The UK’s journey to net zero: an uncertain path ahead

Upstream will play a crucial role in developing clean energy. Policy needs to support this, as well as foster a favourable environment for decarbonisation technologies

4 minute read

Mhairidh Evans

VP, Global Head of CCUS Research

Mhairidh Evans

VP, Global Head of CCUS Research

Mhairidh leads our global research on carbon capture, utilisation and storage (CCUS).

Latest articles by Mhairidh

-

Opinion

Can CCUS help achieve Net Zero?

-

Opinion

Can CCUS momentum overcome headwinds to the industry?

-

Opinion

Carbon management frequently asked questions part 3: CCUS

-

Opinion

The challenges and opportunities in Europe’s oil & gas, CCUS and hydrogen sectors

-

Opinion

Our top five takeaway messages from the CCUS conference 2023

-

Opinion

The UK’s journey to net zero: an uncertain path ahead

Gail Anderson

Research Director, North Sea Upstream

Gail Anderson

Research Director, North Sea Upstream

Gail focuses on the North Sea Upstream industry and its gas and power sector.

Latest articles by Gail

-

Opinion

The energy security opportunity for North Sea oil & gas

-

Opinion

Securing the future of the UK North Sea: a balanced path to net zero

-

Opinion

North Sea upstream: 5 things to look for in 2025

-

Opinion

Video | Shell and Equinor announce UK asset merger to create new JV

-

Opinion

End of an era looms as Chevron seeks UK exit

-

The Edge

Why the transition needs smart upstream taxes

Murray Douglas

Vice President, Hydrogen & Derivatives Research

Murray Douglas

Vice President, Hydrogen & Derivatives Research

Murray is responsible for Wood Mackenzie’s global coverage across the hydrogen value chain.

Latest articles by Murray

-

Editorial

Our biggest takeaways from Wood Mackenzie's Hydrogen Conference 2026

-

Featured

Hydrogen: 5 things to look for in 2026

-

Opinion

eBook | Overcoming the challenges around hydrogen deployment

-

The Edge

Securing offtake for green hydrogen

-

Opinion

Hydrogen: the outlook to 2050

-

Opinion

Our top takeaways from the World Hydrogen Summit

Net zero and decarbonisation are high on the UK’s political agenda. But the pathway is uncertain. With an election looming in 2024, leading political parties are promising clean, cheap and secure energy. However, there is a key difference between their proposals – and the North Sea is an important battleground.

It is a critical time for the industry. Even when net zero becomes a reality, the UK will still rely on oil and gas for its energy needs. Simultaneously, to progress its energy transition, the UK must invest in new and emerging decarbonisation technologies. A thriving upstream sector will be best placed to lead the way, but the policy and fiscal environment need to support this.

In a recent webinar, we tackle the big questions about the future of UK’s upstream and what its route to net zero might look like, while exploring the UK’s potential to maximise investments in the nascent hydrogen and carbon capture, utilisation and storage (CCUS) industries. Fill in the form to watch the replay, or read on for some key themes.

A thriving upstream sector will drive the clean energy transition

The policy environment for the UK’s upstream sector is in a state of flux. The offer of new exploration licence rounds and maximising production from the country’s oil and gas resources both feature in the government’s plans for what it calls a pragmatic energy transition. Meanwhile, opposition parties want the decarbonisation pathway to proceed at a faster pace and with an increased focus on renewables.

The maturity of the UK continental shelf means that the new bid rounds are unlikely to move the needle for the North Sea. Over the past decade, bid round discoveries have accounted for less than 4% of the UK’s remaining reserves.

