Can CO2 utilisation drive increased carbon capture?

Carbon dioxide utilisation could bolster carbon capture economics, but there are major obstacles

3 minute read

In theory, using captured carbon dioxide (CO2) instead of simply storing it should improve capture project economics, boosting uptake. However, currently less than 5% of carbon capture capacity announced globally involves utilisation. So, what’s stopping this potentially useful resource being reused?

Wood Mackenzie has published an in-depth insight into the potential of CO2 utilisation as an enabler for carbon capture uptake, based on data from Lens Carbon, part of our Lens platform. Fill in the form to download a complimentary extract from the report, or read on for a brief overview of the issue.

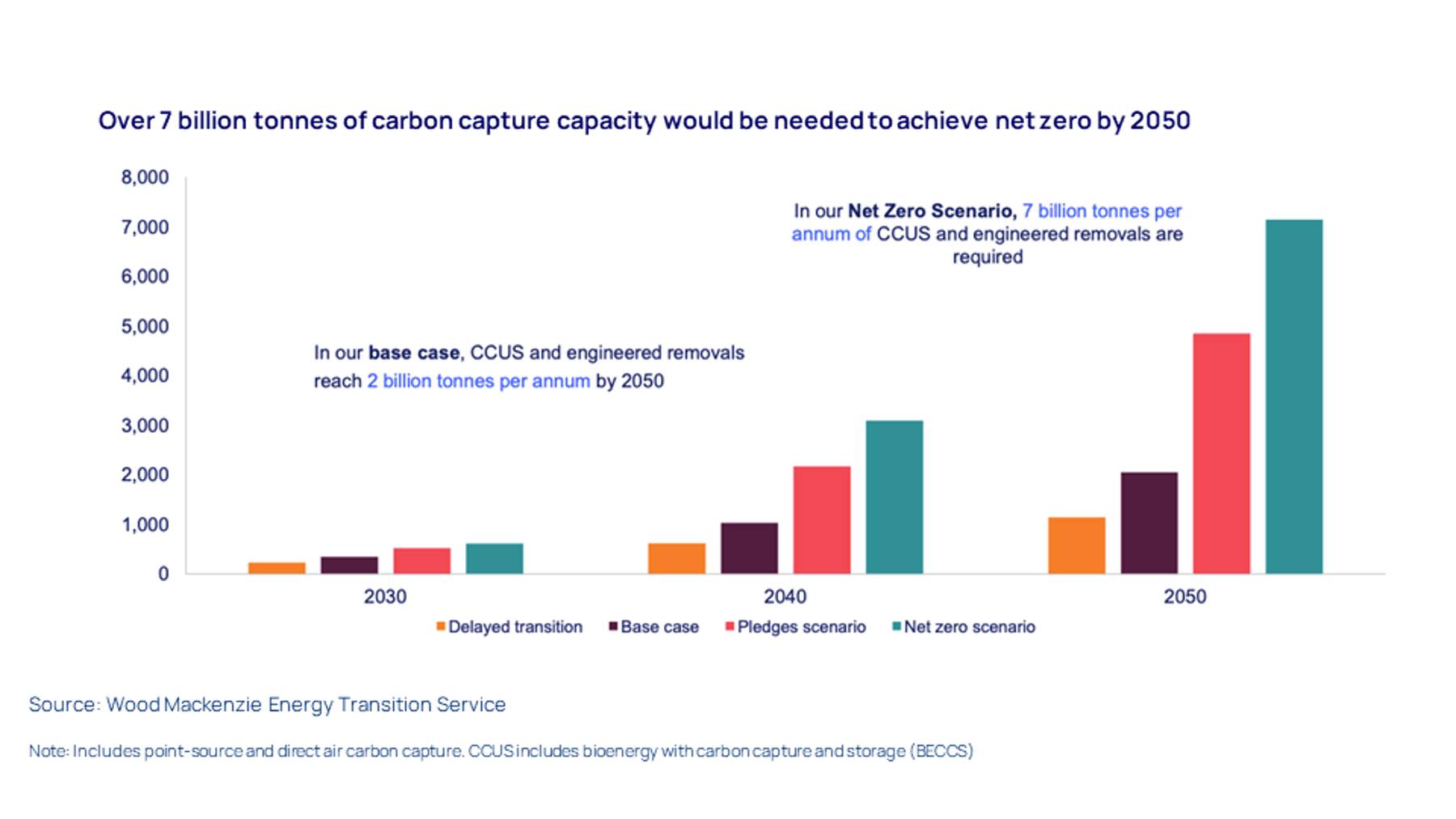

Why carbon capture matters

Strong carbon capture utilisation and storage (CCUS) buildout will be a crucial element of achieving global decarbonisation in a timescale aligned with minimising the impact of climate change. In our base case, which corresponds to a 2.5 ˚C global warming pathway, two billion tonnes per annum of CCUS and engineered CO2 removals will be needed by 2050. Meanwhile, under our net zero 2050 scenario, which assumes global warming is brought back under 1.5˚C by 2100, that figure rises to seven billion tonnes a year (see chart below).

{kind=link}

Why utilisation matters

Unfortunately, current incentives are not enough to encourage the widespread use of carbon capture and storage (CCS) in some sectors. Aside from government support, developers need other ways to boost revenue and bolster project economics.

Potential revenue pathways include credit generation (from selling CO2 removal in voluntary or compliance-based marketplaces) and product premiums. However, proven markets for green premiums and carbon removal don’t yet exist at scale, and in any case will be highly unpredictable.

Another option is to derive revenue from the sale or conversion of CO2, which can be used in a number of ways, such as in the production of e-fuels. If CO2 utilisation pathways can be made competitive, this could provide sustainable, long-term revenues for projects, supporting increased deployment of CCS and carbon dioxide removal (CDR) – i.e., any technology used to produce net removal of CO2 from the atmosphere.

The bull case

