Sign up today to get the best of our expert insight in your inbox.

Can carbon offsets deliver for oil and gas companies?

Higher-quality projects are required to drive the sector forwards

4 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

View Simon Flowers's full profile

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Nuomin Han

Principal Analyst, Head of Carbon Markets

Nuomin Han

Principal Analyst, Head of Carbon Markets

Nuomin provides clients with insights into emissions and climate-related development.

Latest articles by Nuomin

-

Opinion

Flight path to net zero: aviation’s fuel outlook to 2050

-

Opinion

The forces shaping the future of carbon management

-

Opinion

Carbon markets Q2 update: policy shifts and market evolution

-

Opinion

Forecasting carbon offset use to 2050: what you need to know

-

Opinion

4 key carbon policy developments from Q1 2025

-

Featured

Carbon markets 2025 outlook

A slower energy transition poses a conundrum for oil and gas companies. Stronger fossil fuel demand is positive for balance sheets but magnifies the challenge of emissions reduction.

With companies across all sectors struggling to neutralise hard-to-abate emissions, carbon offsets offer an additional string to the decarbonisation bow. Many oil and gas companies will depend on offsets to achieve net zero, and the industry is already buying offsets and increasingly developing offset projects, acquiring offset companies and establishing partnerships with offset project developers.

But the sector faces numerous challenges. The key rules for a global carbon market remain undefined, project quality must improve, and offsets remain tarnished by cries of greenwashing.

Can carbon offsets offer oil and gas companies a credible decarbonisation option at scale? Gavin Thompson, Vice Chair EMEA, spoke to Nuomin Han, Head of Carbon Markets.

What kind of carbon offsets are there?

Carbon offsets are generated by two kinds of projects – those that reduce or avoid emissions and those that remove and store legacy CO2 from the atmosphere. Projects can be either nature- or technology-based and range in size from micro-grid solar panels to mega dams.

While emissions reduction projects make up the lion’s share of the existing carbon offset inventory, investment in carbon removal is increasing, with engineered projects employed in tandem with other abatement options. Technology-based solutions counterbalance accumulated emissions and, where these require geological storage, allow oil and gas companies to bring their subsurface expertise into play.

How are the offsets quantified and utilised?

Third-party auditors are required to evaluate levels of emissions mitigated and issue corresponding tradeable offsets that can be sold on the voluntary carbon market. Once purchased, companies have three options to use carbon offsets: for their own decarbonisation needs, to compensate for emissions along their value chain or as financial instruments.

What challenges must be overcome?

The voluntary carbon market has grown rapidly but faces three main obstacles to becoming a net zero tool of scale.

First, defining the rules for a global carbon market. Optimism that COP28 would finalise Article 6 of the Paris Agreement to deliver a new carbon credit mechanism proved unfounded. An agreement would have paved the way for a robust UN-backed global carbon market and supported the voluntary carbon market by creating certainty for private sector investment.

In the meantime, the growing demand for high-quality offsets means future projects must strengthen their credentials for avoidance or removal of carbon emissions. Independent regulation is advancing. Reputable bodies are improving the guidance for project developers on what constitutes high-quality offset projects and providing clarity on offset choices for buyers.

