Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980 -

BIG PartnershipWoodMac@BigPartnership.co.uk

UK-based PR agency

Global policy support for nuclear expands to address challenges of reliable, low-carbon energy supplies

New technologies driving down costs to make nuclear competitive with other low carbon power technologies

3 minute read

As nations look for more low-carbon energy supplies, many are adjusting energy policies to support new nuclear projects and developing new technologies that will make this energy source more cost-competitive, according to a new report from Wood Mackenzie.

“Critical to long-term net zero emissions pathways, nuclear power also addresses several challenges facing the world today – the need for reliable, low-carbon energy supply,” said David Brown, director, Energy Transition Service for Wood Mackenzie. “Nuclear is a key part of addressing the energy trilemma, by limiting the role of higher cost marginal supply sources, such as natural gas.”

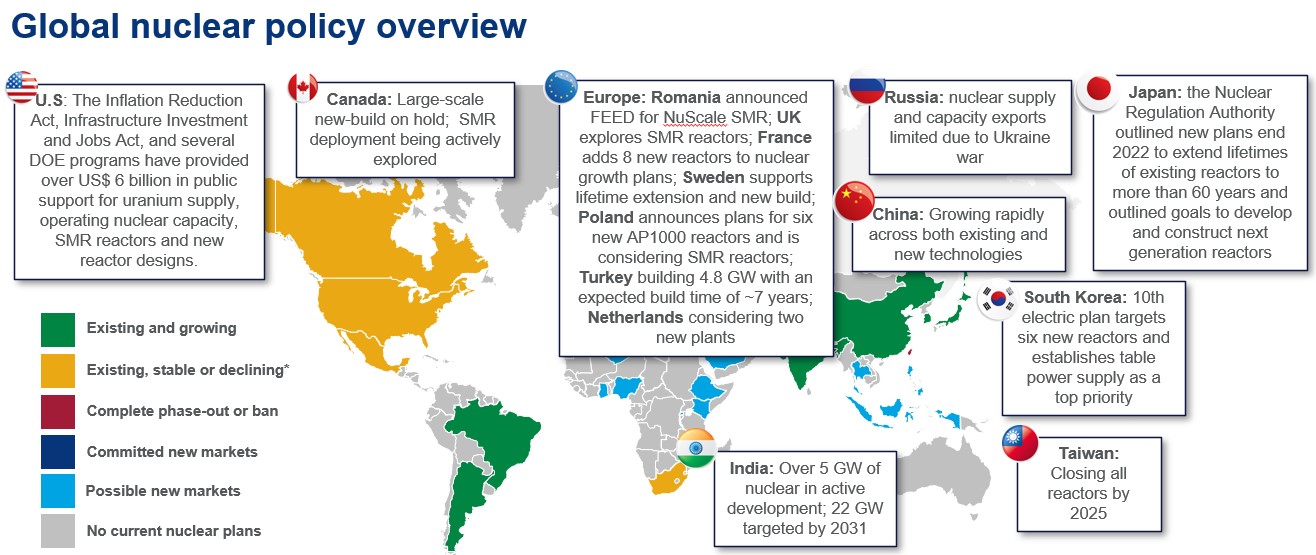

According to the report “Investing in the future of advanced nuclear” policy support has expanded in markets with 50% of global nuclear capacity as of 2022. The United States recently received $6 billion in public support, while other nations such as India, Japan and especially China will continue to expand support and grow capacity.

“Investment in conventional and emerging nuclear technologies will need to expand,” said Brown. “Currently, 75 percent of nuclear capacity was built between 1970-1990, most of it in the US and Europe. New reactors with innovative technologies must be brought online, with the dual target of delivering more low-carbon energies at a competitive price point.”

