Fuelling change:

How oil and mining companies can finance the energy transition

April 2023

Authors

How oil and mining companies can finance the energy transition

The corporate energy transition is experiencing an identity crisis. Shareholders are constraining companies by focusing on capital discipline. Environmental, social and governance (ESG) issues are on the back foot and investors are favouring value and cash flow over carbon commitments. Renewables are struggling to compete with resurgent fossil fuels as far as returns are concerned and there are worries that the mining sector won’t deliver the necessary metals and minerals.

With energy security trumping sustainability, some elements driving the decarbonisation agenda have certainly gone backwards. The heavyweight Glasgow Financial Alliance for Net Zero (GFANZ) has lost momentum and been forced by its members to adapt. Coal is resurgent in the electricity mix to help keep the lights on. High-profile course corrections on portfolio greening have contributed to a perception that companies are not rising to the challenge, exacerbated by a vocal, anti-ESG backlash.

But the reality is more nuanced than it was in the aftermath of the COP26 climate conference – arguably, peak-ESG – in 2021.

We have identified three ways for companies to manage this complex dynamic. First, shift to a transition growth mindset while nurturing legacy cash cows.

Companies are still responding to the challenges and opportunities of the transition but tending to their legacy cash cows for a bit longer. Financial institutions still think of climate risk as a material investment risk – and an opportunity. Crucially, governments have increased incentives and regulation to drive investment in the transition.

Stakeholders need to build on this progress to drive low-carbon technologies and new transition material supply through the investment inflection point to enable rapid scale-up. It’s a delicate balancing act. On the one hand, the transition leaders have moderated their pace, moving closer to the herd. On the other, transition laggards face rising costs of capital and will have to either improve or accept a narrowing opportunity set.

We have identified three ways for companies to manage this complex dynamic. First, shift to a transition growth mindset while nurturing legacy cash cows. Second, incorporate transition risks and rewards into differentiated investment hurdles rates. And third, use new business models to enable growth and close valuation discounts.

Oil and mining companies have the balance sheets and cash flows to finance ‘their bit’ of the energy transition. However, this is predicated on robust commodity prices to finance investment and shareholder distributions, as well as orderly capital markets and the absence of turmoil. The transition would be harder to finance in a prolonged risk-off market.

Decarbonisation progress card: warnings abound

The energy transition means different things to different companies: an opportunity for multi-decadal growth for power and renewables players, select growth for mining and metals producers, and a potential existential threat to oil and gas companies’ legacy businesses.

Decarbonisation is at the heart of the transition. More energy and natural resource companies have set net-zero operational targets.

Decarbonisation is at the heart of the transition. More energy and natural resource companies have set net-zero operational targets (scope 1 and 2 emissions). This trend will continue and become an acknowledged corporate obligation.

Reducing absolute (or scope 3) emissions from products sold is much more complex. Cutting the carbon intensity of products sold is an obvious risk management necessity – and a potential growth opportunity for many. The responsibility for reducing consumption emissions across the economy does not sit solely with companies, however; it is a societal challenge.

