Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Global PV tracker shipments grew by 28% in 2023 to 92 GWdc

The US region saw 10% YoY increase to more than 37 GWdc of shipments in 2023

1 minute read

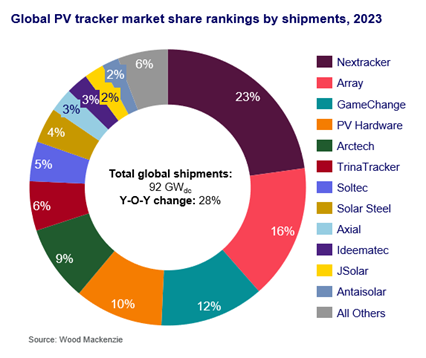

Global PV tracker shipments grew by 28% in 2023 to 92 gigawatts direct current (GWdc), reflecting a strong year for utility-scale solar in most regions across the world. The top ten vendors accounted for 90% of the global market share, according to Wood Mackenzie’s ‘Global solar PV tracker market share’ report 2024.

For the ninth consecutive year, Nextracker and Array Technologies continued to lead the market, taking the first and second positions in the global tracker market, respectively. They were followed by GameChange Solar who made it to #3 in the rankings for the first time.

Nextracker extended its lead over Array with 20% annual growth, while GameChange achieved an impressive 55% growth to close the gap between second and third positions. These three US-based manufacturers combined for more than 50% of global tracker shipments and 90% of the United States market.

The United States, the largest individual market for PV trackers, experienced a 10% year-over-year (YoY) increase to over 37 GWdc of shipments in 2023. This was helped by Inflation Reduction Act incentives which kickstarted construction for many new large-scale projects across the country, according to the report.

In Europe, Spain was the largest market in the region with more than 50% of the continent’s demand. PV Hardware (PVH) ranked first in shipments for Europe and second in Spain behind Solar Steel. The two vendors were joined in the global top 10 by two other Spanish manufacturers, Soltec and Axial. All these companies capitalised on both domestic and international demand, particularly in the rest of Europe and Latin America.

By contrast, the PV tracker market in China fell to 4.3 GWdc in 2023, despite the country exceeding 140 GWdc of utility-scale solar installations in 2023. Instead, Chinese manufacturers experienced much higher demand for fixed-tilt products, as low installation costs were a main driver for developers in China.

Despite this drop in Chinese demand, TrinaTracker and Arctech still rose into the global top six by expanding their regional presence in the Middle East, central Asia, and Latin America.

ENDS

Reporting metrics:

Market shares are determined by trackers shipped in megawatts (MWdc) as defined by the DC capacity of the supplied project. Shipments are determined by the date on which product is delivered to the project site, title/risk is transferred, and revenue is recognized by the vendor.