What E&P firms need to know about the future of carbon offsets

As the voluntary carbon market refocuses on quality over quantity, the oil and gas sector must take a proactive approach to credit procurement

1 minute read

Michelle Uriarte-Ruiz

Senior Research Analyst, Carbon Offsets Valuations

Michelle Uriarte-Ruiz

Senior Research Analyst, Carbon Offsets Valuations

Michelle is part of the carbon team, providing clients with insights and analysis of carbon offset projects.

Latest articles by Michelle

-

Opinion

Four carbon policy developments set to impact E&P decision-making in H2

-

Opinion

4 carbon policy developments that impact E&P decision-making

-

Opinion

What E&P firms need to know about the future of carbon offsets

-

Opinion

Middle East tensions: a litmus test for carbon market resilience, not transition momentum

-

Opinion

The forces shaping the future of carbon management

-

Opinion

Forecasting carbon offset use to 2050: what you need to know

As a key factor for long-term risk management and competitiveness, emissions are not merely an ESG issue but a strategic portfolio and capital allocation challenge. For energy-intensive industries like oil and gas, carbon offsetting is therefore invaluable as a means of compensating for hard-to-abate emissions that are integral to the production process.

Ambitious climate commitments and resulting strong interest in carbon offsetting saw a past focus on quantity over quality, damaging the credibility of the voluntary carbon market and impacting its growth. Yet for oil and gas exploration and production (E&P) firms, the need for carbon offsets remains. In an increasingly scrutinised market, what do decision-makers need to know to be confident of the credibility and quality of the carbon credits they purchase?