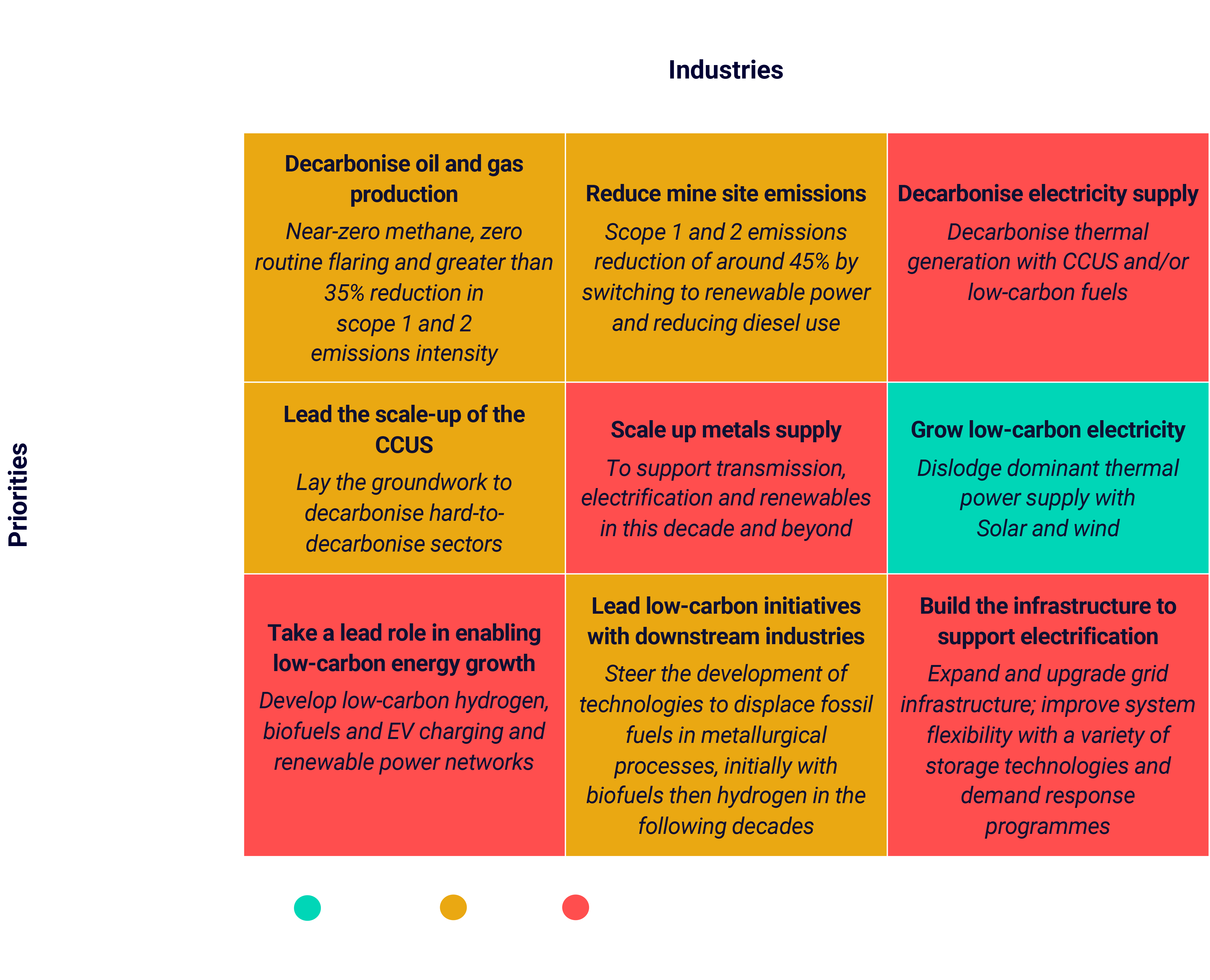

Energy and natural resource companies share similar investment priorities for the energy transition:

- decarbonising operations

- delivering competitive, low-carbon supply growth through, for example, renewables, energy transition metals and biofuels

- enabling infrastructure and supply chains, such as carbon capture, use and storage (CCUS), hydrogen, transmission, renewable equipment manufacturing and electric vehicle charging.

An improving risk-reward balance is already boosting capital allocation. Decarbonisation and low-carbon investment are taking off among the pacesetters in the oil and gas sector. Mining companies are also cautiously increasing the capital allocated to growth in transition-enabling metals.

But the investment response is still way off what is needed. Our 2030 progress card shows that both the development of enabling infrastructure for low-carbon supply growth and downstream decarbonisation are blocking progress.

In the power and renewables sector, the blocks to scaling are grid access, planning and permitting issues, supply-chain bottlenecks and other regulatory issues – not capital availability. For oil and gas companies and miners, capital allocation into the transition is most definitely a constraint. What is holding it back?

