Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Johor's data centres could consume 40% electricity demand by 2035, testing grid expansion plans

Power supply remains adequate in the near term, but grid infrastructure is becoming a critical bottleneck

1 minute read

As Southeast Asia's fastest-growing data centre hub and one of Asia's most attractive locations for new data centre investment, Johor is rapidly emerging as a critical digital infrastructure centre. According to a new Wood Mackenzie report, data centres could account for approximately 40% of the state's total electricity demand by 2035, fundamentally reshaping power consumption patterns and increasing pressure on grid infrastructure.

The report, Powering Johor's Data Centre Boom: Supply, Demand, and Grid Constraints, finds that while power generation remains sufficient to support near-term growth, access to transmission and distribution infrastructure is emerging as the primary constraint for new developments. As demand accelerates, grid readiness will play an increasingly important role in determining the pace of future investment.

Johor has attracted MYR165 billion (US$42 billion) in cumulative investment from hyperscalers and technology companies, supported by its proximity to Singapore, competitive operating costs and favourable policy environment. Data centre load in the state more than doubled between 2024 and 2025, and Johor now accounts for an estimated 51% of total data centre maximum demand across Peninsular Malaysia.

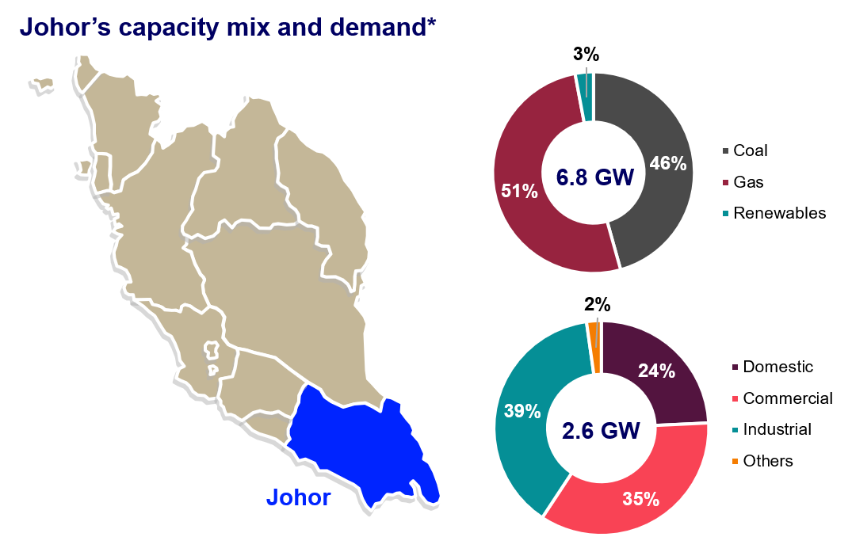

Wood Mackenzie estimates that data centre maximum demand in Johor has reached approximately 3.8 GW, equivalent to nearly one and a half times the state's current electricity demand. By 2035, data centres are expected to account for around 40% of Johor's end-user electricity consumption, up from approximately 24% today.

“Many investors still view power supply as the main hurdle for data centre development in Johor, but our analysis suggests the challenge is becoming much more localised,” said Alvin Tan, research analyst for power and renewables at Wood Mackenzie. “The issue is increasingly about where power is available rather than whether it is available. Areas attracting the highest concentration of data centre investment are also where grid infrastructure is under the greatest pressure, making transmission and distribution readiness a key determinant of future growth.”

Note: *Based on 2024’s official data from Energy Commission Malaysia.

Source: Wood Mackenzie

Grid bottlenecks emerge despite adequate power supply

Johor currently has approximately 6.8 GW of installed generation capacity, consisting primarily of natural gas and coal-fired power plants, alongside strong interconnection with the wider Peninsular Malaysia grid. Current electricity demand stands at approximately 2.6 GW, providing a healthy supply buffer.

However, Wood Mackenzie's analysis finds that system-wide capacity figures mask increasingly localised constraints. While overall transmission and distribution utilisation remains relatively low at around 30%, demand is becoming heavily concentrated around major data centre clusters, particularly in Sedenak Tech Park and Nusajaya Tech Park.

As a result, substations and grid connection points are becoming key bottlenecks for developers. The report identifies shortages in 132 kV main intake substations and limited availability of suitable nodal injection points in Johor, particularly for renewable energy integration, as the most immediate infrastructure challenges.

Potential solutions include higher-voltage 275 kV connections supported by on-site substations, greater deployment of decentralised solar generation for self-consumption, and longer-term development of dedicated renewable energy infrastructure serving data centre clusters.

*as of December 2025

Source: Wood Mackenzie

Coal retirements increase focus on future supply adequacy

While grid access is the most immediate challenge, the report highlights longer-term supply risks as existing generation assets retire.

Approximately 2.1 GW of coal-fired generation capacity in Johor is expected to retire during the mid-2030s. At the same time, reserve margins across Peninsular Malaysia are projected to tighten in the near term, driven by demand growth and the expiry of several major PPAs for gas-fired plants..

Wood Mackenzie identifies Malaysia's NewGen26 programme, an open tender for 6 GW to 8 GW of new gas-fired generation capacity, as critical to maintaining long-term reliability and supporting future industrial growth. The NewGen25 programme is expected to support near-term adequacy by extending the operation of selected gas-fired assets, thereby maintaining reserve margins at a healthy level. However, Wood Mackenzie identifies Malaysia's NewGen26 programme, an open tender for 6 GW to 8 GW of new gas-fired generation capacity, as critical to maintaining long-term reliability and supporting future industrial growth

The Southern Johor Renewable Energy Corridor (SJREC) is also expected to play an increasingly important role in the state's power mix. Planned developments in Mersing and Kota Tinggi could add up to 4 GWp of solar capacity integrated with battery storage, helping offset the impact of future coal retirements.

While these additions are expected to ease supply pressures from 2031 onwards, Wood Mackenzie's analysis suggests that continued investment in both generation and grid infrastructure will be required to support projected demand growth.

Supportive policy framework continues to attract investment

Johor remains one of Asia's most attractive markets for data centre investment, supported by a comprehensive package of incentives and regulatory reforms.

Key measures include preferential tax incentives under the Johor-Singapore Special Economic Zone (JS-SEZ), streamlined approvals through Malaysia's National Data Centre Framework, and Tenaga Nasional Berhad's Green Lane Pathway, which significantly reduces grid connection timelines for qualifying projects.

At the same time, policymakers are introducing stricter sustainability requirements. Malaysia is exploring the introduction of a carbon pricing mechanism, while water tariff reforms for data centres are being considered at the national level, alongside strengthened oversight of project approvals to ensure alignment between development plans and utility infrastructure readiness

Renewable energy procurement is also accelerating. As of June 2025, 1.3 GW of Corporate Renewable Energy Supply Scheme (CRESS) agreements had been signed in Peninsular Malaysia, all linked to data centre projects in Johor.

“The real test for Johor is not whether it can attract demand. The question is whether infrastructure planning can stay ahead of a pipeline that is growing faster than almost anywhere else in Southeast Asia.” said Tan. “Delays in substations, transmission upgrades or new generation projects could ultimately become the limiting factor on future expansion.”