the Iran war could change energy markets

-

Opinion

Energy transition outlook: Asia Pacific

-

Opinion

Energy transition outlook: Middle East

-

Opinion

Energy evolution: navigating the path to a sustainable future

Despite a promising overall outlook, bioenergy faces scalability challenges. There will always be an upper limit to supply, tied to the amount of waste that other sectors generate. For the residue that is utilised, the feedstock market is unorganised and supply is not guaranteed. While renewables are secure in the knowledge that wind will blow and the sun will shine, bioenergy facilities’ reliance on residues leaves it at the mercy of wider headwinds.

And while in aggregate there is sufficient – if not a glut – of resources waiting to be used, for any individual facility, minor changes in the external operating environment may adversely affect project economics.

In most cases the cost of producing upgraded biomass, biomethane, and biofuels exceeds the cost of fossil-fuel equivalents. In Europe, carbon pricing has brought wood pellets up to price parity with coal and natural gas. However, liquid biofuels face difficult economics, with feedstock costs roughly double the price of crude.

Despite this price premium, bioenergy is still cost-effective in comparison to other advanced decarbonisation pathways, estimated at less than half the cost of hydrogen, carbon capture, and synthetic fuels in 2030.

Market activity is surging on the back of expanded policy support

Policy support is key to unlocking the potential for bioenergy by de-risking aspects of the value chain. Direct financial support through tax credits, enhanced gate fees, and concessionary finance can kickstart adoption, while consumption mandates and carbon pricing can ensure long-term demand.

For example, the EU Sustainable Aviation Fuel (SAF) directive generated a flurry of investment activity in liquid biofuels. The mandate requires 70% of the EU’s jet fuel to come from SAF by 2050 and lists heavy penalties for noncompliance. If this requirement were to be met entirely by biofuels, it would amount to a million barrels of biojet per day.

Value stacking and integration with other industries can generate new revenue streams. Syngas and biocrude are versatile bioenergy products and can be used both as transport fuel and chemical feedstock. Bioenergy carbon capture and sequestration (BECCS) is one of the few technologies that can provide net negative emissions at scale. Biomethane production also yields high-quality organic fertiliser as a byproduct. Aside from its direct benefits, bioenergy offers opportunities for improved waste management and supply security.

For more on our view of the changing energy mix to 2050, explore our energy transition outlook scenarios.

Find out more about our Biomethane/RNG Service

In-depth insight into the biomethane / renewable natural gas (RNG) market to identify opportunities, mitigate risks, and support investment and decarbonisation strategies