Catalysts that shift the risk-reward balance

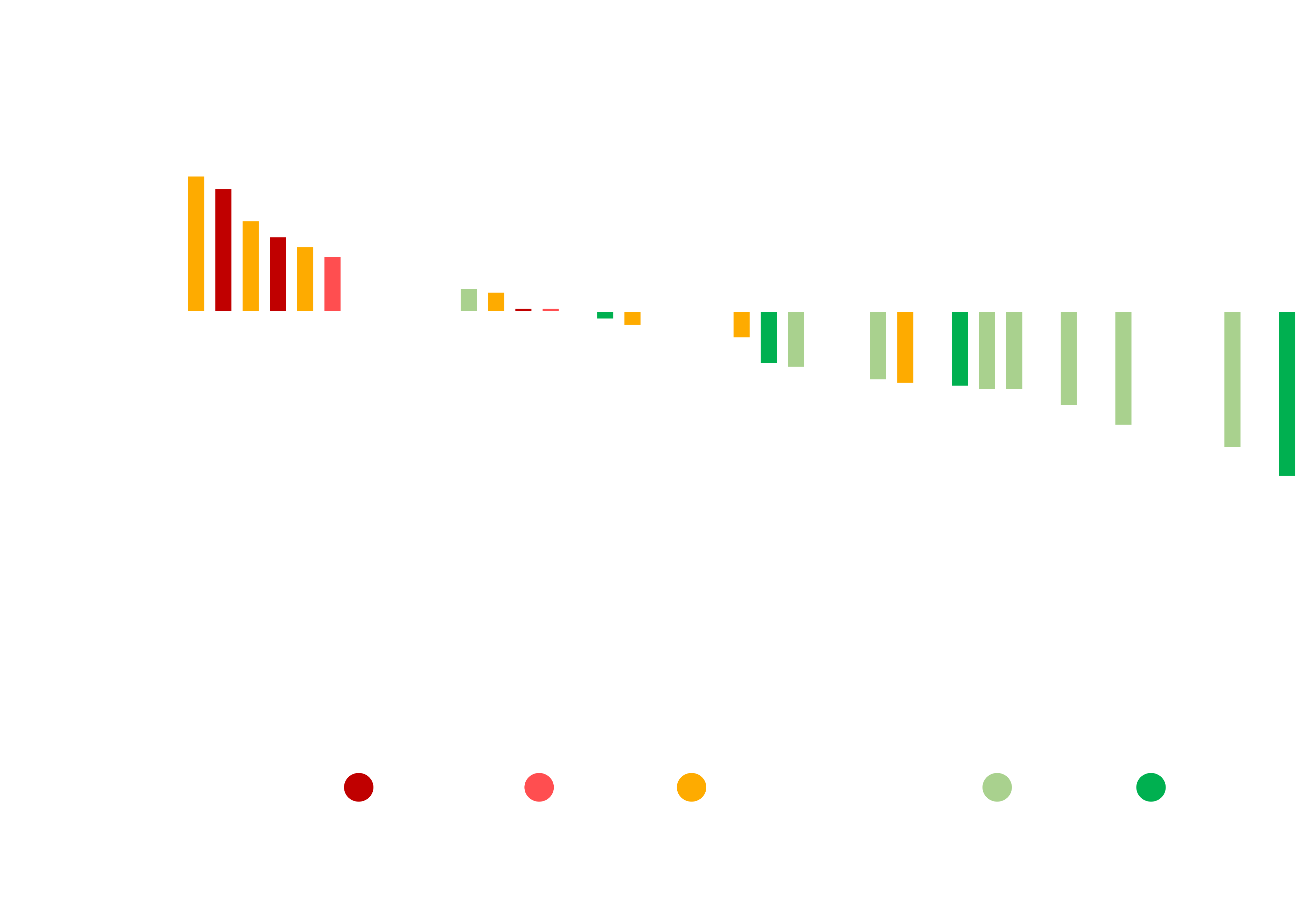

Capital discipline is partly to blame. Expected reinvestment rates (investment as a percentage of operating cash flow) in oil and gas companies and miners of between 40% and 50% trail the investment rates of utilities chasing growth. Reinvestment rates in both sectors have been trending down since the middle of the last decade.

