4 threats to the global ethylene boom

Can the global ethylene boom be sustained as risks mount?

1 minute read

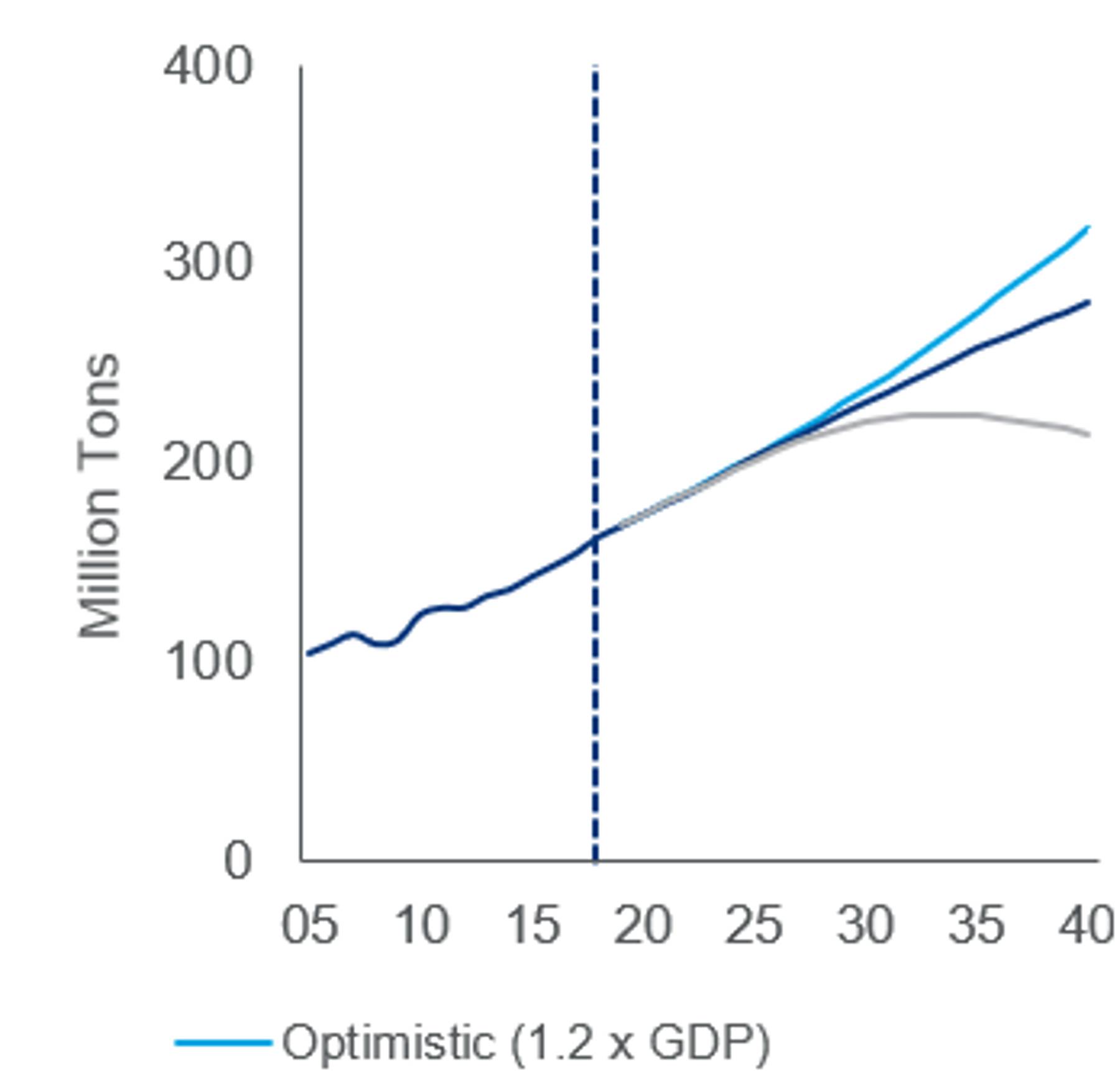

The ethylene market is booming. Driven by consumer demand for everyday products from plastic packaging to clothing, we expect global demand growth of 3.4% annually. How do we see the supply/ demand pattern playing out in key markets globally and who is set to benefit most? More importantly, alongside every boom comes a potential bust.

