Cross currents Charting a sustainable course for offshore wind

August 2023

Authors

Cross currents: charting a sustainable course for offshore wind

The offshore wind sector is navigating uncharted waters as it grapples with a fresh set of challenges in cost escalation and supply chain pressures. Much recent focus has homed in on a number of problematic projects in the US and UK. These projects won competitive tenders that locked in their remuneration schemes, but have recently found themselves facing low projected returns due to unanticipated cost increases. Developers, used to declining costs for offshore wind projects, had assumed that these would continue, or at least not increase. These unwelcome headwinds have even prompted a few of the projects to halt development and pay contract termination fees for early exit.

This has left the offshore wind industry at a critical juncture. Dealing with such challenged projects is a real set-back for the industry and the energy transition. More importantly, however, they contribute to a larger issue lurking just around the corner ‒ ramping up the supply chain to meet developer and government objectives. These supply-chain challenges need to be addressed as a matter of urgency, as lead times on new manufacturing facilities are typically three to five years, with an additional one to two years until fully up and running. This edition of Horizons looks at these supply-chain constraints and the challenges and opportunities they present.

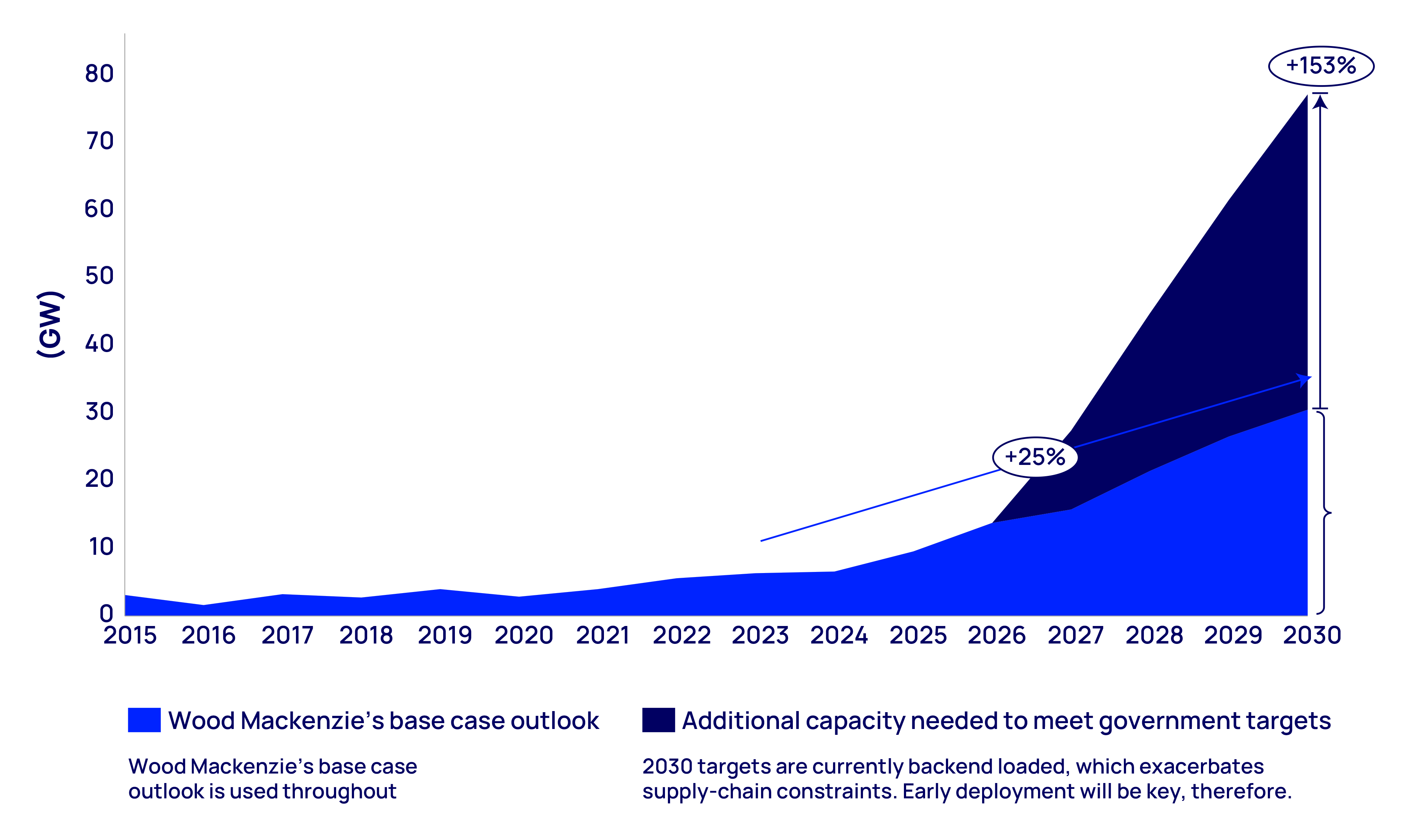

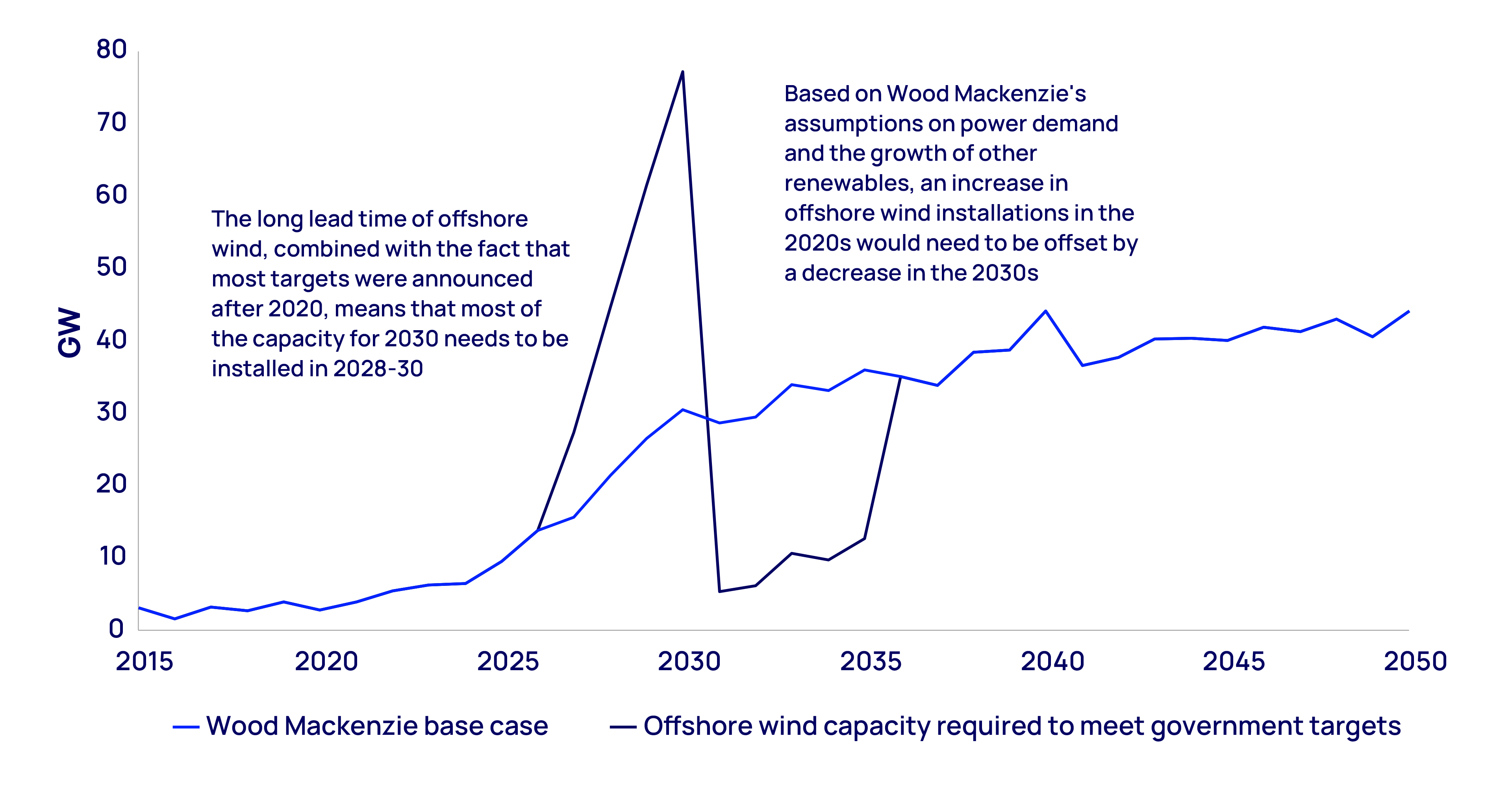

Between 2015 and 2021, annual additions of offshore wind outside China averaged around 3 GW a year. By 2030, we project annual non-Chinese additions to increase tenfold. The technology is proven and cost declines have improved competitiveness. The need for carbon-free generation in land-constrained markets or regions with less attractive irradiance and onshore wind resources has resulted in strong public policy support. Since 2021, governments globally have announced 135 offshore wind targets. If all of these targets for offshore wind were to be achieved, annual additions, excluding China, would need to reach 77 GW by 2030, far exceeding what we expect to be built.

