IRA set to increase cumulative US wind energy installations by over 50% in the next five years

Our new report, in partnership with the American Clean Power Association, uncovers insights on the surge in offshore wind projects, the revival of onshore markets, and the booming repowering sector, all fueled by strategic policy shifts and significant investments

2 minute read

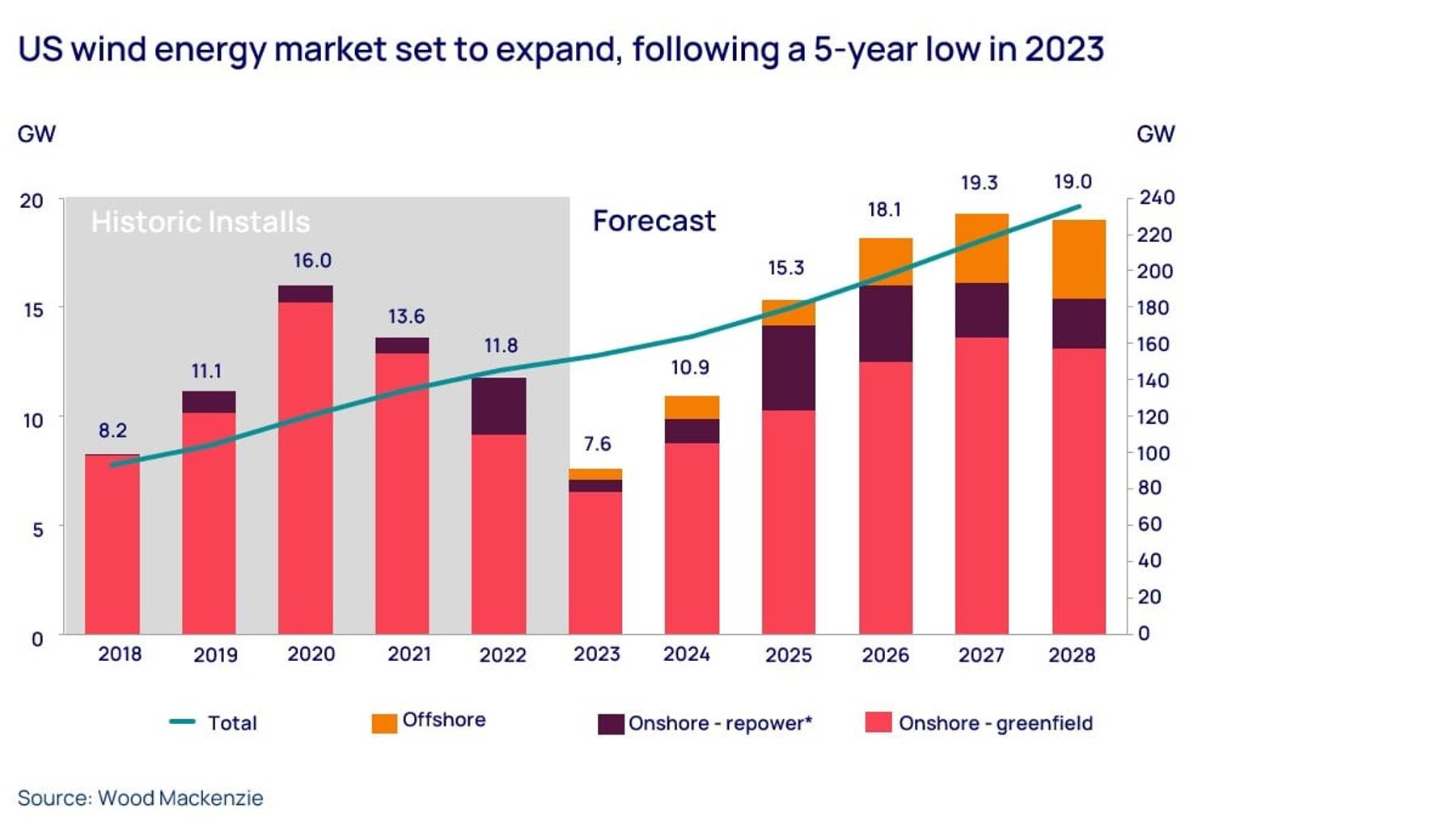

The US Wind Watch, a new report released by the American Clean Power Association (ACP) and Wood Mackenzie, is forecasting over 90GW of wind energy will be installed within the US by the end of 2028, including offshore wind projects, onshore wind development and repowering of aging wind farms.

The groundbreaking report leverages the industry-leading market insights from Wood Mackenzie, combined with the deep industry network of the American Clean Power Association. To download your complimentary extract, fill out the form. Or, read on for a summary of some of the key takeaways.

{kind=link}

The US offshore market is set to take off, with the first commercial scale offshore wind projects currently under construction. By the end of 2028, the report forecasts that nearly 12 GW of offshore wind projects will be operational, across seven different states on the Atlantic coast. The offshore wind market faces several significant challenges, including project economics, regulatory hurdles, permitting timelines and supply chain constraints. Despite these challenges, nearly 30 GW of offshore wind capacity has commercial potential by the end of the decade. Reaching this potential requires positive movement by policymakers at the state and federal level and significant investment from within the offshore wind supply chain.

The US onshore market will also rebound, following a low-point of 6.5 GW in 2023, to exceed 13 GW annually by the end of 2028. This increase in market activity is reinforced by the long-term extension of the Production Tax Credit (PTC), that was passed within the Inflation Reduction Act (IRA) in 2022.

The interconnection queues are full of onshore wind projects, and the promise for meaningful queue reform has the potential to unlock significant additional wind capacity. While Texas has been the wind leader with over 28% of the existing US installed base, the state will contribute just 15% of the 5-year forecast, due to congestion and transmission constraints. The West, Plains and Midwest will collectively drive over 67% of the five-year forecasted onshore wind energy installs. Massive onshore wind projects in these regions with dedicated transmission access will have an outsized role in the onshore wind outlook.

Repowering of aging wind assets is also expected to see tremendous growth in the US, thanks to the passage of the Inflation Reduction Act. Many assets over 10 years old can qualify for an additional 10 years of the PTC by making major upgrades to existing equipment, including new blades, drivetrains or nacelles. These upgrades promise better performance and improved reliability on the aging fleet.

Repowering has experienced significant success under the previous PTC regime, but a new wave of wind projects are now eligible for repowering and are expected to take advantage of this incentive. Repowering is expected to be performed on over 30 GW, or 20%, of the existing US onshore wind energy fleet by the end of 2028.

Learn more

The new US Wind Watch report will be released jointly by ACP and Wood Mackenzie. The report will be made available to existing ACP member companies and included in our Wind Energy Research subscription.