Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

India needs radical transformation to reach net zero emissions by 2070

4 minute read

How can India attain its net zero emissions goal by 2070, in line with global pledges to reach net zero emissions by mid-century? Wood Mackenzie analyses the scenario in its latest report ‘India energy transition pathways 2070i’, concluding that the country must radically transform its energy landscape and prioritise renewable energy, electrification, hydrogen adoption, and carbon removal strategies.

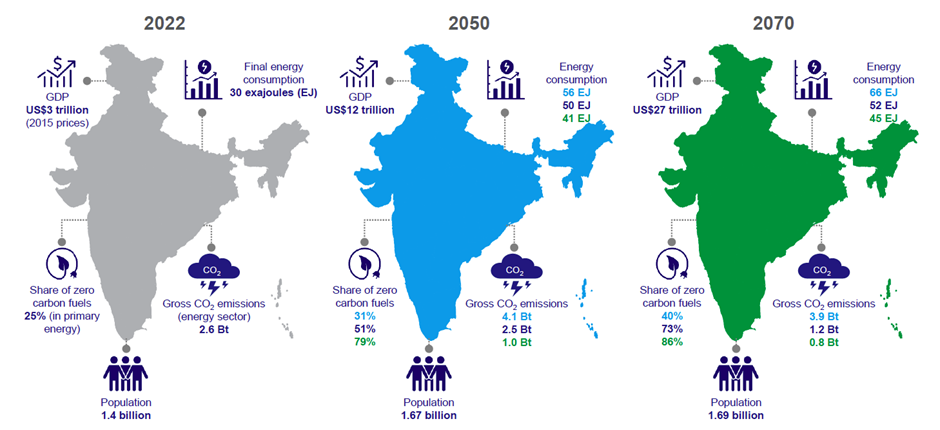

As the world's most populous country, India's energy landscape is on the brink of a radical shift, with an anticipated population increase of a quarter billion by 2070 and projected gross domestic product (GDP) growth from $3 trillion to approximately $27 trillion.

Roshna N, research analyst, Energy Transition Service for Wood Mackenzie, said: “Under Wood Mackenzie’s 2°C energy transition scenarioii, India’s energy demand will increase from 30 exajoules (EJ) in 2022 to 52 EJ by 2070. However, CO2 emissions will decouple from GDP in the early 2030s and slowly decrease from 2037, resulting in 1.2 billion tonnes by 2070. Using Carbon Capture, Utilisation, and Storage (CCUS), direct air capture (DAC) and nature-based solutions will be necessary to reduce residual emissions.”

India in 2022, 2050 and 2070, under Global Energy Transition 2.5 °C, 2 °C and 1.5 °C pathways

Source: Wood Mackenzie Energy Transition Service

The report discusses five strategies for India to reach net zero emissions by 2070, which are;

Profound changes for zero emissions

Wood Mackenzie’s analysis concludes that to achieve net zero, India will need to transition from predominantly fossil fuels to zero-carbon fuels. To achieve net zero emission by 2070, 73% of primary energy supply will need to generate from zero-carbon sources. This shift will require a fivefold increase in electricity generation, with 93% of it coming from non-fossil sources. Also, low-carbon hydrogen will cover 11% of energy demand, while bioenergy will make up 12% of non-fossil fuel energy.

At the same time, the fossil fuel share of final energy demand needs to decrease from 72% today to 27% by 2070. Coal demand peaks by 2030 and drops to 25% of current levels by 2070, mainly focused on industrial subsectors. While natural gas will serve as a transition fuel, with demand rising until the 2040s – a 60% jump from current levels.

Hydrogen and carbon capture

To achieve net zero, annual low-carbon hydrogen demand would need to reach 30-40 million tonnes by 2050 and 85-90 million tonnes by 2070. CCUS will also play a significant role, with a projected annual capacity of 700-750 million tonnes by 2070, according to Wood Mackenzie’s AET-2 scenario.

Additionally, clean hydrogen holds immense potential as a versatile and dispatchable power generation source. Using captured CO2 in the cement and petrochemical sectors further enhances sustainability efforts.

“In the journey towards emissions reduction, low-carbon hydrogen and carbon capture play pivotal roles in decarbonising hard-to-abate sectors like steel and cement. The recent Energy Conservation (Amendment) Act 2022, Carbon Credit Trading Scheme 2023, and subsidy schemes for low-carbon fuel production act as strong drivers, propelling the adoption of low-emission energy sources, notably low-carbon hydrogen. While there is progress, India needs to put the right policy frameworks, and consumption mandates for low-carbon hydrogen, and accelerate the development of CO2 storage projects,” Roshna added.

In addition, nature-based solutions, mainly from forestry projects, can provide 200 million tonnes per annum (Mtpa) of potential sink capacity longer term.

Electric vehicles and the materials transition

Under Wood Mackenzie’s AET-2 scenario, electric vehicles (EVs) will be crucial in decarbonising the economy and will create massive investment opportunities in the EV, battery, and renewable energy sectors. Iron-based cells will likely account for a considerable proportion of installed EV batteries in the long term. If commercially extracted, the substantial lithium deposits identified in the Jammu and Kashmir regions will significantly bolster India’s self-sufficiency in battery raw materials.

New industries and business models on the path to net zero

India’s pathway to net zero will embrace niche and emerging technologies, including nuclear (in the form of small modular reactors, or SMRs), geothermal, and offshore wind, which will become mainstream contributors as part of India’s pathway to net zero.

Ensuring India’s energy security

“India is taking proactive steps to revise its energy security plan in light of recent global events, such as Russia’s invasion of Ukraine and the unprecedented surge in coal and gas prices. The country is embracing low-carbon technology and bolstering local production while continuing to import oil and gas. Despite geopolitical shifts, India remains steadfast in its commitment to a resilient energy strategy,” said Roshna.

Roshna concluded: “India is moving towards achieving its net zero goal by 2070 by introducing the Net Zero Bill in parliament. As a major energy and commodity importer, India’s efforts to rapidly reduce carbon emissions have significant global implications. India needs to focus on low-carbon energy projects and revamp its energy landscape to achieve this.”

ENDS

Editor’s Notes:

- Wood Mackenzie’s India energy transition Pathways 2070 report is based on scenario modelling drawn from Wood Mackenzie’s Global Net Zero Pledges; first edition published December 2022. Our analysis of modelling results suggests the scenario is equivalent to our Accelerated Energy Transition 2 ˚C (AET-2) warming pathway.

- Wood Mackenzie’s AET -2 scenario shows our view of a possible state of the world and of the energy industry that is consistent with limiting the rise in global temperatures since pre-industrial times to 2 degrees Celsius. There could be multitude of potential pathways for meeting that condition, and the AET-2 scenario represents our interpretation of the likeliest route, given the policy drivers and technological innovation required. We do not assign a probability to the likelihood of any scenario being realised.