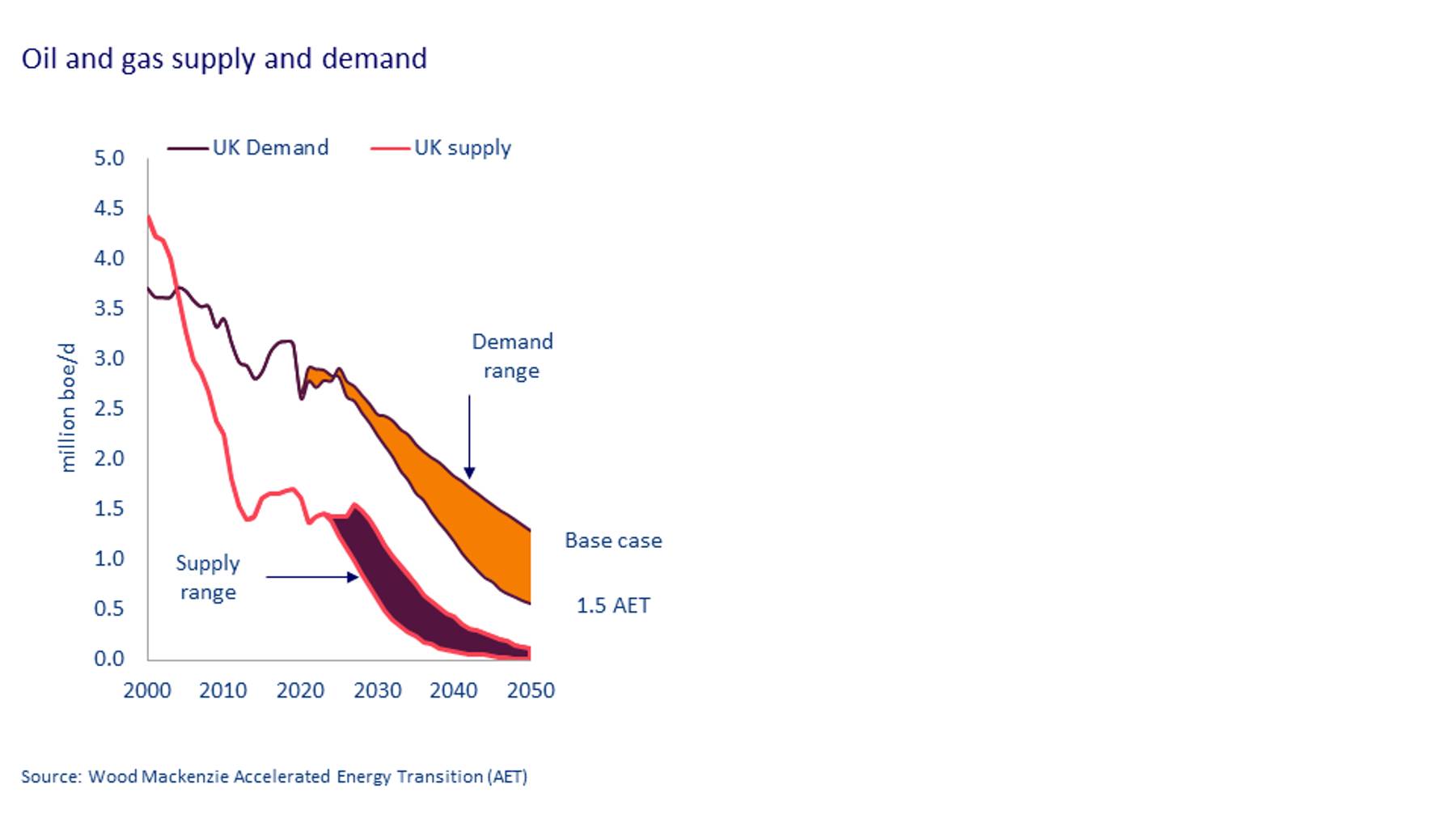

We forecast that the UK could still be consuming as much as 1.3 million boe per day by 2050 – although this will be less in a 1.5-degree accelerated energy transition scenario – leaving it in the position of net oil and gas importer.

So, where will supply come from? The sanctioning of the Rosebank field west of Shetland could be one additional source. However, the project has been controversial as arguments rage about whether it should be allowed to progress given the UK’s net zero commitments. Yet our analysis shows that end-use emissions will be the same, with or without the new field.

Production from the field will be half as emissions intensive as fields elsewhere in the UK and the rest of the world. Without Rosebank, an alternative source of supply, which is likely to be more emissions intensive, will need to be secured to balance the global market.

If bid rounds aren’t the answer, how else can the government support UK upstream?

The UK’s marginal tax rate for upstream has been significantly amended many times over the past 23 years. A more predictable regime would bring greater stability, which would extend beyond upstream to boost the UK’s clean energy sector.

Many of the companies that we rely on to jumpstart low carbon investments are legacy oil and gas producers or are part of an established supply chain. A more holistic fiscal approach to upstream renewables and low carbon projects would incentivise green investments by upstream producers.