Adding 77 GW of annual installations to meet all government targets is not realistic. Even achieving our forecast of 30 GW will prove unrealistic if more immediate investment in the offshore wind supply chain doesn’t happen soon. Government and developer ambitions got offshore wind off the ground. The early evidence from these initial efforts is that adjustments and new policies will be required to transform the supply chain to deliver offshore wind projects at industrial scale.

Until very recently, China had developed its own supply chain, largely to meet its own demand. For the purpose of this analysis, therefore, we exclude projects and manufacturing facilities in China, unless otherwise specified. We will look at how China could potentially factor into the larger global supply chain in the future, though.

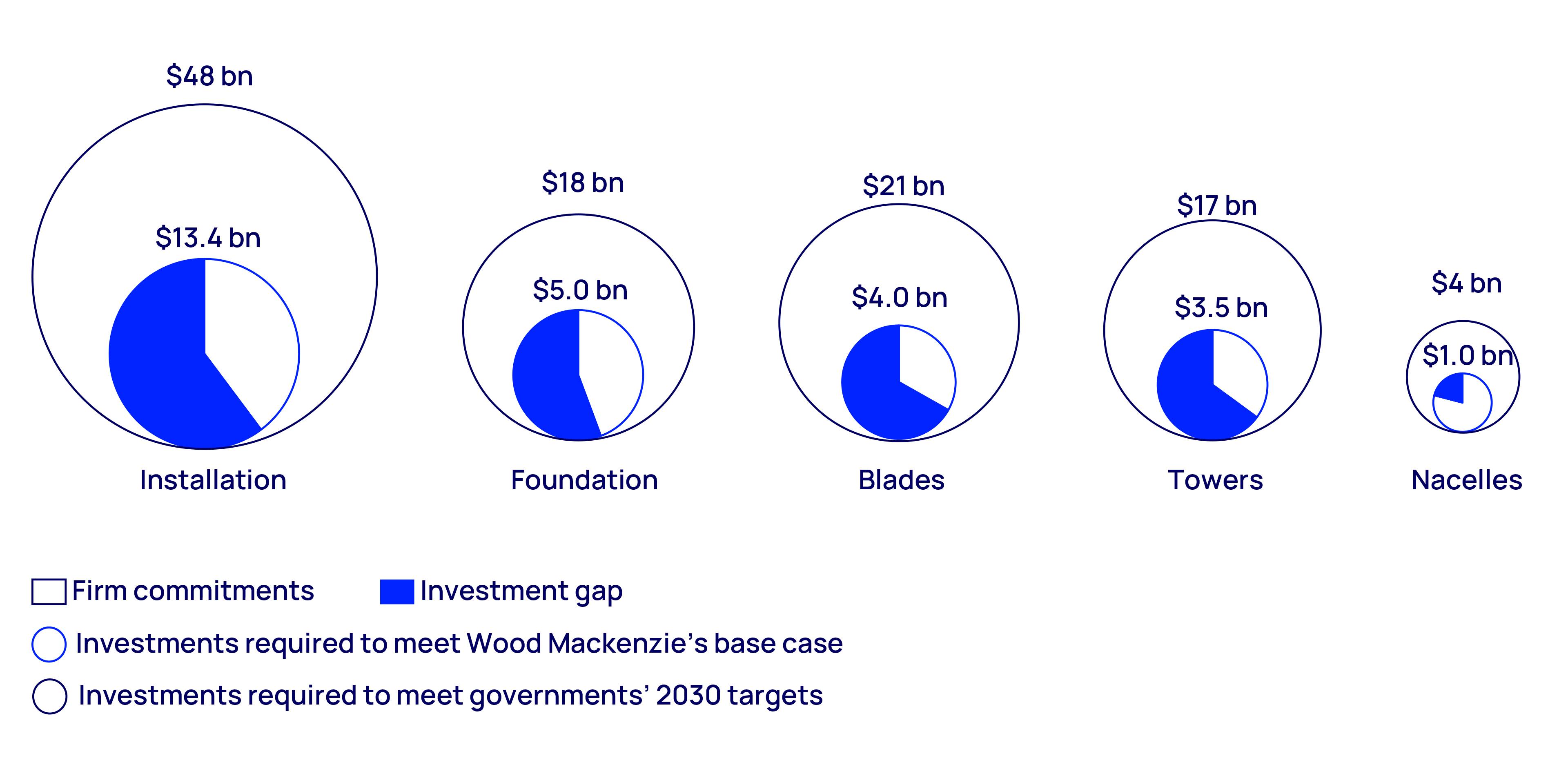

US$27 billion investment needed to build out the offshore wind supply chain

To reach governments’ 2030 targets, more than US$100 billion of investment in new supply-chain capacity would be required. Even to reach our base-case 30 GW of annual installations by 2030, however, will require approximately US$27 billion of investment by 2026, with the bulk of that secured in the next two years to account for facility ramp-up. This US$27 billion does not include full supply-chain buildout; it is what is required for installation, foundations, towers, blades and nacelles. The investment need for each area, along with the gap in investment, is summarised in the figure below.

