1 minute read

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan is responsible for formulating our research outlook and cross-sector perspectives on the global downstream sector.

Latest articles by Alan

-

Opinion

The Hormuz shock: what the data reveals about global oil markets in 2026

-

The Edge

Has the oil price bubble burst?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

The Edge

Ceasefire in the Middle East

This article was updated on 17 July 2020 with our latest view on the impact of Covid-19 on the refining sector

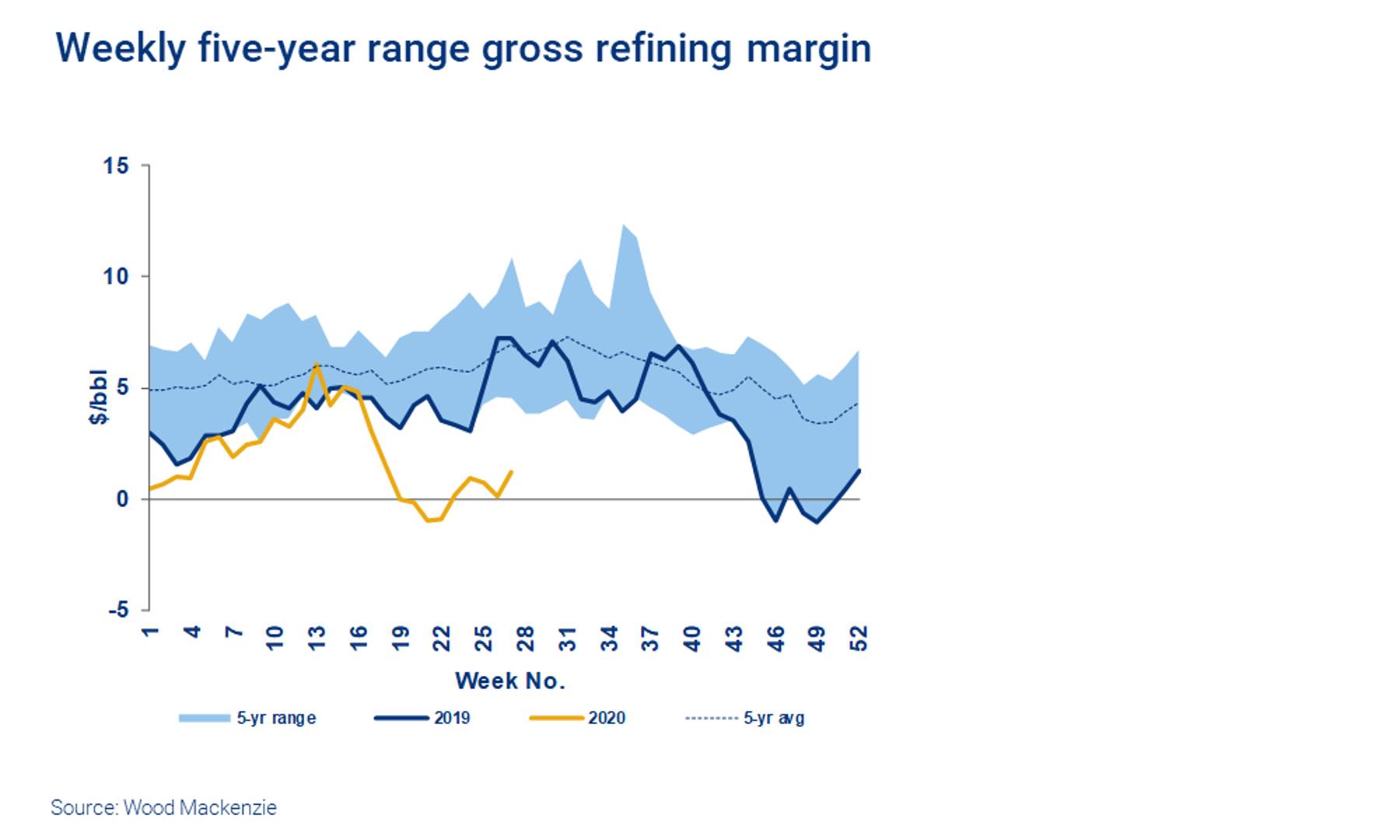

The global coronavirus pandemic has hit the refining sector hard in two ways. Firstly, the collapse in demand for personal mobility (gasoline and jet fuel) has resulted in lower refinery utilisation and, in some cases, key upgrading units being shutdown. Secondly, the OPEC+ group has made major cuts in their supply of crude oil, so medium crude oils are now in tight supply and no longer cheap. The combination of low utilisation and lack of crude price differential delivered catastrophic refinery margins in May and June.