Nuclear sector innovation

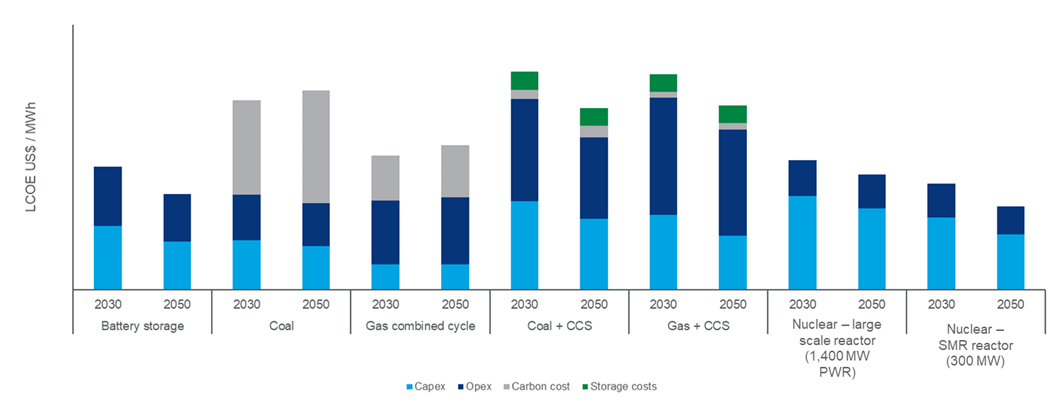

According to the report, investments in advanced nuclear, such as small modular reactors (SMR) and new reactor technologies could lower costs, improve time to market and make nuclear a viable competitor with renewables.

“We project that by 2030, SMR costs can fall quickly to be competitive with abated thermal capacity,” said Brown. “By 2050, SMR costs could fall even further to be competitive with thermal capacity.”

Levelized cost of electricity (LCOE) comparison ($/MWh) – average values for Europe

Uranium requirements expand

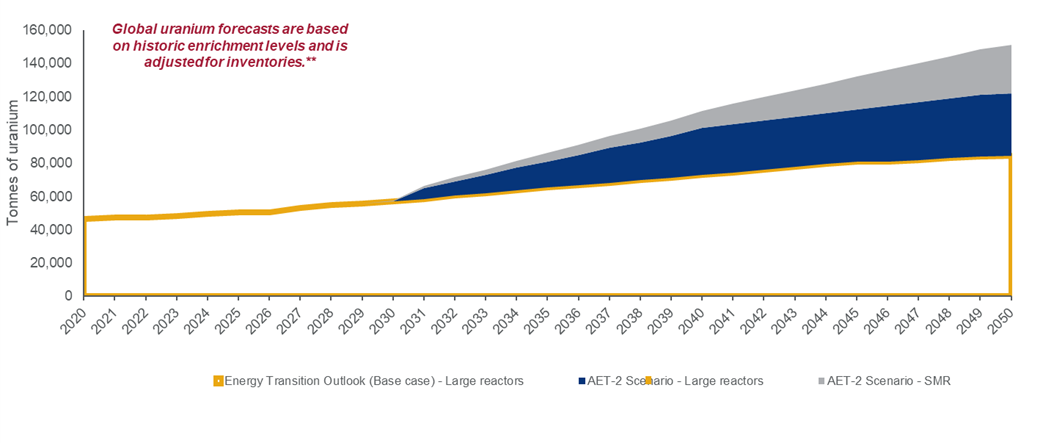

With growth in nuclear capacity will also come more demand for uranium. Wood Mackenzie projects that demand will remain flat until 2030, but then nearly double to meet its ETO outlook, and triple to meet its AET-2 scenario, which is consistent with a 2 C warming trajectory by 2050. There is enough uranium to meet this demand, but countries that rely on sources from Russia may find additional challenges.

Global uranium fuel requirements (2020-2050)

Added Brown, “Russia’s invasion of Ukraine will put additional focus on the fuel cycle. Europe and the other markets that rely on Russian uranium will seek to maximise the use of spent nuclear fuel and procure new uranium supply at the lowest possible cost. Considerations such as plant age, utilisation, uranium availability and the energy density of recycled and new uranium all influence supply optimisation.”

Nuclear renaissance: possible but challenging

Beyond addressing competitive costs and innovation, nuclear has other hurdles to overcome. Continued operations safety, faster regulatory reviews, and continued grid expansion are several priority areas that the nuclear industry and national governments need to address.

“The energy industry has a track record of technological breakthroughs during periods of high commodity prices and strong policy support,” said Brown. “If these areas are addressed, a renaissance is possible.”

WM ETO: Wood Mackenzie’s Energy Transition Outlook is consistent with 2.5 C warming trajectory by 2050. This will be driven by the advancement of current and nascent technologies, as well as the evolution of current policies. This dataset is aligned to our Strategic Planning Outlook (SPO) released in Q1 – Q2 2022.

WM AET-2: Wood Mackenzie’s Global Pledges Case Scenario

(WM AET-2) is consistent with a warming trajectory below 2 ˚C warming. It is aligned with net zero pledges announced in the run up to COP27. It incorporates policy response to the current energy crisis, and geopolitical challenges facing global economy