Sign up today to get the best of our expert insight in your inbox.

Unlocking the potential of white hydrogen

Oil and gas company expertise holds the key

3 minute read

Simon Flowers

Chairman, Chief Analyst

Simon Flowers

Chairman, Chief Analyst

Simon is our Chief Analyst; he provides thought leadership on the trends and innovations shaping the energy industry.

Latest articles by Simon

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Oil and gas markets’ perilous dilemma

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

Kate Adie

Research Analyst, Subsurface

Kate Adie

Research Analyst, Subsurface

Kate is a key contributor to our global research on established and developing geoenergy technologies.

Latest articles by Kate

-

The Edge

Can natural hydrogen deliver its potential?

-

Opinion

Hot rocks: geothermal momentum continues to build

-

Opinion

Rock solid: geothermal’s upward trajectory

-

The Edge

The coming geothermal age

-

Opinion

Heating up: 2024 showcased the promise of geothermal energy

-

Featured

Subsurface 2025 outlook

Richard Hood

Senior Research Manager, Subsurface

Richard Hood

Senior Research Manager, Subsurface

Richard leads the New Energies research within our Subsurface team, working to help clients assess new opportunities.

Latest articles by Richard

View Richard Hood 's full profileFaced with high costs, midstream transportation challenges and the slow development of demand, the low-carbon hydrogen economy is facing lowered expectations around its growth in the near term.

Developers and consumers continue to explore alternative forms of low-carbon hydrogen. White hydrogen’s superpower is that – unlike alternatives such as green or blue, which require inefficient conversion processes – it comes ready-made and at a much lower cost. And with their exploration and development expertise, oil and gas companies are well-placed to become champions of this emerging low-carbon molecule.

Gavin Thompson, Vice Chair, EMEA, spoke to Richard Hood and Kate Adie from our Subsurface research team, authors of our recent analysis of white hydrogen’s potential.

What is white hydrogen?