But capital restraint, rising dividends and massive buybacks are working for companies and investors. The oil and gas and metals and mining sectors have outperformed the broader market by 44% and 16%, respectively, since the end of 2021.

Realistically, the only way to change investor sentiment is to bring about further shifts in the risk-reward equation.

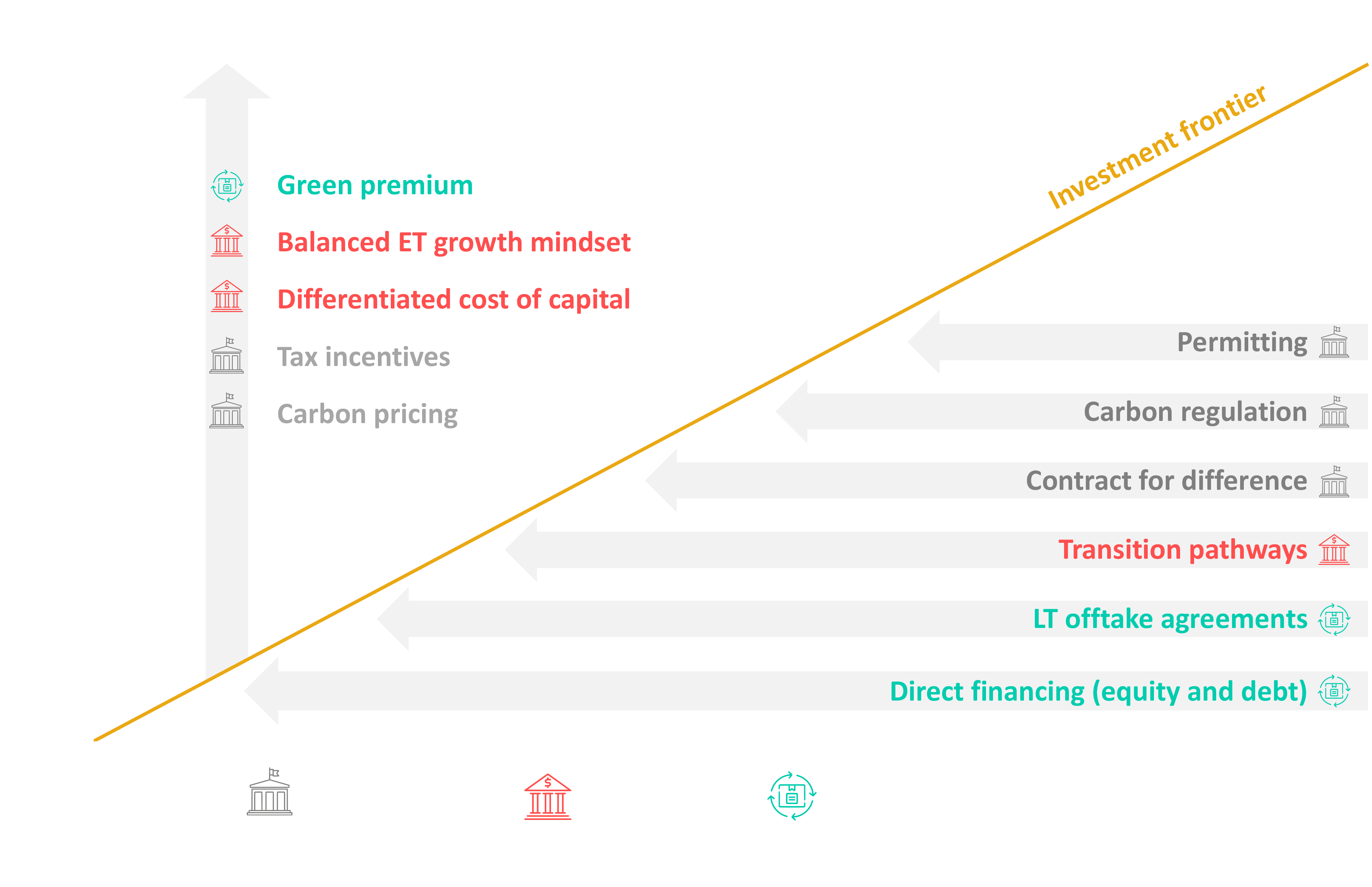

Shifting the risk-reward balance

Capital allocation dynamics can shift rapidly with the right support. We’ve identified several catalysts that could substantially improve the risk/reward balance and incentivise companies to increase investment in the energy transition.

