Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Global energy storage integrator market grows increasingly competitive in 2022

Market expected to consolidate in the short and middle term

3 minute read

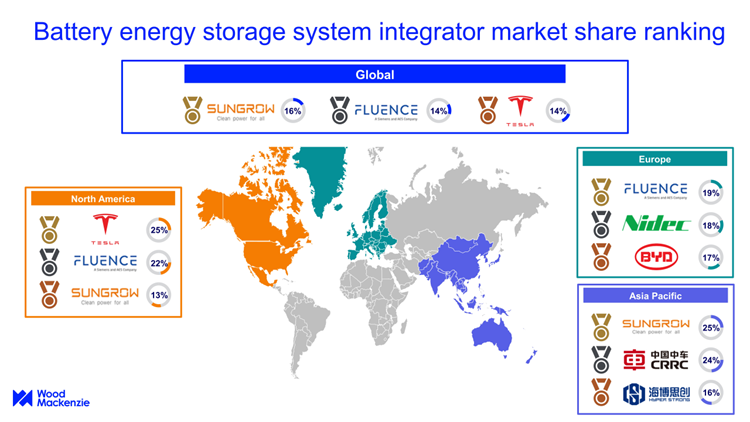

The global Battery Energy Storage Systems (BESS) integrator market has grown increasingly competitive in 2022, with the top five global system integrators accounting for 62% of overall BESS shipments (MWh), according to latest analysis by Wood Mackenzie.

Leading vendor, Sungrow dominated the market with 16% of global market share rankings by shipment (MWh), jointly followed by Fluence (14%) and Tesla (14%), Huawei (9%), and BYD (9%).

Kevin Shang, senior research analyst at Wood Mackenzie, said: “As major policy developments propel the battery energy storage systems market, the BESS integrator industry is becoming increasingly competitive. While existing system integrators are striving to increase market share, the fast-growing energy storage market has also attracted many new entrants to this space.”

“A common feature behind the leading BESS integrators is that their global presence allows them to access a larger customer base and unlock additional revenue streams. In addition, many BESS integrators have been seeking to enhance the vertical integration of their supply chain.”

Commenting on the supply chain, Shang added: “While global battery supply eased in 2023, after experiencing supply tightness the previous year, the limited supply of transformers has become the new bottleneck of the energy storage supply chain. The industry is struggling with short supply and price spikes of transformers, with a minimum lead time of more than one year for transformers of all sizes. This has a direct impact on system integrators as transformers are integral for grid connection.”

Note: The market share calculation is based on integrators’ battery energy storage system shipment numbers in 2022; the number includes both grid-scale and community, commercial & industrial sectors. Source: Wood Mackenzie

North America leading the way

The North American BESS integrator market is concentrated, with the top five players holding 81% of the region’s market share in 2022. Tesla led the region with 25% market share rankings by shipment.

“Being the world’s most vertically integrated energy storage provider, Tesla has a key advantage. Importantly, by integrating hardware, software and added services, Tesla can deliver continued improvements and new features to clients quickly.”

Following Fluence (at 22%), Chinese company Sungrow held its third position with a 13% market share in the North American market in 2022. This high ranking is largely attributed to the company’s cost competitiveness and advanced liquid-cooling products.

“The Inflation Reduction Act (IRA) and state-led clean energy policies will drive growth in the storage market. We forecast that the competition in the US BESS integrator market will become increasingly over the coming years. Companies need to act on a robust business strategy to succeed in a highly competitive market.”

Asia Pacific

China led the Asia Pacific BESS integrator market, with an 86% market share in 2022.

Shang said: “China’s integrator market is becoming increasingly competitive, squeezed heavily by both upstream and downstream supply chain participants. Possessing manufacturing capacity on key components, like cell, PCS, BMS and EMS, tends to be a necessity rather than a plus as bid requirements for energy storage projects become more detailed and stringent.”

Facing the trend of energy storage product homogenisation, price has become the most significant distinction and key winning bid factor in the region.

Shang added: “The price war among system integrators has started in China. We’ve observed an increasing number of players willing to sacrifice profits in exchange for market share, dragging down the profitability of the whole industry. However, we forecast that aggressive bid strategies with little margin will not be sustained. Intensifying market competition will make it difficult for companies with low profitability and no clear competitiveness to survive over the coming years.”

- ENDS –

EDITOR’S NOTES

Report methodology

Wood Mackenzie’s BESS Integrator market share rankings are based on the number of BESS shipments in megawatt-hour (MWh) in 2022. Only shipments with revenue recognised in the reporting year are counted towards the market share. The number included both grid-scale and CCI sectors.

The ranking is built upon careful tracking of the global landscape. Wood Mackenzie’s primary data collection comes from annual BESS integrator surveys, public filings, project databases and discussions with system integrators, EPC providers and project developers. Where necessary, market-based estimates are made.