Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

US wind installations to nearly double by 2026 as market builds towards 48 GW through 2030

Robust 15.4 GW near-term pipeline that has cleared commercial hurdles underpins strong 2026-2028 outlook despite cost pressures

1 minute read

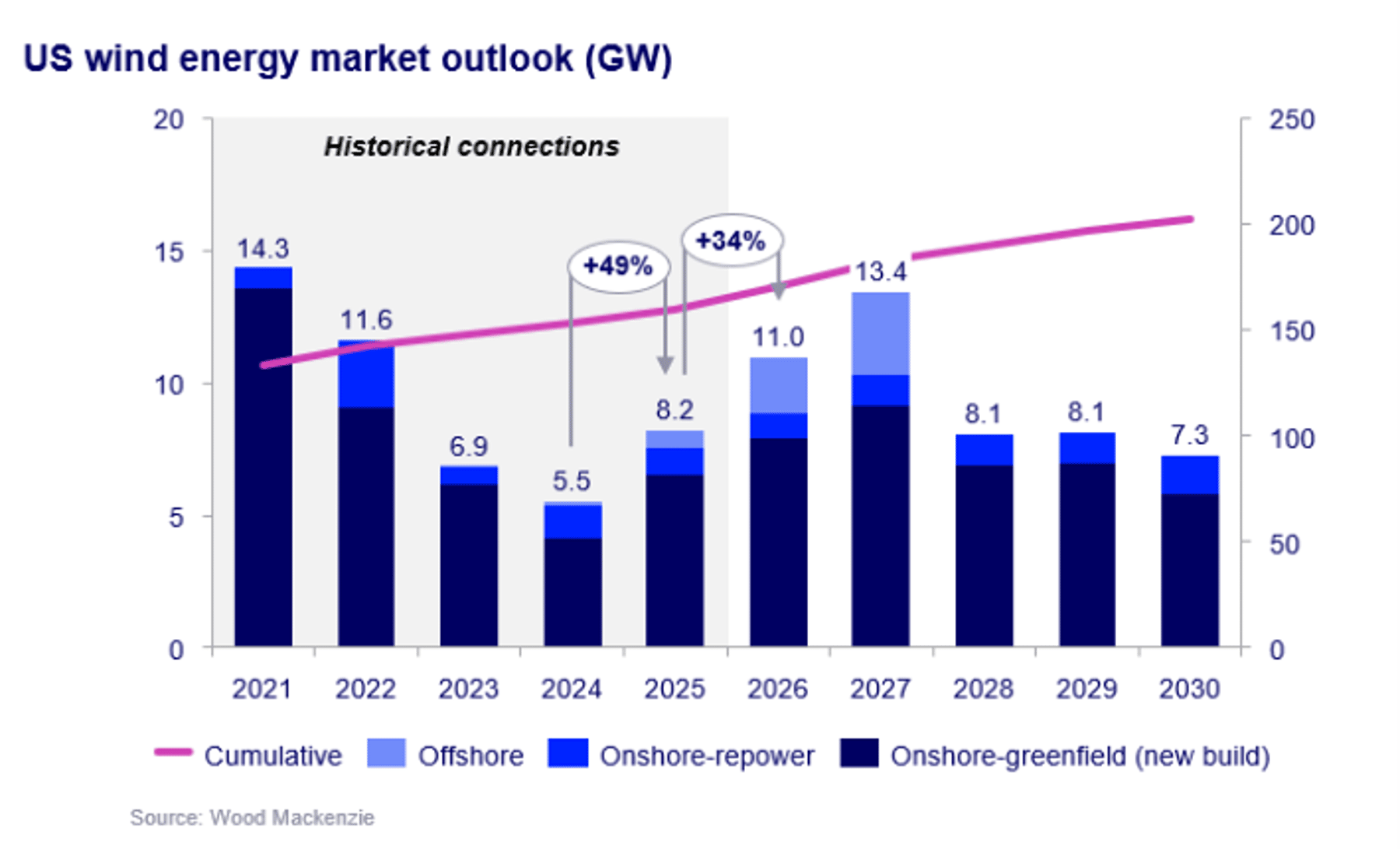

The US wind sector rebounded sharply in 2025 with 8.2 GW of installations—a 49% year-on-year increase— and is forecast to reach around 11 GW in 2026, according to the US Wind Energy Monitor report released today by Wood Mackenzie.