Each of these components is supplied solely to the offshore wind industry and not the onshore industry due to the unique size of offshore equipment. Other components ‒ of which transmission is the most important ‒ are supplied to other industries in addition to offshore wind.

Installation: the largest investment gap

Installation refers to the installation of turbines and foundations. Here, installation vessels are the critical equipment. Half of the existing fleet is set to be retired from service due to its inability to cope with increasing turbine and foundation weights and dimensions, meaning that more than 20 new installation vessels need to be commissioned. Of the US$13 billion in investment needed overall, installers have committed to slightly less than half.

Foundations: expansion faces numerous challenges

Foundations are the support structures for offshore wind turbines. Monopiles are the primary technology ‒ steel tubes that are driven into the seabed. While established companies have committed to projects that will almost double existing capacity, a similar-sized capacity increase will be required to support 30 GW of annual additions by 2030. Also, scaling the manufacturing capacity of foundations is more challenging than other aspects of the supply chain, because of their large weight and size, complicated logistics and the customisation required for individual sites.

Blades: manufacturers feel the financial strain

Blades interact with the wind to produce an aerodynamic force, which spins the rotor of the turbine. Blade manufacturing typically requires ongoing investment, not just to meet demand growth, but as blade sizes grow, new moulds must be made and the output per mould diminishes. Some facilities have even had to close because they cannot accommodate larger blade sizes. Turbine original equipment manufacturers (OEMs) are suffering low to negative EBITDA margins and have committed to just a third of the US$4 billion investment required in new factories, which is alarming given the three- to five-year lead time for a new facility.

Towers: larger turbine sizes will fuel increases in tower demand

Towers support the mass of the nacelle and blades. Turbine towers are made up of multiple sections, with three-section towers long the mainstay of the industry. But the need to support larger turbine sizes is leading to four- and five-section towers, resulting in a 3.5-fold increase in demand for tower sections by 2029. Increasing section sizes are also making the towers more complex to manufacture and extending the physical dimensions required of factories, sometimes even making existing factories obsolete. While there have been numerous announcements of new potential tower manufacturing capacity, only 35% of the requisite new or expanded facilities have reached final investment decision (FID).

Nacelles: least likely to become a supply-chain bottleneck

The nacelles in a wind turbine house the components that help convert mechanical energy from the blades into electrical energy. Compared with all the other aspects of the offshore wind supply chain, nacelles are least likely to become a supply-chain bottleneck. To meet peak demand this decade, capacity must increase by around 50% from 2023 levels. OEMs have already made FIDs, committing to most of this increase. However, the nacelles are made up of multiple components that are sourced externally. Coordinating the ramp-up of the required sub-suppliers will be challenging.

Why is it so hard to drum up US$27 billion?

Against the backdrop of a multi-trillion-dollar climate crisis, US$27 billion to build out the offshore wind supply chain through 2030 does not seem like a lot of money. So why is it proving so hard to mobilise investment?