- Government support schemes: The US Inflation Reduction Act (US IRA) and the REPowerEU plan, along with the race-to-the-top policy responses from other regions, are huge, imminent and potentially transformational in terms of changing capex allocation. Unblocking commercialisation pathways by way of permitting and grid support will also boost investment. And other government objectives, such as employment and security of supply for raw materials, are spurring policy to boost investment. Expect more to follow.

- Customers step in to support market creation: Corporate power purchase agreements, long-term offtake agreements and investment in enabling low-carbon infrastructure are all means of de-risking investment. End[1]user willingness to pay a premium for low-carbon products that reduce their supply-chain emissions would send positive pricing signals. Offtake contracts are prerequisites to project finance, particularly important for greenfield mining projects, but also hydrogen and bioenergy.

Those are some of the carrots. Governments and financial institutions hold the two main sticks.

- Government regulation: The European Carbon Border Adjustment Mechanism could have as much of a ground-shifting impact as the US IRA. Tighter regulation, disclosure, country decarbonisation targets, carbon pricing and emissions trading schemes will also support investment in emissions mitigation and CCUS.

- Financial institutions: Leading investors have made it clear that climate risk is investment risk, and companies must actively engage in emission reductions to remain investible. Institutions now include decarbonisation pathways in their core lending and investment criteria, and already impose a higher cost of capital on laggards. Increasingly stringent reporting rules and climate disclosure will boost investors’ ability to evaluate and penalise companies with higher climate risks.

Managing investment inflection points

It is clear to us that it will take this shift in the risk/reward inflection point to convince corporate boardrooms to spend more on decarbonisation. This is when companies start to put meaningful capital to work in an emerging low-carbon technology.

