CCUS: the US$196 billion investment opportunity

Exploring the ten-year forecast for carbon capture and storage capacity build-out and investment opportunities across countries and sectors

2 minute read

Hetal Gandhi

Lead, Global forecasting and Asia Pacific Research, Carbon Mitigations

Hetal Gandhi

Lead, Global forecasting and Asia Pacific Research, Carbon Mitigations

Hetal leads CCUS for APAC with a growing team of analysts to help clients in decision-making and business planning.

View Hetal Gandhi's full profileCarbon capture, utilisation and storage (CCUS) will be critical to delivering net zero, providing the means for essential hard-to-abate sectors to decarbonise rapidly. So, what’s the outlook for this essential technology over the next decade, and what regulation and policy support is being put in place to make it happen?

Drawing on insight from Lens Carbon, our CCUS: 10-year market forecast provides an in-depth macro- and micro- level analysis of the global CCUS landscape. Fill out the form at the top of the page to download a complimentary copy of the executive summary of the report, or read on to learn about one key finding.

CCUS: a US$196 billion global opportunity over the next decade – government support in key countries amounts to US$80 billion

There is still much debate about the role of CCUS in decarbonising the global economy. Some insist it should be strictly an interim technology for hard-to-abate sectors including cement, chemicals, steel, refining and power generation. Others see it as a deep decarbonisation tool.

Either way, for CCUS to fulfil its potential over the next ten years, several conditions must be met. To deploy CCUS at scale, heavy emitters must be motivated to decarbonise, the technology must be cost-effective and efficient, and a viable option for utilisation or storage must be available.

We project CCUS will represent a US$196 billion investment opportunity globally over the next decade. Our analysis indicates a risked investment pipeline of US$143 billion, with additional investments of US$53 billion expected to make up the rest of the total.

Nearly half of that amount is associated with CO2 capture, with US$53 billion from transport and US$43 billion from storage. About 70% of the investment will be in North America and Europe.

{kind=link}

The expected pace of CCUS deployment will be driven by the level of regulation and support in different countries. The US and Canada have robust regulatory and funding mechanisms in place to drive development and implementation, as does the European Union and the UK. In APAC, while regulatory momentum is strong in Australia, Japan, South Korea and Indonesia, government incentives are needed to accelerate CCUS development.

In contrast, development in China, India, Latin America, the Middle East and Africa is limited by a lack of firm policy, regulatory frameworks and funding support.

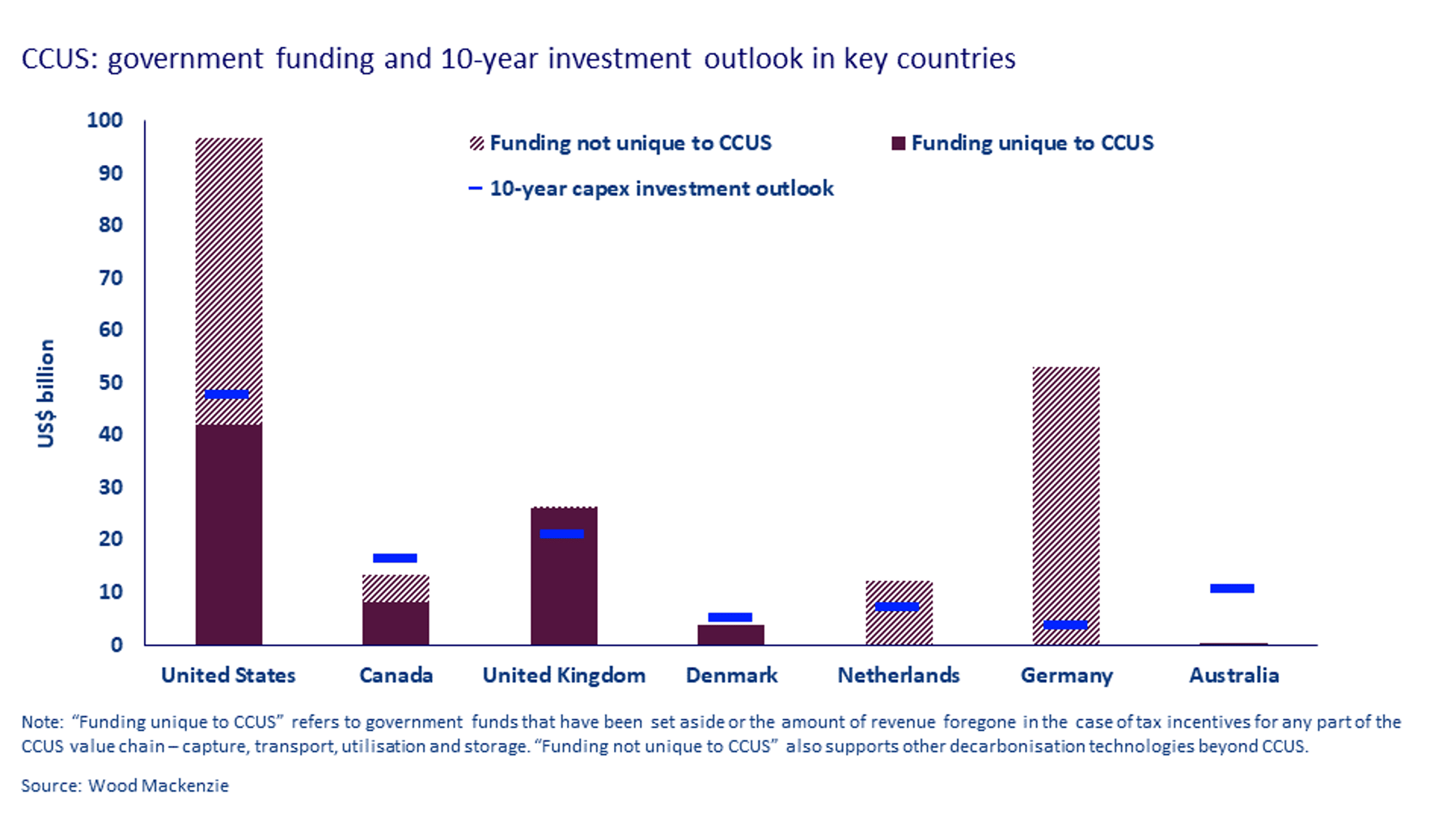

Announced government funding specifically for CCUS across key countries – including the US, Canada, the UK, Denmark and Australia – amounts to around US$80 billion. The US leads funding with a 50% share of the total, followed by the UK at 33% and Canada at 10%.

In addition, many countries have further funding available not unique to CCUS but applicable to decarbonisation technologies in general. Approaches vary, with countries devising a range of novel methods to incentivise investments. These include tax incentives, direct capex grants, contracts for difference and loan-related support.