Boom or bust?

Ten years ago, the picture looked very different. Now, as the largest petrochemical by volume in 2018, ethylene forms the backbone of the petrochemical industry. A heady combination of strong global consumer demand combined with a lower oil price enabling cheaper feedstocks and high operating rates has created boom conditions, leading to a rush of investment from North America to China and even Europe. With mounting risks including a consumer backlash against plastics and the threat of overcapacity following a rush to invest, is the perfect storm on the horizon? We look at four factors that pose a threat to the continuation of the ethylene boom.

1. It’s all happening in North America

North America was the first to benefit from ethylene’s changing fortunes. The competitive advantage delivered by the shale boom, resulting in low natural gas prices relative to crude oil prices, saw the US market build capacity that is now starting to materialise.

While ethylene from shale remains globally competitive, additional investment that willincrease US market capacity by 50% over the next five years from its 2010 level, will not enjoy the high margins we saw initially. The advantages North American producers experienced as a result of being ahead of the investment curve have now shifted elsewhere, with super-cycle margins transferring to Asia and Europe.

2. Routes to market remain a challenge

For US producers, market access is a key limitation, particularly for surplus ethylene monomer for the time being. Construction of ethylene export terminal infrastructure is in progress but until it is ready, producers will need to turn to easier-to-export derivatives, such as polyethylene and MEG. As the demand for ethane feedstocks grows, prices will rise as costs of production and delivery increase, with basins located further away from the US Gulf Coast.

Meanwhile, the tariff war with China has changed the playing field for US producers and is an ongoing risk to the ethylene export industry. The market for surplus exports in China is clear, but protectionism will limit market access.

3. China’s investment explosion

China is on a massive wave of steam cracker investment, driven by the ethylene industry’s healthy margins. The liberalisation of the market has allowed private companies to invest alongside state-owned producers and this changing pattern of ownership has created an investment explosion as producers look to benefit from ethylene’s attractive profitability levels.

The additional capacity will help to improve China’s self-sufficiency but will not eliminate the country’s ethylene deficit. China remains a critical outlet for export surpluses.

4. Plastic is now in the sustainability spotlight

The public, environmentalists, brand owners and governments are responding to the rising tide of negative perception against plastic waste, with ongoing efforts to reduce, reuse, recycle and even ban plastic materials. However, despite the backlash, improving living standards and population growth plus the lack of ready alternatives support the market for plastics for the next 20 years.

{kind=link}

What it all means for the ethylene dream

Mounting risks could create the perfect storm. After years of boom conditions, storm clouds are gathering.

As players across the US and China rush to invest in production, with many ethylene projects planned post-2020, there is a clear downside risk of overcapacity.

Massive investment is partly driven by the oil industry. Faced with the prospect of declining use of oil in transportation as electrification bites, the industry sees petrochemicals as a means to take advantage of the growing demand for plastics. This shift from crude to chemicals poses a risk to chemicals’ long-term margin viability. And if, as expected, the oil price remains high into the 2020s, this could also affect prices of petrochemical products and impact their competitiveness.

Gathering clouds on the horizon could create the perfect storm for the ethylene industry. Our base case is more optimistic – but whichever way the wind blows, the industry should at least prepare to navigate some choppy waters ahead.

Want to know more about our supply/demand forecasts and the risks affecting the ethylene industry? Fill in the form to receive an extract from our presentation Global Ethylene: Living the Dream delivered at the 2018 European Polyester Conference.