Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Global CCUS investment requires US$ 196B through 2034, according to Wood Mackenzie

Government support in key countries at US$ 80B, North America and Europe most active regions

2 minute read

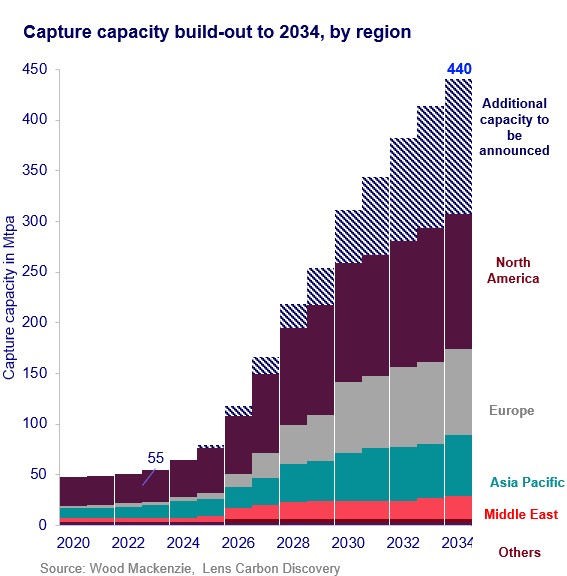

By 2034, global carbon capture capacity will reach 440 Mtpa and storage capacity will reach 664 Mtpa, requiring US$ 196 billion in total investment, according to a recent report from Wood Mackenzie.

According to the report “CCUS: 10-year market forecast”, nearly half of the investment globally is associated with CO2 capture, with the remaining US$53 billion from transport and US$43 billion from storage. About 70% of the investment will be in North America and Europe across the value chain.

“This is a huge ramp-up from where the industry is today. Government funding plays a critical role in driving the first wave of CCUS investments,” said Hetal Gandhi, APAC CCUS lead with Wood Mackenzie. “We see governments offering capex grants, opex subsidies, tax incentives and contracts for differences for CCUS. While no single mechanism has been used predominantly and each country devises novel methods to incentivise investments, nearly US$80 billion is directly committed to CCUS across five key countries.”

The US leads in funding at 50%, followed by the United Kingdom at 33% and Canada at 10%.

“While we are seeing strong support in countries like the US, government support in APAC lags behind,” said Stephanie Chiang, research analyst, CCUS. “Australia, Malaysia and Indonesia have announced some benefits, but they are substantially lower as compared to their investment needs. Australia’s direct incentives at US$40 million is less than 1% of the investment needed over the next 10 years.”

Capacity not keeping up with demand

Despite the large, forecasted increase in projects, Wood Mackenzie does not expect supply of carbon capture to meet demand. Industries will need up to 640 Mtpa of carbon capture capacity by 2034 as they look to decarbonize, but the projects expected to come into operation fall around 200 Mtpa short of that.

“Of the projects already announced and expected to go ahead in the development pipeline, 71% are in North America and in Europe,” said Hetal. “Government incentives such as the US Inflation Reduction Act (IRA), UK business models, Canada’s Investment Tax Credit and the Netherlands SDE++ scheme are moving projects towards final investment decision ( FID). We also expect a further boost to European projects due to the recently announced EU Industrial Carbon Management Strategy.”

Continued Hetal, “The lack of CCUS announcements in APAC’s largest emitting countries – China and India – is causing the region to have substantially lower capacity than needed under Wood Mackenzie’s base case. Key sectors like power and chemicals will see a large gap between demand potential and actual supply until 2034. We expect APAC’s capture pipeline will mature through additional announcements later in the decade.”

The report also sizes the global storage capacity to reach 664 Mtpa in 2034, with almost 80% of the planned pipeline starting up by 2030. CO2 storage projects will outpace emitter uptake, leaving a global capture-storage gap of more than 200 Mtpa by 2034.

“With storage capacities more concentrated than the spread-out capture capacities, hub-based storage ecosystems will evolve especially in Europe and APAC,” said Fauzi Said, senior research analyst.

Policies for transportation of CO2 across borders and bilateral agreements handling of liability risk remain key areas to watch out in the medium term.