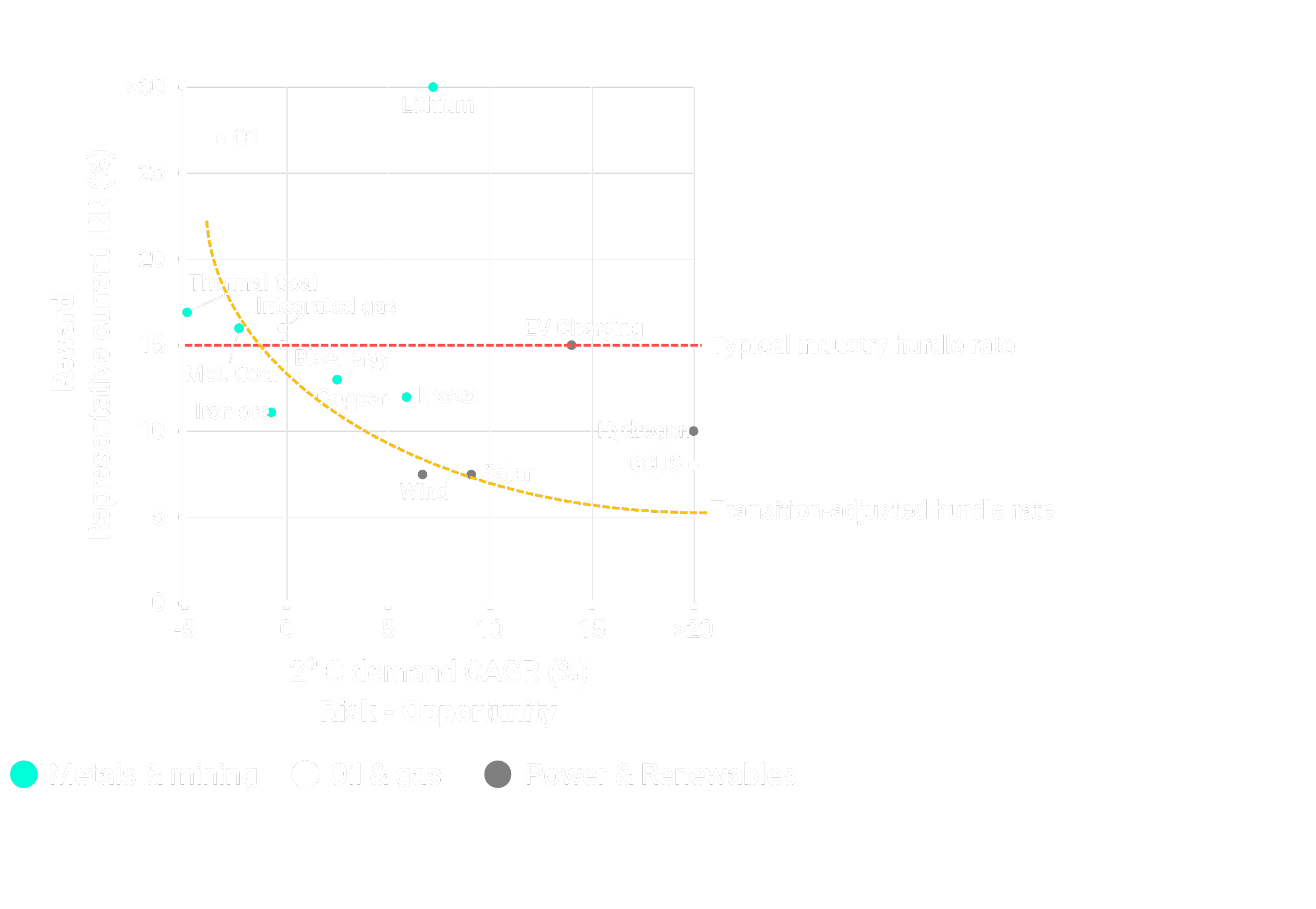

Wind and solar are already well through the inflection point. Capital is pouring in and both technologies are scaling up rapidly. Stakeholders need to engineer something similar for the energy transition support system – metals, CCUS, bioenergy, hydrogen and charging infrastructure.

It is starting to happen in CCUS. Meaningful progress on project maturation in 2022 has lowered risk, while fiscal support in various countries has provided clarity on the business model, offering higher reward.

How policy evolution will impact the timing and pace of the scaling up of these technologies is the big unknown. Oil companies may still face the capital allocation dilemma of high oil and gas returns versus lower-risk, lower-return renewables for many years yet. The metals most exposed to the transition, such as lithium and rare earth elements, have garnered broader market interest than established commodities such as nickel, copper and aluminium. But it is these base metals that need to mobilise the most growth capital to achieve climate goals.

We see three key routes for corporate boardrooms to navigate this complex dynamic.

- Tend to the legacy cash cows while shifting to a transition growth mindset

The more nuanced debate around ESG gives companies an opportunity to strike a more balanced deal with stakeholders, one that will accelerate the low-carbon pivot while ensuring an affordable supply of energy and materials today. This is likely to be accompanied by robust company valuations.

Industry-specific transition pathway frameworks – which define how different sectors will achieve Paris alignment – will contribute to a more open discussion between investors, companies and other stakeholders. Transition pathways are at the heart of the GFANZ framework adopted by major financial institutions.

Companies can influence this discussion from a position of improved strength. As Larry Fink, Chairman and CEO of BlackRock, the largest asset management company in the world, wrote in his 2023 annual letter to investors, it is “not our place to be telling companies what to do. My letters to CEOs are written with a single goal: to ensure companies are going to generate durable, long-term investment returns.”

Most mining majors exited coal before the energy crisis, missing out on bumper profits. The spin-off companies are using cashflows to expand production – not the intended result. Investors now expect companies to balance the need for returns today by tending to their legacy portfolio with transformation tomorrow. Companies have greater flexibility to harvest legacy hydrocarbon portfolios, ensuring responsible rundown.