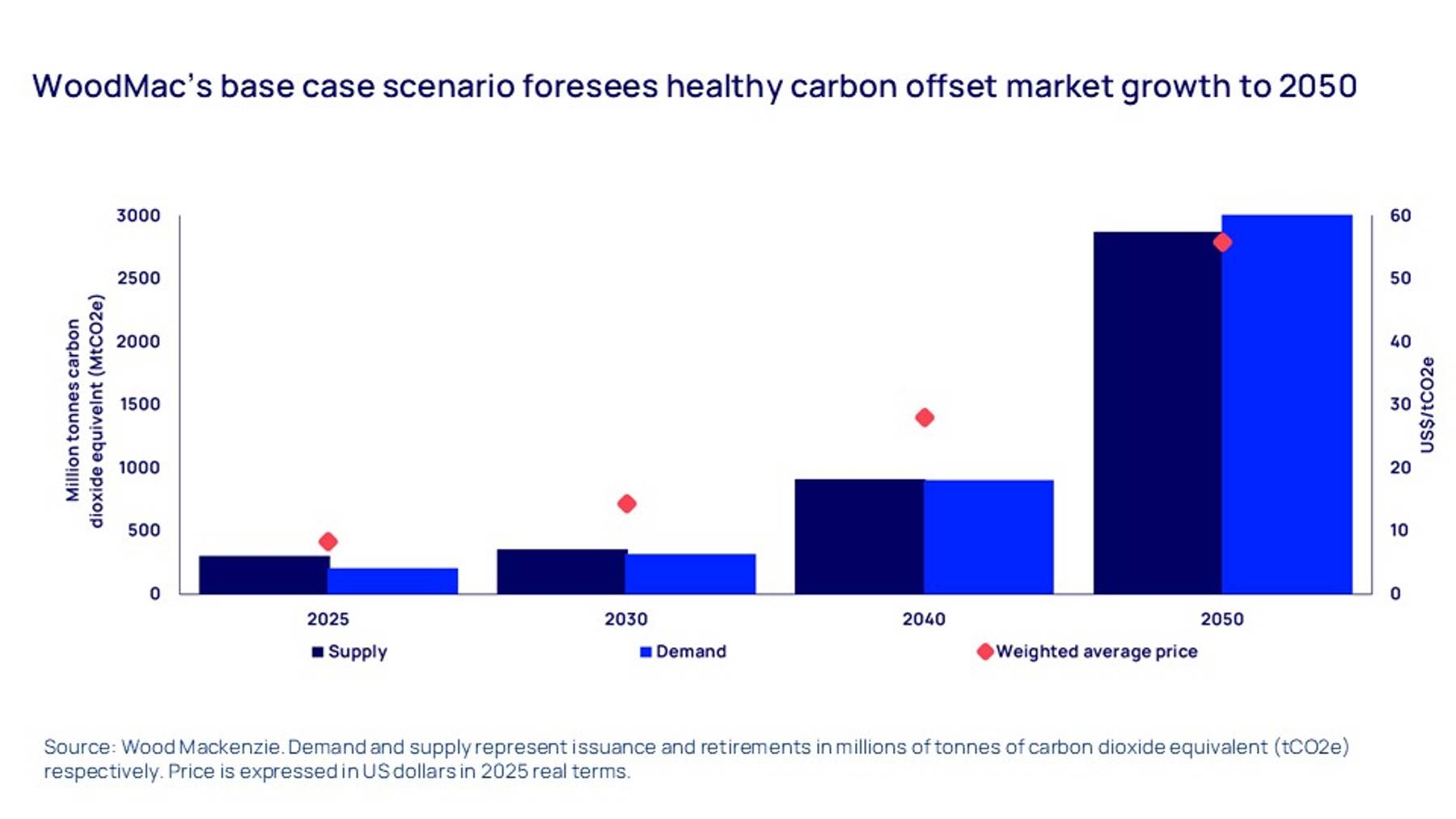

The voluntary carbon market has strong long-term growth potential

Despite recent market retrenchment, there is no doubt of the strong latent demand for carbon offsetting from hard-to-abate sectors. Research carried out by WoodMac’s expert analysts using our Lens Emissions data and analytics platform forecasts the voluntary carbon market could grow at an average annual rate of 11% between 2025 and 2050. However, this will be dependent on the market’s ability to maintain transparency, strengthen governance and align supply with high quality standards.

A maturing carbon market is focusing on high-quality frameworks and credit integrity

Lower voluntary carbon market volumes since 2022 reflect a shift in priorities, with buyers now placing stronger emphasis on the credibility and quality of the carbon offsets they purchase. Methodologies, verification and UN Sustainable Development Goal (SDG) indicators have long supported the market for carbon offsets; however, new initiatives are focusing on rebuilding trust by defining common quality standards and addressing past integrity gaps, guiding buyers towards higher-integrity credit.

Two pioneering frameworks are taking a key role in shaping buyer expectations:

- CORSIA: The International Civil Aviation Organization’s Carbon Offsetting and Reduction Scheme for International Aviation defines which credits airlines can use to offset international flight emissions — it is the first global market-based scheme to apply across a sector

