Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

US community solar surpasses 10 GW milestone in 2025 despite tightening market conditions, according to Wood Mackenzie

1 minute read

Expected national growth to be 12% in 2026; Subscriber acquisition costs decline 12% on average in 2025; community-scale solar potential exceeds 12 GW through 2030

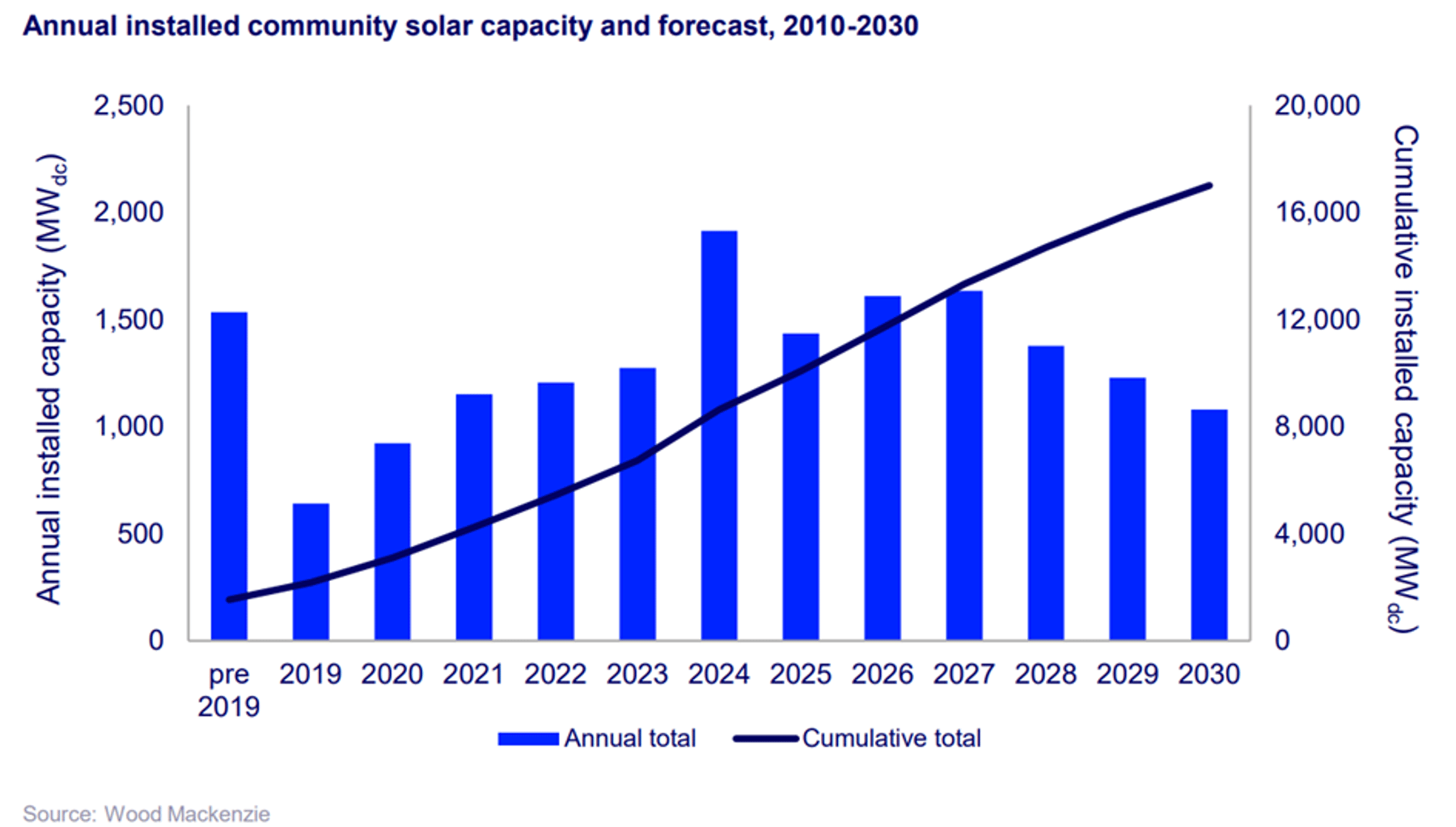

The US community solar sector reached a historic milestone in late 2025, officially surpassing 10 gigawatts (GWdc) of cumulative national installations, according to a new report released by Wood Mackenzie in collaboration with the Coalition for Community Solar Access (CCSA).