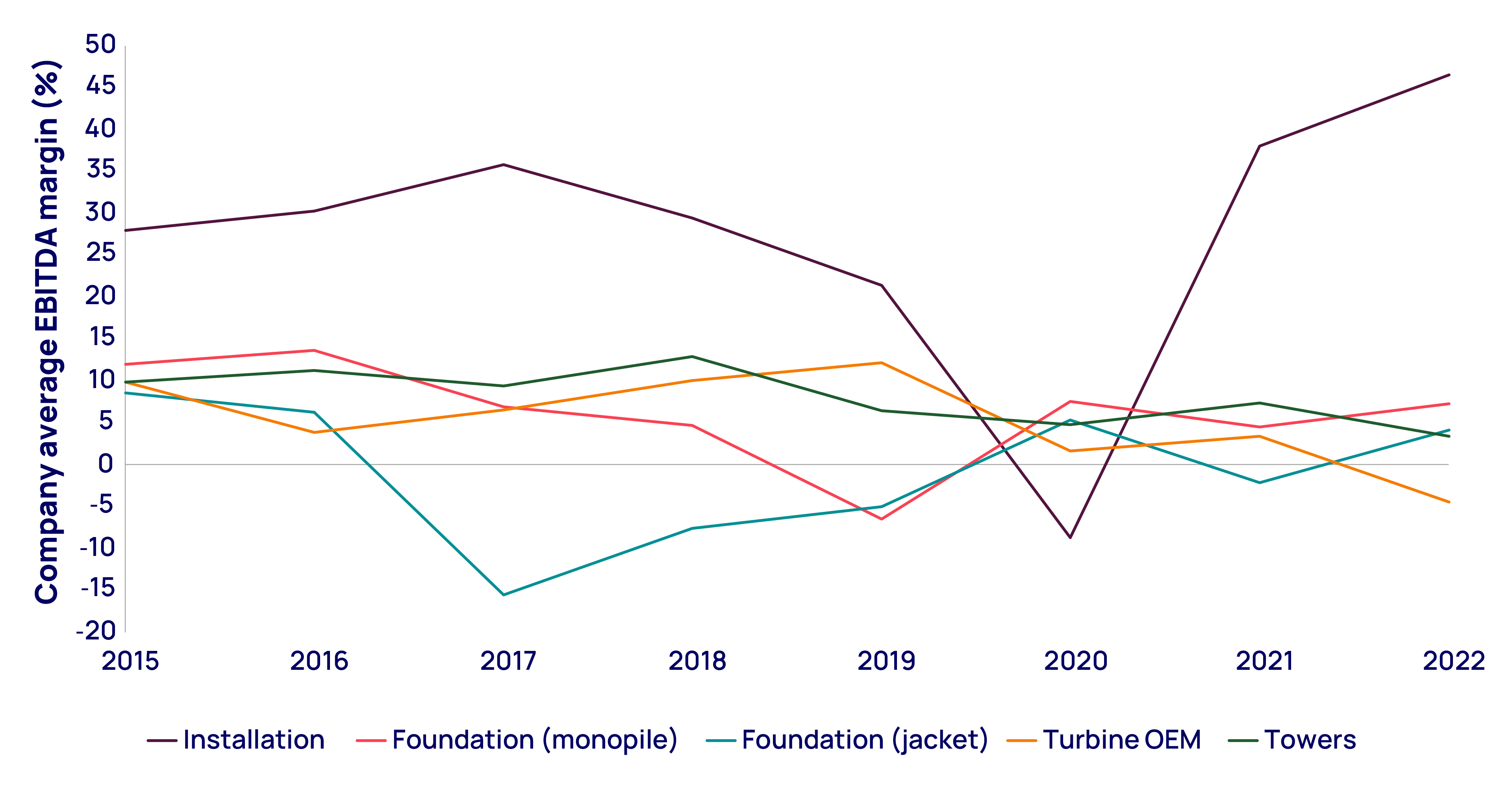

Low offshore margins make the investment case more challenging

Companies in the offshore wind supply chain have seen declining EBITDA margins since 2015, when the industry had built out its capacity to supply around 800 turbines. Since 2015, turbine installations have averaged around 500 a year. Even in 2022, only 678 turbines were installed outside China.

The oversupply that resulted from the 2015 buildout is one of the factors depressing profitability.

The oversupply that resulted from the 2015 buildout is one of the factors depressing profitability. Suppliers are now also having to cope with the inflation of the past two years and higher commodity input costs. An exception to the fall in EBITDA margins lies with the installation companies, which have higher and increasing EBITDA margins. This is misleading, however, as installation is more capital intensive than other sectors and high depreciation has taken a toll on profit.

Burned once, current suppliers are cautious in their investment plans. Moreover, their lack of profitability is hampering their ability to fund manufacturing capacity expansion and has stalled innovation in the sector. What’s more, macroeconomic inflationary pressures are driving up the cost of capex needed for new investments.

Casualties of the turbine-size arms race

The innovation that resulted in increasing turbine size has been key to bringing down the cost of offshore wind. But these larger sizes have also rendered obsolete some elements of the supply chain, such as installation vessels. Elsewhere, costly investments have been required to change manufacturing facilities. Consequently, supply-chain investments and spending on research and development have to be recovered over shorter timeframes, and those investing are unsure what turbine sizes to plan for. Larger-size components have also increased the cost of repairing mistakes when something goes wrong in the manufacturing process. Lastly, increasing turbine sizes have made developers reluctant to sign equipment orders until the last possible moment, hoping costs will continue to fall for their projects with larger turbines. This is probably one of the factors making some projects unprofitable.

