5 key takeaways from Wood Mackenzie’s CCUS Conference 2025

Perhaps not full speed ahead, but CCUS continues to grow

1 minute read

Peter Findlay

Director of CCUS Economics

Peter Findlay

Director of CCUS Economics

Peter leads the economics and project valuation function for CCUS projects globally.

Latest articles by Peter

-

Opinion

How gas and power markets are inextricably linked in 2026

-

Opinion

Decarbonising data centres: hyperscalers’ power race will increase emissions but spur more direct decarbonisation

-

Opinion

5 key takeaways from Wood Mackenzie’s CCUS Conference 2025

-

Opinion

Is CCUS viable in power generation?

-

Opinion

5 key ways to decarbonise cement production

-

The Edge

COP29 key takeaways

Tania Alvarez

Research Associate, CCUS

Tania Alvarez

Research Associate, CCUS

Latest articles by Tania

-

Opinion

5 key takeaways from Wood Mackenzie’s CCUS Conference 2025

-

Opinion

Is CCUS viable in power generation?

-

Opinion

5 key ways to decarbonise cement production

John Ferrier

Senior Research Analyst, Carbon Management

John Ferrier

Senior Research Analyst, Carbon Management

John works to provide expert insight and strategic analysis on developments in CCUS across EMEA to support his clients.

Latest articles by John

-

Featured

Carbon mitigation: 2026 half-time report

-

Opinion

5 key takeaways from Wood Mackenzie’s CCUS Conference 2025

-

Opinion

CCU – from decarbonisation to defossilisation

-

Opinion

Defossilizing industry: considerations for scaling-up carbon capture and utilization pathways

-

Opinion

Ready, steady, store: delivering on the EU’s CO₂ storage obligation

-

Opinion

Video | Three FIDs, one day: a turning point for CCUS in the UK and Denmark

Shashank Atreya

Senior Research Analyst, Carbon Markets

Shashank Atreya

Senior Research Analyst, Carbon Markets

Latest articles by Shashank

-

Featured

Carbon mitigation: 2026 half-time report

-

Opinion

4 carbon policy developments that impact E&P decision-making

-

Opinion

5 key takeaways from Wood Mackenzie’s CCUS Conference 2025

-

Opinion

Carbon markets Q2 update: policy shifts and market evolution

-

Opinion

CBAM: break for the border (mechanism)

Wood Mackenzie hosted its third annual CCUS Conference on October 8-9 in Houston. With its global focus on project development, strategy, markets, new technology feasibility and economics, the event convenes some of the world’s most prominent CCUS developers and investors. Preceding the event, Wood Mackenzie hosted its inaugural CCUS Executive Summit that brought together 25 of the world’s leading CCUS and carbon management executives for two days of Chatham House discussions.

Read on for the first takeaway, and complete the form to access the full conference summary. Full CCUS Executive Summit insights will be available in November for Lens Carbon subscribers and Summit attendees only.

