2024 tight oil costs: the push and pull between efficiency and OFS rates

Are efficiency gains enough to offset price inflation?

4 minute read

Authors: Atif Chaudhry, Senior Research Analyst, Supply Chain, Ben Hirschman, Senior Analyst, Supply Chain, Caitlin Shaw, Director - Research, WMC, Damola Olayinka, Research Analyst, WMC, Nathan Nemeth, Principal Analyst, Tufayl Khan,Sales Associate, Supply Chain.

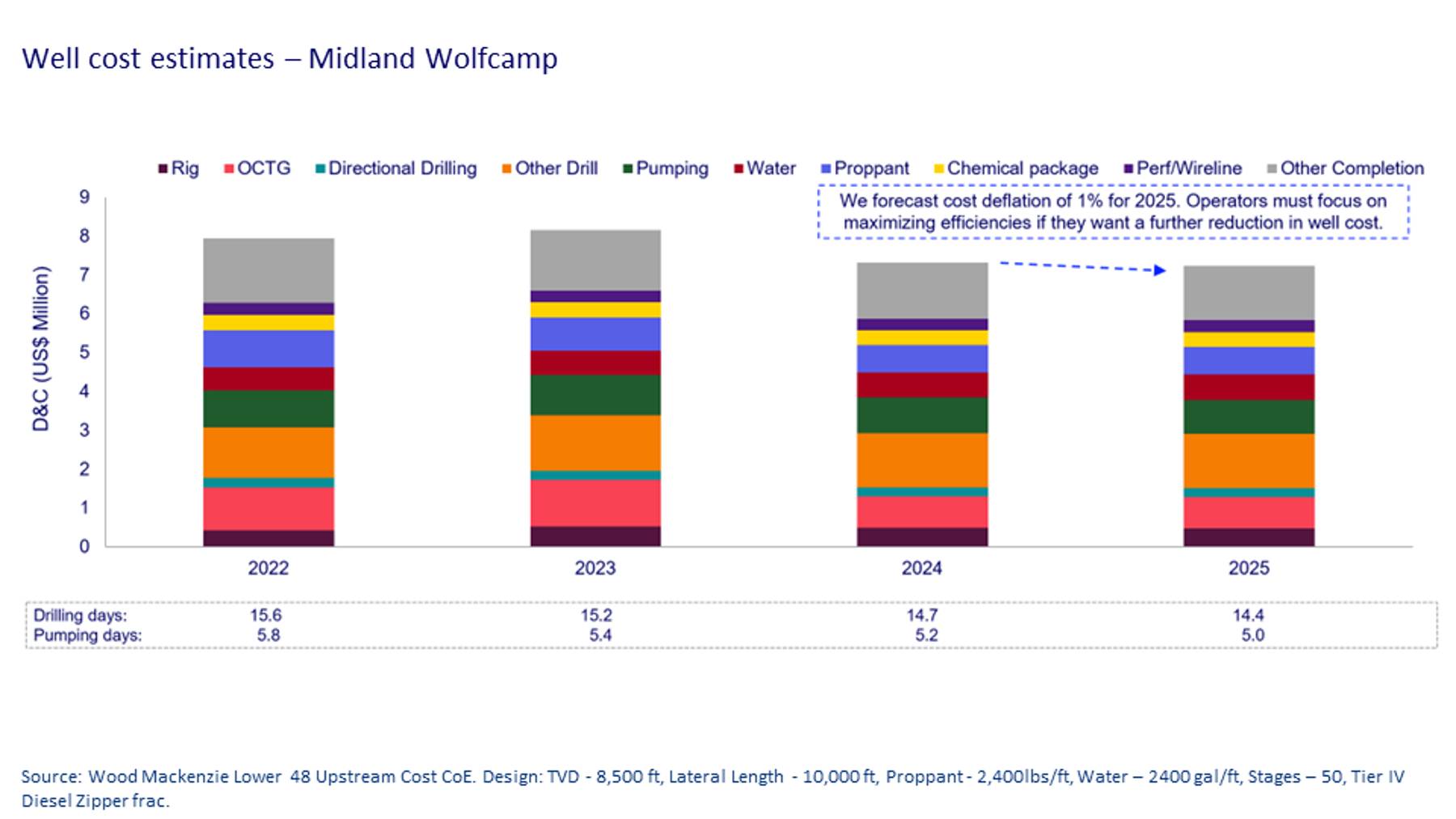

After peaking in 2023, Lower 48 well costs are expected to decline 10% in 2024 and 1% in 2025. Declining input pricing for oil country tubular goods (OCTG), proppant and diesel, combined with substantial drilling and completion efficiency gains, are pushing costs lower. Rig and pressure pumping rates are trending lower but have remained mostly sticky, as demand for high-performance and technology-focused equipment remains strong.