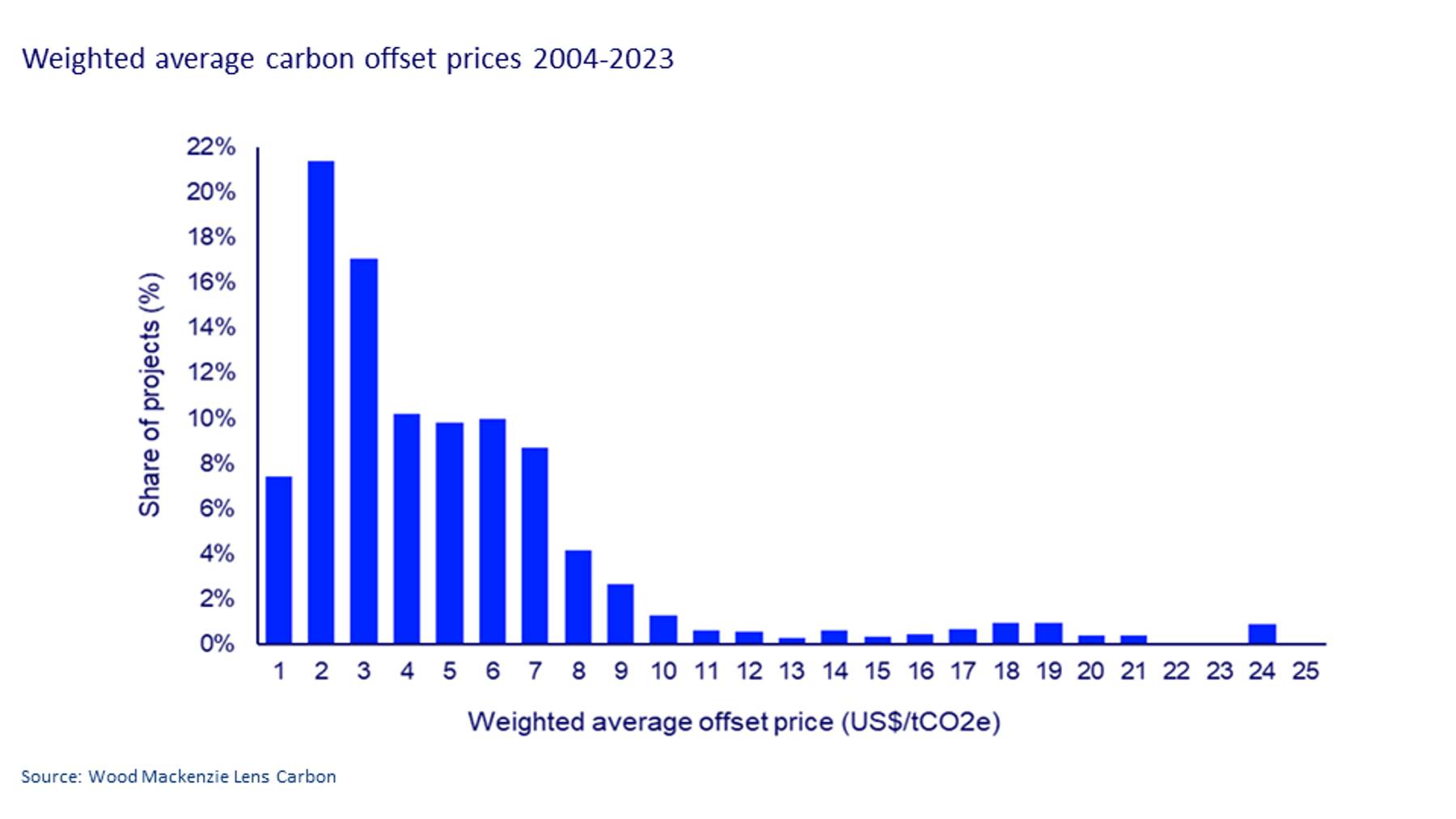

Second, realising the full value of carbon offsets. Almost two-thirds of offset projects received a price below US$5/tCO2e, a reflection of their limited value in offsetting emissions and reputational risk to buyers. Without recognised measurement and verification, project developers will struggle to convince buyers their offsets will permanently remove or avoid carbon emissions – and, thus, achieve higher prices.

Project developers must also focus on the non-climate value of their offsets. The market is increasingly rewarding projects that can prove their sustainable development credentials, including benefitting biodiversity and local communities.

Third, building public confidence in carbon offsets. Environmental groups have long opposed carbon offsetting on the basis that offsets divert attention from efforts to reduce emissions in the first place. Oil and gas companies buying offsets from the voluntary carbon market are criticised for ‘laundering’ their actual emissions through buying cheap credits rather than implementing real carbon mitigation solutions. Higher-quality, higher-priced offsets will address this.

Where next for carbon offsets?

Despite these challenges, offsets can prove an effective tool for oil and gas companies. Offsetting carbon emissions offers an additional pathway when mitigation options alone are insufficient to deliver net zero and are also used by oil and gas companies to provide customers with an option to compensate for their emissions.

The European Majors are leading the charge. TotalEnergies aims to build up 100 million carbon credits from 2030, as well as offsetting 10 Mt of residual scope 1 and 2 emissions by 2050 with nature-based solutions. Eni is planning for around 25 Mtpa of offsets by 2050 and Shell and BP have also announced that carbon offsets are a key part of meeting their emissions reduction targets.

Improving the global governance of carbon offsets is critical to delivering this level of ambition. With greater project accountability, high-quality credits can support the oil and gas industry’s push towards net zero. They will also support higher prices: we expect offsets to exceed US$50/tonne by the end of the decade if regulation keeps pace with demand.

Looking to the long term, carbon offsets also offer the opportunity to help tackle scope 3 emissions. With a slower energy transition, high-quality carbon offsets can be a potent weapon in the ultimate battle to achieve net zero.

{kind=link}