In theory, utilisation could enable increased CO2 capture deployment through the creation of a large-scale CO2 commodity market:

- Mineralisation and plant co-feed: Pathways including conversion to high-purity limestone and plant co-feed are already technologically mature and cost competitive with traditional methods

- E-Hydrocarbon production: CO2-to-hydrocarbon pathways could help compensate for limited availability of biofuel feedstocks, providing drop-in fuel replacements for shipping and aviation

- Commodity replacement: Using captured CO2 in low-emission processes could displace commodities produced through high-emission processes, delivering additional emissions reductions

- Co-feed to existing production units: Traditional pathways such as methanol production provide opportunities for co-feed to deliver selective decarbonisation of production with minimal capex

The bear case

While there are a range of potential uses for captured CO2, they may not be competitive with other carbon capture and storage (CCS) revenues and traditional manufacturing:

- Limited potential scale: Global prospective subsurface CO2 storage capacity is nearly 15,000 billion tonnes, dwarfing the potential of utilisation

- Policy disadvantages: Policy support for utilisation is weaker than for storage; currently, the European Union’s legislated CO2 utilisation mandate is unique – and it only covers aviation e-fuel

- Cost issues: e-fuel pathways are immature and rely on expensive green hydrogen and renewable power; e-fuel is not expected to be directly competitive with traditional fuels through 2040

- Immature markets: Decarbonised commodities have yet to be commercialised at scale – it remains unclear whether price premiums for decarbonised goods will justify higher costs

- Co-feed limitations: While partial decarbonisation through co-feeding of CO2 is achievable at low cost, full decarbonisation of production is expensive and limited in scope and volume

Overall, declines in feedstock and technology costs and the development of strong policy incentives will be crucial if CO2 is to become a legitimate, widespread enabler of carbon capture deployment.

Don’t forget to fill out the form at the top of the page to access your complimentary extract from the report. This includes a range of charts illustrating the economics involved in the potential of CO2 utilisation as an enabler of carbon capture.