Refining margins are now recovering, as lockdown restrictions are eased. Demand growth has returned and refining runs are increasing, but slowly to draw down high product stocks. Many of the refineries shut during the worst of the pandemic are coming back to operations as their local economies emerge from lockdown.

{kind=link}

The refining system is emerging into a “new normal”, with lower levels of demand. This is a more challenging environment, with the pandemic providing a foretaste of refining in a world of low demand Refiners now have a clear impetus to establish how they can survive and thrive during the energy transition.

Refining has always been a challenging business

Global refining capacity has continued to grow despite periodic bouts of rationalisation in OECD countries. The energy transition introduces the threat of oil demand peaking before 2040, which makes refinery investment decisions even more difficult.

The coronavirus crisis could be a grim foretaste of what the longer-term future looks like for the refining industry when oil demand starts to decline. In this report, we explore how existing refiners can adapt to low demand in a low carbon future, whilst staying true to their roots as a conversion industry.

Get the highlights of the report below; fill in the form to get your copy of the full report.

As demand growth stalls, refineries get ever larger

Since 1980, global refining has increased by 25%, but that growth has varied markedly by region. Investment has flowed where oil demand growth or imports of refined products have been strong; elsewhere, capacity has been either rationalised or closed.

That same story will continue to play out over the next two decades. But sustained investment in additional refining capacity will be required during this period, according to Wood Mackenzie’s energy transition outlook.

More capacity will be needed in the Middle East and Asia to satisfy regional demand growth. The attributes of new refineries to be built in regions of demand growth, such as the Middle East and Asia are well known – large, highly petrochemical integration and strongly competitive. In OECD countries, competitively weak assets will be closing, as local demand falls due to fuel efficiency improvements and electrification of the vehicle fleet.

World-scale refineries are getting bigger while the energy transition is weakening the global growth in oil demand. Within the next five years, the risk of cannibalisation within the sector – when each new refinery project prompts the closure of assets elsewhere – will grow.

Who will thrive and who will merely survive?

We were projecting a significant surplus of refining capacity over the next five years, even before the emergence of the coronavirus and its near-term downward impact on oil demand. Our broad expectation is that demand is not destroyed but delayed.

Any new refineries will need to be large coastal sites that are heavily integrated with petrochemicals to ensure they are highly competitive. OECD refiners need to adapt to declining local demand and a shifting social and political landscape. Business responses must extend beyond the traditional levers of selective investment and cost control to reduce carbon intensity in both operations and their supply of liquid fuels. The core competences of operating integrated refinery petrochemical sites can be leveraged to become a central hub in a “low-emissions energy complex” that brings together carbon capture and storage, chemical recycling, LNG and renewables.

US and European refinery competitiveness profile

The chart shows recent US and European refinery earnings and the future demand for road fuels in those regions for 2025 and two energy transitions scenarios for 2040. By 2040, in either scenario, significant crude oil refining capacity is under threat of rationalisation.

No one-size-fits-all strategy for refiners

In a world aspiring to restrict the global temperature rise to less than 2 degrees Celsius, the disruption to the global refining industry could be even more severe. Wood Mackenzie’s accelerated energy transition would require much greater penetration of battery technology and hydrogen into the vehicle fleet. In such a scenario, localisation is a key theme – refiners working closely with the local community and their government to retain a social licence to adapt their business.

Cost reduction, competitive position improvement and understanding the refinery’s carbon life cycle are obvious “no regret” moves. Beyond that, no one size fits all, so strategic reviews will be essential to establish a road map for the future.

Refining is, after all, a conversion industry – one that must transition away from carbon-intensive feedstocks such as crude oil and into products and services that the consumer still values.