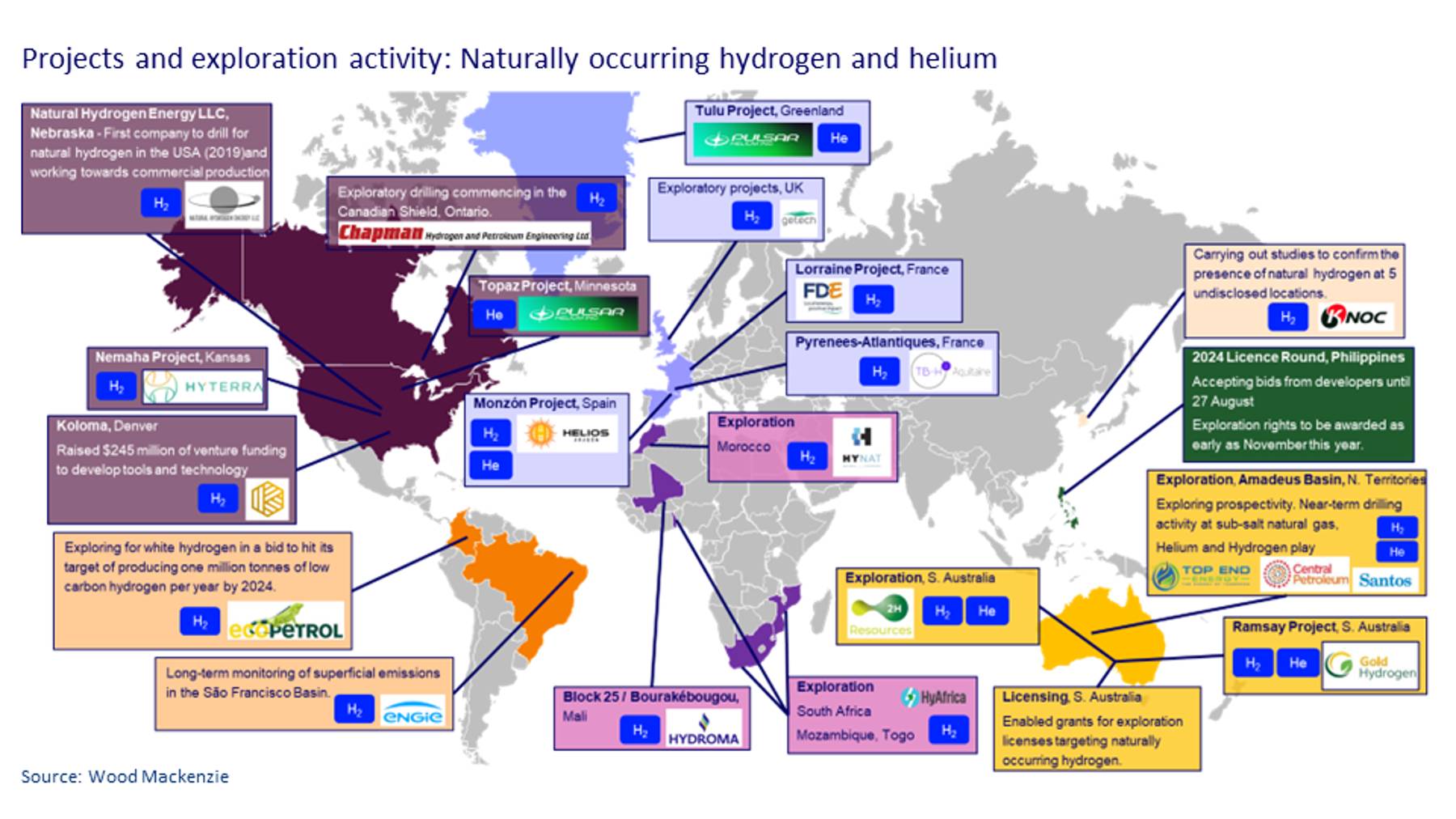

Like oil and gas, white hydrogen is naturally occurring. Generated by continuous geochemical reactions in hard rock, white hydrogen’s characteristics differ from hydrocarbon molecules in that they are small and light, and more likely to escape cap rocks. More research is still required, with practical field experience and data collection needed to establish the key components of a hydrogen play.

Why is white hydrogen generating interest right now?

The world needs low-carbon hydrogen to decarbonise. Global low-carbon hydrogen demand is forecast to reach almost 200 Mtpa by 2050, up from 1 Mtpa today in WoodMac’s base case, with green hydrogen supply meeting the bulk of this future demand. Green hydrogen’s production costs, though, remain stubbornly high with a range as wide as US$6/kg to US$12/kg. This is driven by green hydrogen’s need for high availability of renewable power for electrolysis. It will also depend for years on substantial subsidies to work towards a commercial threshold in the range of US$3/kg.

White hydrogen offers a much cheaper alternative resource. Without the need for inefficient energy conversion or manufacturing processes, white hydrogen produced at scale from reservoirs sited close to end-user markets could be delivered well below US$1/kg. The co-existence of helium may also offer a valuable commercial lever for white hydrogen exploitation.

How significant an energy source could white hydrogen become?

White hydrogen is not an energy transition panacea. Currently, we estimate alternative forms of low-carbon hydrogen production – including methane pyrolysis, gasification and the extraction of naturally occurring white hydrogen – combined will form only a small portion of future supply.

This outlook may change in the coming decade if successful pilot projects prove technical and commercial feasibility and supportive policy frameworks are introduced. Based on prospective resource volumes, we estimate white hydrogen production could reach 17 Mtpa by 2050. Capturing similar levels of subsidy support to green hydrogen would also provide a significant boost to infrastructure, displacing some higher-cost manufactured hydrogen production.

Who is involved?

The industry is truly nascent. A handful of innovators, backed through private investment, are leading the way in trying to understand the prospective resource. To date, the only operational white hydrogen project is the Bourakébougou field in Mali, delivering electricity to a small village.

Globally, some countries are considering the opportunity to develop white hydrogen, enabling exploration-led activity through amendments to existing petroleum and mining codes. But regulating the unknown is never straightforward. In Europe, France has led the way in recognising the potential of white hydrogen, modifying its mining code as a result, whereas the German government has announced it sees no extraction opportunity in naturally occurring hydrogen.

Can oil and gas companies lead the way?

With significant work needed to gain a full technical understanding of how hydrogen molecules are generated and stored in the subsurface, petroleum industry techniques are critical to unlocking white hydrogen.

With their subsurface expertise, white hydrogen should hit the sweet spot for oil and gas companies. Given the right regulations and incentives, governments could enable exploration opportunities for these companies and kick-start the sector. Block licensing, exploration and appraisal drilling and fiscal terms could broadly mirror those for oil and gas.

Oil and gas companies also have the capital to drive white hydrogen forward, just as they are doing with CCUS. This could prove transformational, as even the most advanced white hydrogen projects being led by small privately backed startups still lack firm timeframes to FID and face significant obstacles.

Still unproven, white hydrogen has the potential to form part of the future portfolio of low-carbon molecules for some oil and gas companies, which will also include biomethane, e-methane, blue and green hydrogen and its derivatives. Indeed, white hydrogen would likely displace some blue and green developments. Technology, capital and regulation hold the key.

{kind=link}

Make sure you get The Edge

Every week in The Edge, Simon Flowers curates unique insight into the hottest topics in the energy and natural resources world.