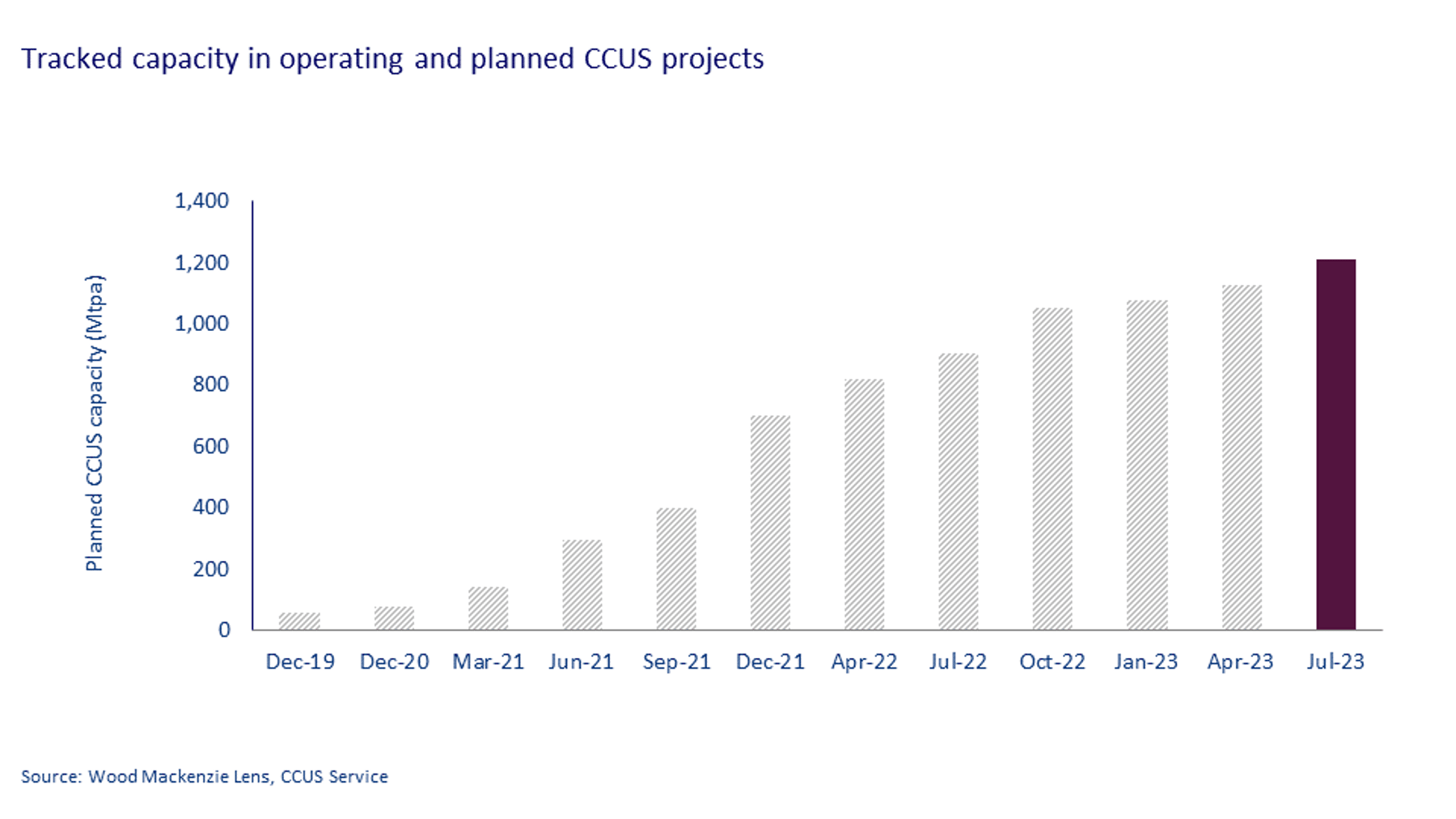

There is momentum behind CCUS, but the UK needs more certainty

Spurred on by the focus on net zero targets, the global pipeline for CCUS projects has grown 13-fold since the beginning of 2020. There are now around 1.3 billion tonnes per annum of capacity planned in projects to capture, transport or store CO2, globally.

{kind=link}

{kind=link}

CCUS technology will play a crucial role in decarbonising many different industries. Although there is huge potential, the industry is immature. In order to make a meaningful contribution to net zero goals, CCUS must scale up – and fast.

To support the industry, there needs to be much greater certainty around policy and funding. Currently, CCUS is a relatively high-cost technology. While it should get cheaper with time, governments need to step in to provide clear funding programmes and policies to incentivise companies to get new projects off the ground.

There is an opportunity for the UK to help establish the industry, with a solid project pipeline in place. However, the ball is firmly in the government's court at the moment to make sure that the funding streams are available for these projects to go ahead.

Listen to our webinar to learn more about our international policy index, which ranks countries’ readiness to adopt CCUS projects. The index takes a number of different factors into account, including net zero targets, carbon pricing, incentives and regulation.

The UK is well placed to compete in an overcrowded hydrogen market

Low-carbon hydrogen opportunities have emerged rapidly across the globe and the pipeline continues to grow in scale and diversity. While the USA leads in announced capacity, spurred on by generous subsidies and policy support such as the Inflation Reduction Act, the UK retains a sizeable share of the global pipeline.

Although there is a large project pipeline, it is unclear whether policy support will be sufficient to meet ambitious production targets. However, the UK policy environment has been supportive, setting it up for success. Learn more about how UK policy stacks up internationally in our policy readiness index, which we discuss in more detail on our webinar.

Track the UK’s journey to net zero

Watch the webinar replay for a detailed analysis of the future of upstream and its role in the UK’s road to net zero. It includes charts and data on global hydrogen and CCUS capacity, project pipelines and more.

Fill in the form on the top of the page for your complimentary access.