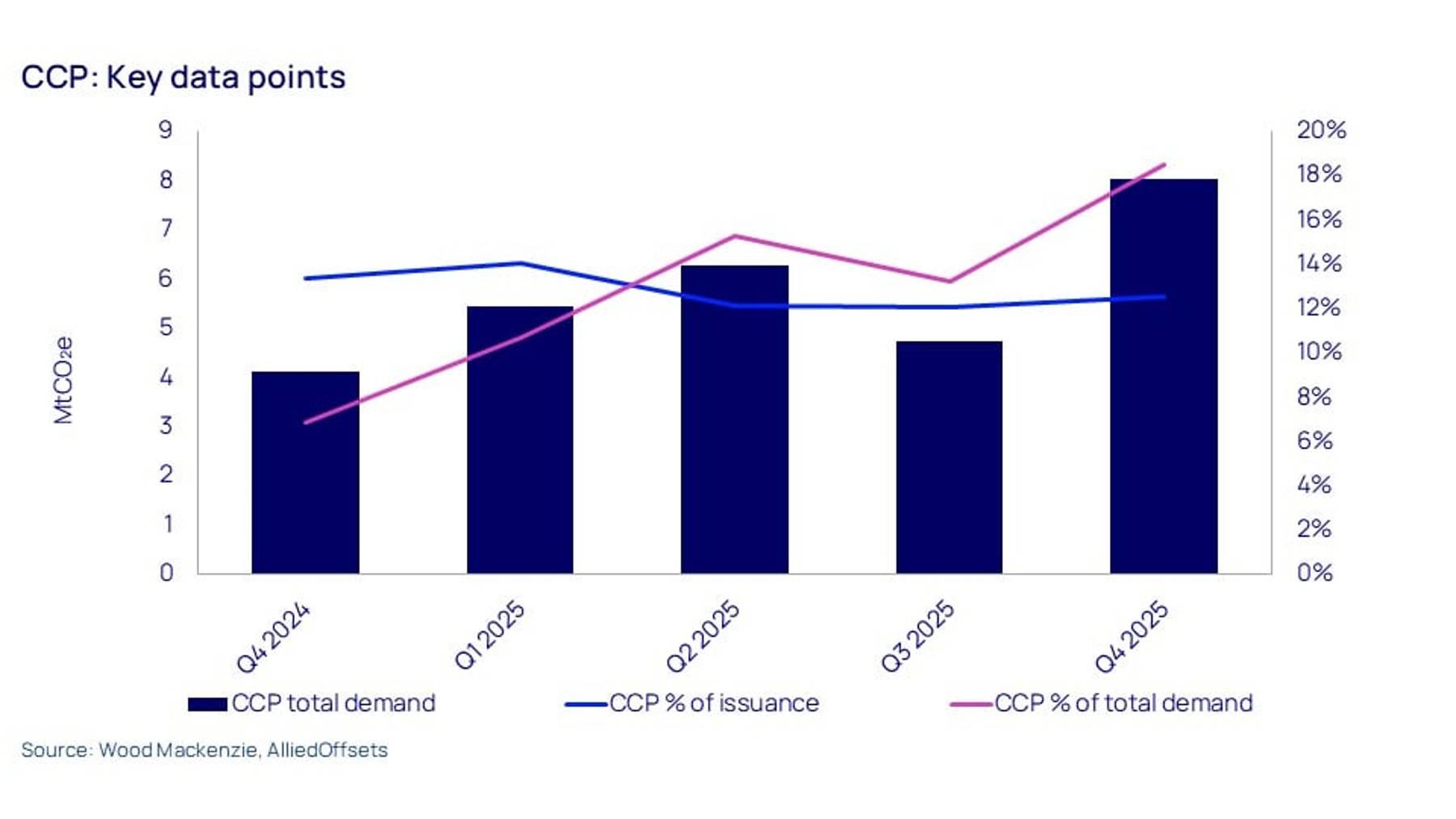

- CCP: Set by the Integrity Council for the Voluntary Carbon Market (ICVCM), the Core Carbon Principles are described as ‘ten fundamental, science-based principles for identifying high-quality carbon credits that create real, verifiable climate impact’

CORSIA has established a baseline for integrity, ensuring transparency, monitoring, reporting and verification (MRV), and governance. CCP builds on this foundation by applying deeper quality checks at the methodology level, addressing key issues such as additionality, over-crediting, leakage and permanence.

Third-party ratings agencies’ project-level assessments complement frameworks

To complement these macro frameworks and labels, third-party agencies offer more granular assessments at an individual project level, focusing on risk and quality and typically providing a rating from AAA to D. These ratings can act as a due diligence shortcut for businesses, adding confidence and protecting reputation while reducing the internal resources required.

These agencies increasingly use rigorous, project-specific methodologies that combine geospatial, financial and science-based analysis, enabling buyers to benchmark and compare offsetting projects. However, to date, coverage is still partial and fragmented, with no uniform rating standard.

E&P firms should take three key steps to adapt their carbon offsetting strategies

Regulatory momentum is building, with compliance integration accelerating the adoption of eligible carbon credits. This is slowly leading to price differentiation for higher-quality products in some (but not yet all) sectors.

{kind=link}

{kind=link}

{kind=link}

As the market evolves, E&P firms need to proactively adapt their credit procurement strategies to balance three key factors: assurance, cost and control:

- Adopt a layered approach: combine CORSIA and CCP eligibility with third-party ratings for improved risk management

- Secure supply early: Anticipate scarcity and lock in high-quality credits via offtake agreements

- Budget for quality: Account for price differentiation on eligible credits versus non-eligible alternatives

To position their businesses for success, E&P decision-makers need to build effective carbon credit procurement pipelines, expanding their supplier due diligence and hedging long-term price risk with forward contracts.

Confident, defensible decisions must be based on competitive benchmarking, portfolio analysis and economic impact assessment across the value chain. Why not find out more about how Wood Mackenzie’s Lens Emissions solution can help.

Don’t forget to fill out the form and download the report extract, which covers the carbon offset market’s quality transformation in detail, including:

- A detailed comparison of quality checks by CORSIA, CCP and third-party agencies versus the voluntary carbon market baseline

- Pros and cons of assurance frameworks and third-party ratings

- How CCP- and CORSIA-certified credits are reshaping issuance and retirements

- How CCP approvals strengthen credibility and drive price differentiation for forestry and land-use credit