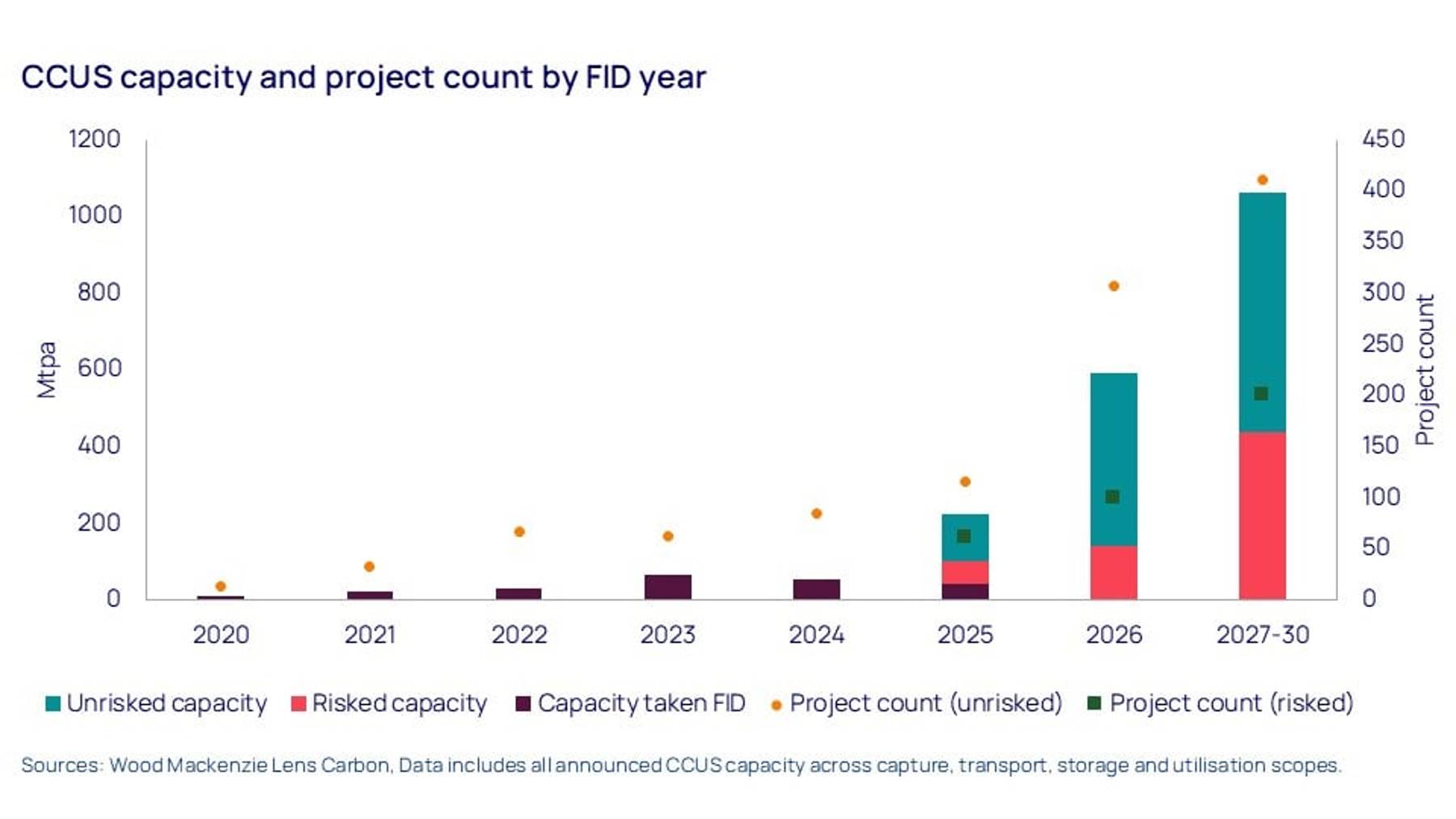

1. Progress continues despite turbulent politics

While decarbonisation efforts across several key sectors may appear to be slowing, global CCUS development continues.

The US still leads capture capacity across North America – despite political uncertainty – with increasing interest in CCUS-integrated power generation to meet surging demands from data centre expansion. However, we expect accelerated project development in Europe, where comprehensive regulatory frameworks and targeted funding mechanisms are creating favourable conditions for CCUS deployment.

Project developers confirm that combining tax credits with capture cost subsidies creates favourable policy environments but still emphasize concerns about incentive stability across changing governments for long-term investments. CCUS leaders also highlight export markets for low-carbon products and high-quality removals as essential revenue diversification beyond government incentives.

Full value chain collaboration remains critical to connect CO2 sources with storage infrastructure. While transport and storage are typically less expensive than capture projects, developers still need to navigate complex cost structures, regulatory hurdles and public opposition.

{kind=link}

Fill in the form above to gain access to all five key takeaways from Wood Mackenzie’s CCUS Conference 2025.