And investors are still rewarding those companies that don’t move too far, too fast. Transition laggards in our oil and gas Corporate Resilience and Sustainability Indices (CoRSI) framework are trading at some of the biggest premium ratings in our coverage.

But the market will shift to a transition growth mindset if (when) the risk-reward equation changes, with a corresponding change in relative valuation. Visibility of low-carbon profit centres starting to support – and supplant – the legacy cash cows could be such a revaluation trigger.

Companies can scale back share buybacks to fund the shift. The mining majors and international oil companies allocated US$157 billion, or a whopping 30% of their operating cash flow, to buybacks in 2022. The great post-pandemic phase of deleveraging is largely complete (oil companies’ average gearing fell from 45% in Q2 2020 to 28% at the end of 2022; mining majors had deleveraged prior to 2020). Companies could still grow base dividends and lift reinvestment rates to over 60%, but may be reluctant to increase them beyond this level to previous cyclical highs.

2. Bend hurdle rates to reflect transition risks and rewards

Internal hurdle rates need to follow the divergence in external costs of capital, risk and long-term growth potential. Initiatives suitable for project financing will continue to enjoy lower hurdle rates; for short-cycle projects (rapid payback), the transition risk is lower.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

As the transition unfolds in the longer term, expect hurdle rates to bend with transition risk and opportunity. Part of the low ‘return’ of transitional investment is risk avoidance and optionality. And higher returns could be up for grabs in low-carbon projects with greater commercial risk, such as CCUS developments that include carbon price risk. In times of uncertainty, companies need a bigger portfolio of options to manage risk.

Building a deep and diverse low-carbon, transition-ready pipeline will be critical to remaining responsive in future. And companies will need flexible strategies to respond to an evolving risk-reward balance, monitoring the main catalysts that impact the pace of the transition and adapting capital allocation accordingly.

Already, some of the European majors are adjusting, diverting part of the capital earmarked for renewable power to other low-carbon opportunities, such as bioenergy. And mining majors are concentrating on their core commodities (like copper), opting for low-risk strategies such as brownfield projects and acquiring existing producers. Mining majors will also need to beef up their transition metals opportunity set, perhaps by diversifying into less familiar battery raw materials to capture the high returns in this sector.

Oil and gas companies will also use ever-tougher capital allocation criteria for hydrocarbon investment, even if prices stay high. We are already seeing this play out with emissions intensity, with new projects increasingly only getting the green light if their emissions intensity is lower than the portfolio average. And many companies already use lower hurdle rates for gas than oil.

3. Use M&A and new business models to enable growth and close valuation discounts

Mergers and acquisitions (M&A) are a potential backstop that will enable late movers to catch up. However, that strategic optionality may evaporate if commodity prices and margins tank in an accelerated transition, even for companies with fortress balance sheets. Buying into advantaged low-carbon assets, such as CCUS and hydrogen, could quickly become expensive.

Major oil companies are already using M&A to accelerate expansion into low-carbon businesses, such as biofuels, biogas and renewable power. However, overall capital allocated to low-carbon M&A remains limited. Mining majors also continue to take a low-risk approach to acquisitions of transition-focused commodities.

New or modified business models can help reduce the transition valuation discount and support efficient capital allocation in businesses with very different costs of capital and risk-reward profiles.

Partial spin-off subsidiaries can inject low-cost growth capital and reveal hidden value in the conglomerate structure of larger groups. Companies can tap into lower-cost capital by partly selling down de-risked renewable assets to boost cash flow and returns. New vertical integration can also support expansion in areas such as biofuels and battery-related supply chains.

Innovative approaches to accessing diverse financing partners are a means of boosting equity returns. The majors' expertise in project management makes them ideal custodians of new capital. But they must align project financing with stakeholder appetites. For instance, project finance offtake agreements would suit original equipment manufacturers’ desire for low-risk offtake, while also boosting returns for mining operators.

Loading...