{kind=link}

The report forecasts 48 GW of new wind capacity through 2030, with 2026 set to deliver the strongest installation year in five years. A robust 15.4 GW pipeline of projects that have already cleared challenging commercial hurdles provides visibility into near-term growth, even as federal policy volatility, rising costs and permitting bottlenecks create headwinds for the sector.

"The US wind market has proven remarkably resilient through 2025 despite significant policy uncertainty," said Diego Espinosa, senior research analyst at Wood Mackenzie. "The strong rebound in installations, combined with a well-contracted pipeline through 2028, demonstrates that developers continue to prioritize projects that can secure tax credits under the OBBBA framework."

Land-based wind drives near-term growth

Land-based wind accounts for the majority of near-term activity, with 24 GW expected between 2026 and 2028. About 64% of this pipeline is already in advanced stages, including projects under construction, providing greater certainty on volumes. The regional mix is shifting, with growth becoming more distributed rather than concentrated in traditional wind-rich areas.

The West will dominate 2026 connections at 64% of total capacity, driven largely by Pattern Energy's 3.5 GW SunZia project in New Mexico. The Midwest will peak in 2027 with more than 40% of connections, led by projects in Illinois, Minnesota and Iowa. Texas returns as the leading market in 2028 with around 2.5 GW of connections.

Offshore wind accelerates execution

Offshore wind is delivering faster project execution than previously forecast, with 6 GW expected online by 2027. In 2025, Avangrid’s Vineyard offshore wind farm installed 624 MW, driving a 261% increase in US offshore wind capacity, and subsequently achieved mechanical completion in Q1 2026.

Revolution Wind and Coastal Virginia Offshore Wind (CVOW) have both achieved first-power milestones and are progressing through construction. Ørsted's North America construction program is delivering results, with Revolution Wind on track for H2 2026 commissioning and Sunrise accelerated to H2 2027 from H1 2028.

Policy uncertainty and permitting challenges persist

Federal policy volatility under the current administration continues to weigh on investment confidence, particularly for offshore wind. The Federal Aviation Administration (FAA) and Department of Defense (DoD) permitting processes have become binding constraints for land-based projects, creating downside risk to post-2027 installations if backlogs persist.

Wood Mackenzie's analysis shows that approximately 60% of projects filed with the FAA for Determination of No Hazard trigger a DoD review. The backlog of turbines without final determination has increased more than five-fold in 2025 to nearly 5,000 wind turbines. Failure to clear projects currently held by the DoD could reduce installations through the end of the decade by 17%, or roughly 7 GW.

Cost pressures remain elevated

Supply-chain and cost pressures remain elevated, with turbine prices 22% higher than early 2022 levels. US land-based wind capital expenditure is projected to increase by 5% through 2029, driven by tariff exposure on raw material inputs and subcomponents, permitting obstacles and uncertainty over future volumes.

However, clarity on tax credit rules following the passage of OBBBA and subsequent Internal Revenue Service (IRS) guidance has reduced some near-term uncertainty.

Strong demand fundamentals support long-term outlook

Large-load capacity growth is securing demand growth and strengthening the business case for new renewable capacity. A total of 183 GW of large-load capacity with signed construction or long-term supply agreements represents a significant opportunity for wind energy. About 72% of this capacity with committed status resides in wind-rich areas like ERCOT and PJM.

Power demand growth through 2030 is expected to average around 3% compared to just 0.7% over the previous decade, with data centers accounting for a substantial portion of total peak demand growth. This surge in baseload demand positions wind as a natural fit to meet rising power needs.

"Despite current headwinds, the fundamentals supporting US wind growth remain compelling," said Espinosa. "Rising electricity demand, competitive economics and the safe harbor of federal tax credits create a strong foundation for continued deployment through the end of the decade."