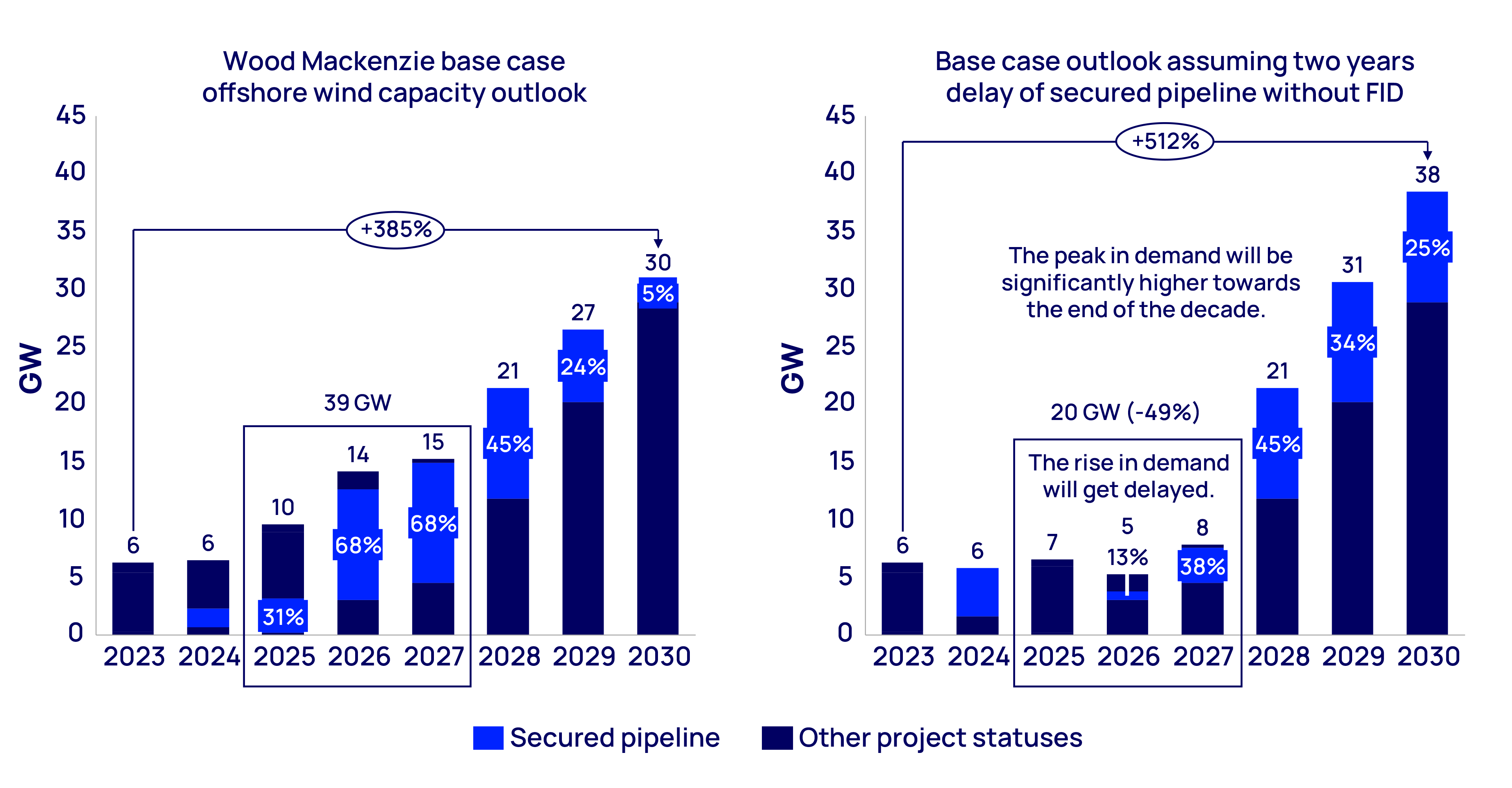

Uncertainty of project timing could result in very different supply-chain needs

Some 24 GW of projects scheduled to come online between 2025 and 2027 have secured a route to market ‒ either some form of subsidy or power purchase agreement (PPA) ‒ but not yet made an FID. Some of these projects signed their PPAs or subsidy agreements before costs started to rise and are now faced with potentially uneconomic projects that they want to renegotiate or exit and bid at a later date.

The following charts show our buildout projections based on current schedules compared with a delay of two years in all projects that have not reached an FID. While it is unlikely all of the projects would be delayed, it would shift expected equipment demand from 2025-27 to 2028-30. The result would be less need for manufacturing expansion in the shorter term, but an even greater need for expansion to meet 2028-30 demand. In reality, if this occurs, certain projects might not get built at all in 2028-30, meaning governments will fall even further behind their targets. The uncertainty surrounding project timing is one reason supply-chain participants hesitate to expand further.

The uncertainty surrounding project timing is one reason supply-chain participants hesitate to expand further.

Figure 4: Wood Mackenzie base-case annual additions outlook vs. outlook assuming a two-year delay to the secured pipeline without an FID

The focus of many governments around the globe has been to set an offshore wind target for 2030, resulting in a projection of 77 GW of installations in 2030 compared with 6 GW in 2023. Many investors are concerned that if the supply chain were built out to satisfy peak installation demand in 2030, somewhere close to government targets, there would be insufficient demand for equipment to support it after 2030. To the industry, this seems eerily similar to the post-2015 collapse in margin. This is an important consideration for suppliers, in particular, as they need 10-plus years to earn a return on their investment.