While the market experienced a 25% contraction in 2025 due to a slowdown in mature markets like New York and Maine, national installed capacity is expected to rebound with 12% growth in 2026. The market installed 1,435 MWdc in 2025.

{kind=link}

“Overall, we expect national installed community solar capacity will contract by an average of 5% annually through 2030 in existing state-level programs,” said Caitlin Connelly, senior analyst and lead author of the report. “The segment’s near-term growth is anchored by a strong project development pipeline that now exceeds 8 GWdc, 29% of which is reported to be under construction. Developers are navigating a complex federal policy landscape and interconnection queue backlogs to ensure their current pipelines are built out as efficiently as possible to meet the start-of-construction and placed-in-service deadlines required to secure the ITC.”

Proposed Programs Add Upside Potential Pending Implementation Timelines

According to the report, the market contraction in 2025 was primarily driven by low installation volumes in New York and Maine. This year, capacity additions in Illinois and Mid-Atlantic markets will drive national annual growth.

The long-term growth of traditional community solar is increasingly dependent on the establishment of new state markets. Developers have already established strong pre-development pipelines for proposed programs in states including Ohio, Iowa, Pennsylvania, and Michigan.

"So far in 2026, there are signs that the value proposition of community solar is gaining new traction across several states,” said Connelly. “The passage of legislation in these markets could potentially add upwards of 1.5 GWdc through 2030; however, the removal of the ITC in 2030 will complicate new program design and timelines.”

Developers Look to “Community-scale” Solar as a New Avenue for Growth

Beyond traditional, legislation-enabled community solar programs, developers are increasingly broadening their business models to capture the growing opportunity for “community-scale” resources, which the report defines as solar resources up to 20 MWdc in size. Community solar developers are primarily targeting Ohio and Pennsylvania for this type of development, partially driven by the region’s need for new generation to meet rapidly growing demand.

"Utilities are beginning to prioritize “community-scale” resources, which typically encompasses smaller utility-scale projects connected directly to the distribution grid, in their long-term planning,” said Connelly. "These resources have the ability to be deployed more quickly than larger utility-scale projects and, particularly when paired with storage, can improve grid flexibility and reliability.”

"Surpassing 10 gigawatts is a landmark moment for community solar and a testament to the resilience of this industry. We've delivered bill savings to hundreds of thousands of households and businesses even as federal policy headwinds have created real uncertainty," said Jeff Cramer, President & CEO of CCSA. "But reaching this milestone is just the beginning. The expansion of mid-scale, front-of-the-meter solar and storage into new markets signals that our industry is diversifying and adapting in ways that will serve customers and the grid for decades to come. The pipeline is strong and the states stepping up to create new programs are proving that community and distributed clean energy remains one of the most compelling tools we have for putting affordable, accessible power within reach of everyone."

Average Subscriber Acquisition Costs Continue to Decline Gradually

Subscriber acquisition costs contracted 12% from 2024 on average across all customer segments. Lowering subscriber acquisition costs has become a focus for developers looking to optimize project revenue post-ITC removal. Despite state-specific market challenges, Wood Mackenzie expects average costs will continue to decline gradually through 2030 due to the wider adoption of consolidated billing and digital marketing tools. LMI subscribers remain the most expensive to acquire at $100/kW.

The subscription management landscape is also seeing rapid consolidation. In February 2026, Perch Energy acquired the platform Solstice, following Perch’s previous merger with Arcadia. As of the end of 2025, four major subscription management platforms and vertically integrated developers manage 55% of total operational community solar capacity.

Market Outlook and Scenarios

As of the end of 2025, cumulative community solar installations total 10.1 GWdc. Wood Mackenzie has developed high-case and low-case scenarios to capture market uncertainties:

High case: A 16% uplift to the base case five-year outlook through favorable state policy changes and efficient interconnection reform, adding around 1.2 GWdc

Low case: A 14% contraction due to complex tax credit qualification guidelines and limited state intervention, reducing outlook by around 1 GWdc

Notes:

Community solar refers to local solar facilities shared by multiple community subscribers that receive credits on their electricity bills for their share of the energy produced. In most cases, customers subscribe to community solar projects and receive a bill credit from the utility. The size of the bill credit is determined by the program. Programs can provide a full retail-rate bill credit or some alternative rate.

Community solar has a diverse customer base. Homeowners, renters, and apartment tenants unable to install rooftop solar are typical subscribers to community solar systems. Additionally, non-residential entities like commercial and industrial companies, non-profits, or municipal and government entities often serve as “anchor tenants.” An anchor tenant signs a longer-term contract for offtake from the project and tends to use a significant amount of the electricity supplied by the project.