Despite this deflation, well costs do not return to levels seen in 2020 and 2021. Continued cost reduction must come from additional efficiency improvements as OFS pricing is unlikely to fall significantly. Download complimentary slides from our 2024 tight oil costs presentation by completing the form above. Or, continue reading for detailed insights.

{kind=link}

Efficiency gains help reduce well costs and equipment demand

Both E&Ps and service providers are emphasising significant efficiency improvements, albeit for different reasons. More efficient operations are helping E&Ps drill and complete wells faster, cutting costs. At the same time, OFS firms are utilising more efficient kit and workflows to sustain elevated prices, keeping margins high. Since 2020, rig efficiency has increased by over 30% and pressure pumping efficiency has increased between 30% and 100%, depending on the technology used.

Efficiency gains are not to be confused with one-to-one improvements in well costs. Drilling and pumping efficiency gains are key to cost improvement but only influence 40% of D&C spend. For example, a 10% efficiency improvement yields a 4% decrease in total D&C cost. Costs for OCTG, cement, water, proppant, and chemicals are not affected by variability in drilling and completion times.

Each E&P is at a unique stage in its cost journey

Operators are looking for step-change cost savings that are sustainable through market cycles. The deployment of “simul-frac” and “trimul-frac”, completing two or three wells at once, provides step-change savings. These techniques increase pumping hours per day, reducing spend on idle time and fuel. Fewer completion days save money on rentals and ancillary services.

The adoption of new electric pumping units has accelerated the trend of faster, cheaper, and more reliable operations with fewer emissions. Electric units use smaller pads that require fewer crew members and less routine maintenance. Cheaper fuel for natural gas and electricity replaces high diesel costs, and mobilisation and non-productive time on location are minimised. Operators that have adopted electric frac spreads and simul-frac have already released significant cost savings. Choices on completion technique and equipment type result in a cost range of US$100/lateral ft.

Not all operators will release lower costs. The largest producers with the scale to commit to longer-term contracts (one to three years) for new equipment and technologies will release additional efficiency gains and keep costs lower.

Activity gradually increases through 2025 but remains well below late-2022 levels

M&A consolidation, softening oil and gas prices, efficiency gains and high costs all contributed to the rig count falling in 2023. We forecast rig demand to increase by 40 units by the end of 2025 led by gas plays and the Permian.

But faster drilling operations mute the need for even more rigs. With roughly 550 active Lower 48 horizontal rigs, a 5% improvement in drill speed equates to about 28 fewer rigs needed in the market. With Lower 48 activity relatively flat, service providers will look to keep utilisation rates high to preserve prices and margins. Service rates are forecast to remain steady as the super-spec rig market remains tight and service providers have locked in Frea multi-year contracts for new electric pressure pumping equipment.

The push and pull between efficiency and OFS rates

Future cost trends depend on the outcome of the battle between efficiency and gradually rising unit pricing. This means price trends will be operator-dependent based on the technology and equipment used. OFS providers will look to defend and try to expand margins. With stronger balance sheets, anticipated increases in activity levels, and high demand for their most efficient equipment, they will feel less need to concede.

The largest producers with the scale to commit to longer-term contracts (one to three years) for new equipment will release additional efficiency gains and keep costs lower. The most in-demand equipment will be high-spec, efficient and enable lower emissions. Simul-frac and trimul-frac will be the industry standard. AI, machine learning, downhole monitoring, and big data could unlock further upside. Smaller producers will be most exposed to inflation headwinds — arguably motivating even more M&A.

Finally, oil and gas prices remain the most significant factor in D&C cost trends. Rising prices have a triple impact of higher input costs for fuel, higher indirect transport costs and higher activity levels, increasing demand for oilfield materials and services.

Remember to fill out the form at the top of the page to download a complimentary selection of slides from our 2024 tight oil costs the push and pull between efficiency and OFS rates presentation. This content includes a variety of charts and data, providing a deeper exploration of these themes.