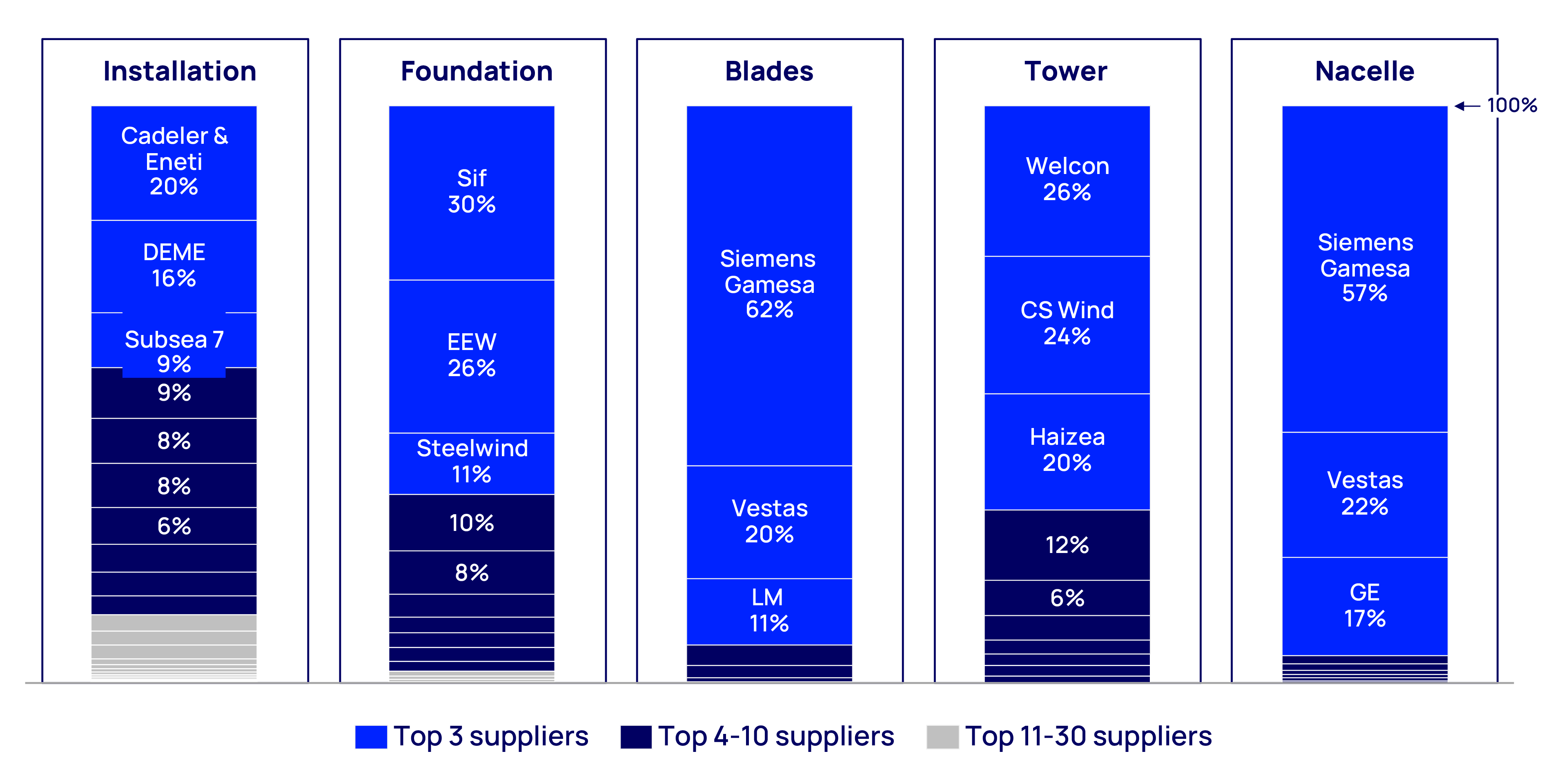

The offshore wind supply chain has become increasingly consolidated

The offshore wind supply chain has become highly concentrated over the past decade. The top three producers of blades, nacelles and foundations account for 93%, 96% and 67% of their respective markets. Not securing capacity with one of the dominant companies could mean having to deal with a considerably less experienced player. Given the weak financial condition of many supply-chain companies now, an exit by any of the companies could have a detrimental impact on the industry’s ability to meet expected demand.

In addition to the consolidation, an increasingly tight market for supply-chain components also means that, unlike the past decade, equipment sellers should, in theory, have more pricing power and an ability to influence project timelines ‒ something developers seeking the lowest cost will have to navigate.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

How to scale up the offshore wind supply chain

Government policy plays an outsized role in offshore wind. The opportunity to invest is often driven by government offtake remuneration schemes, legislation enabling utilities to recover their purchase power costs, the sale of leasing rights and plans to build out the transmission system. Governments also have a direct impact on the supply chain through local content policies dictating that some portion of a project’s equipment be manufactured locally. How government policy is structured and enacted will play a critical role in shaping the growth of the supply chain.

