Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Global nuclear SMR project pipeline expands to 22 GW, increasing more than 65% since 2021

The project pipeline requires investment equivalent to US$176B; uranium supply remains a challenge

2 minute read

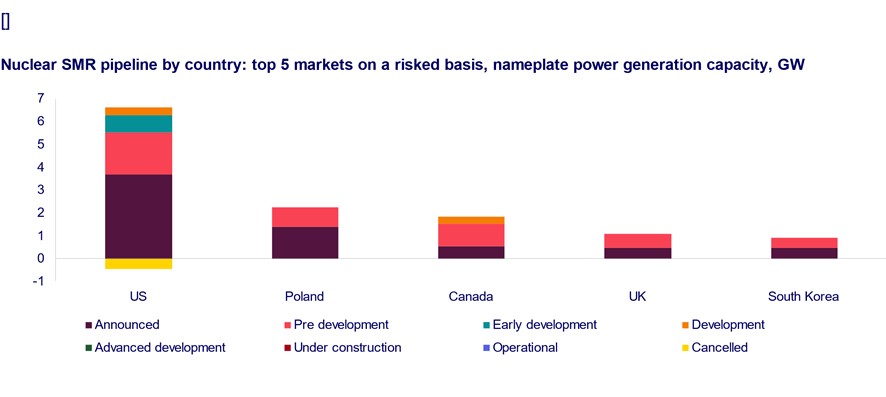

The small nuclear reactor (SMR) project pipeline reached 22 GW in the first quarter of 2024, an expansion of 65% since 2021, according to a recent report by Wood Mackenzie. The current total project pipeline would require an investment of close to US$176 billion.

“The nuclear power market has been gaining momentum as a key strategy to achieving net zero,” said David Brown, Director, Energy Transition Service at Wood Mackenzie. “While the sector has faced a range of challenges over the last 12 months, especially the cancellation of NuScale’s Clean Power Project, multiple markets across the world are expanding their focus on nuclear SMRs,” said Brown.

According to the report, “SMR nuclear market update: 2024”, five countries - the US, Poland, Canada, the United Kingdom, and South Korea - drive 58% of the risked project pipeline.

“COP28 also provided a new tailwind for nuclear with a new goal to triple nuclear capacity by 2050. In Wood Mackenzie’s net zero scenario, SMRs would account for 30% of the nuclear fleet. The global focus on net zero means the market for SMRs has widened from utilities to industrial and technology companies. For these sectors, SMRs provide a range of solutions, including around-the-clock carbon-free power, carbon-free industrial heat, and the ability to meet power demand growth long term; the latter is a particular area of focus in the US with increasing demand for high-capacity data centers,” said Brown.

Policy support essential

Policy support is crucial to accelerating projects to final investment decisions. Some regions have put new policies in place that have spurred the recent activity. Most notably, the US, the United Kingdom and Japan.

- In the US, the Inflation Reduction Act provides a 30% ITC for a zero-emission advanced nuclear power plant to be implemented after 2025. More ITC incentives include a 10% ITC for domestic content and a 10% ITC adder for building an SMR on the site of a retired coal plant.

- In Japan, after fierce public opposition, pro-nuclear sentiment has strengthened following the election of Prime Minister Kishida and amid record-high commodity prices in 2022.

- In the UK, government targets and reactor funding has been set as part of the nation’s path to net zero. The UK has awarded almost US$80 million to GE-Hitachi and Holtec International for SMR feasibility analysis.

“Across the world, governments are stepping up in various ways,” said Brown. “The recent momentum in SMR announcements is a result of strong public and private partnerships involving both established and new companies in the nuclear sector.”

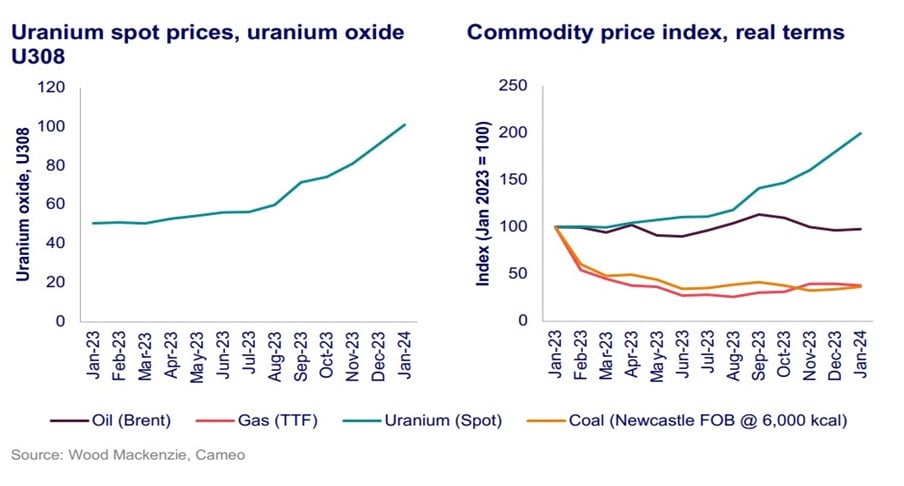

Supply challenges build

Concerns around uranium supply availability and rapidly escalating uranium prices present challenges to the nuclear sector as a whole. In 2023, uranium was the strongest performing commodity, with prices soaring.

“The uranium market is turning bullish, driven by production shutdowns, potential sanctions on Russian uranium supply, the addition of 8 GW of large-scale new nuclear capacity in 2023, and lifetime extensions of the current nuclear fleet,” said Brown. “In turn, this has ignited concerns about uranium supply security across the OECD nations. As a response, there are plans from both governments and the private sector to fund expansions of the uranium supply chain.”