Against this backdrop, important considerations for market participants and policymakers in helping to build out an industry that can meet policy goals include:

- Targets for the post-2030 period. Target setting and plans for power-market infrastructure to support offshore wind integration need to extend beyond 2030 in places where they do not already do so. Ideally, targets could be established for 2035, 2040 and beyond. It is also important to recognise that a 2030 target can be too high, as it cannibalises demand in the coming decades. Lastly, targets need to be accompanied by a clear roadmap for leasing opportunities, transmission buildout and a route to market.

- Competition for equipment. Policymakers should bear in mind that there will be a fight for scarce manufacturing capacity at the end of the decade. The earlier tenders can be held for the 2028‒30 timeframe, and the more robust the tendering framework, the more countries are likely to achieve their targets. We expect these dynamics to be particularly detrimental to the buildout in markets new to offshore wind.

- Confidence in the growth drivers. The sector needs to restore supply-chain companies’ confidence in the certainty that awarded projects will materialise. Almost half of our forecast 2023-30 capacity outside China has already secured an offtake agreement. This level of project visibility is unprecedented. Still, the industry is uncertain as to when and whether projects will reach FID and translate into firm orders. The best way of doing that is to shorten the time between awarding the bid and the project reaching FID, and to enforce strong bid requirements on project deliverability.

- The impact of supply-chain considerations in deciding whether or not to renegotiate at-risk contracts. Countries being asked to renegotiate the terms of previously awarded tenders should consider the supply-chain implications of not doing so: it would likely imperil their ability, and that of other governments, to make 2030 targets. Risk can best be mitigated throughout the supply chain if future contracts include some form of commodity price-risk indexation between contract award and the end of construction.

- Local content requirements. The jobs and economic benefits of local content requirement mandates need to be carefully considered against the goals of developing an efficient and scaled-up supply chain. It will be challenging enough to scale the supply chain without having to ensure that some components are sourced locally. The more local and profuse the requirements become, the more challenging it will be to scale efficiently and the greater the impact on costs.

- Pausing the turbine arms race with a size cap. Turbine OEMs are already developing next-generation turbine models, while some new vessels and facilities being built are capable of accommodating 25 MW turbines ‒ double the size of current installations outside China. The Dutch government recently proposed a cap on turbine tip heights, which would effectively cap turbine size at 25 MW. Ultimately, the most important factor is not the size of the cap, but that a cap is imposed. Getting all nations on board would be challenging. However, if the core markets – Europe and the US – enforced the cap, suppliers would be less likely to introduce technologies that exceeded it, even if it were possible. As increasing turbine size is key to bringing down costs, the cap should be temporary, but at least 10 years in duration, as this would give suppliers and investors confidence in their new investment.

- The China wildcard. With competitive costs, improved quality, healthier financials and an imperative to diversify their portfolios due to fluctuating domestic demand, Chinese companies stand poised to capture market share outside China. Governments, developers and even suppliers now need to make strategic decisions on what role they want Chinese suppliers to play in the global offshore wind supply chain. These decisions will influence jobs, capacity buildout, margins and emissions. Amid western governments’ push for local content and efforts to reduce dependence on China in the solar and storage industry, developers will need to carefully consider whether to develop deep relationships with Chinese companies to plug some of the gaps left unfilled by non-Chinese firms or to rely instead on Chinese suppliers to deal with any contingencies as a backup plan.

- Innovation in partnerships between developers and suppliers. Developers need to consider innovative partnerships with suppliers to provide the demand stability that suppliers need to increase capacity. For instance, in the solar industry, Invenergy recently formed a joint venture with LONGi, one of the world’s largest solar module producers, to build a new manufacturing facility in the US. Invenergy provided a US$600 million investment in the facility and will serve as the anchor customer. In another example, Iberdrola signed a framework agreement with a monopile manufacturer, providing the latter with future sales certainty while Iberdrola receives preferential access to meet its future monopile needs. Other examples include upfront payments and slot agreements by developers to help fund investment in new manufacturing capacity. Developers could also look to invest resources to help scale some of the smaller companies in the concentrated part of the supply chain. These initiatives are needed now to fund new supply-chain investments, but they also create new risk for developers – mainly that they may find themselves committed to equipment orders but not have a project to use that order. We expect tenders to remain competitive, meaning that future ownership for 2028-30 projects remains uncertain. Consequently, innovative types of risk sharing, such as a shared buyback or a secondary market for unused capacity, could prove valuable.

Loading...

Sign up now to get insights like this in your inbox weekly.

Our unique point of view on the latest news, tailored to your industry and interests.