Get in touch

-

Mark Thomtonmark.thomton@woodmac.com

+1 630 881 6885 -

Hla Myat Monhla.myatmon@woodmac.com

+65 8533 8860 -

Chris Bobachris.boba@woodmac.com

+44 7408 841129 -

Angélica Juárezangelica.juarez@woodmac.com

+5256 4171 1980

Wood Mackenzie predicts European gas demand will continue to fall, helping gas storage outlook for this winter and the following

European gas storage level on target for Winter, but high prices persist as uncertainty remains on weather and Russian supply

2 minute read

High natural gas prices will continue to drive down European demand to seven percent below the five-year average through March, leaving a best-case scenario of storage levels at 31% at winter’s end, in line with the five-year average, says Wood Mackenzie, a Verisk business (Nasdaq:VRSK).

These findings come from Wood Mackenzie’s ‘European Gas Q3 Short Term Outlook’ report released today.

Massimo Di Odoardo, vice president, Gas and LNG research for Wood Mackenzie said: “Strong LNG and non-Russian pipeline imports have helped get Europe gas storage levels to 80% at the end of August, beating expectations. We expect this to rise to 86% by the beginning of October. If Russian flows from Nord Stream resume at current levels following the three-day maintenance in September, Europe could be in a position to get through this and next winter without demand curtailments.”

This scenario considers gas demand reducing 7 percent through to March compared to the past five-year average – less than the 15% demand pledged by the EU – and record levels of LNG imports, facilitated by new LNG infrastructure next year. Under this scenario, gas storage levels are expected to refill to 90% ahead of winter 2023/24.

Risk of further supply disruptions or colder-than-normal weather

However, uncertainty does remain, as extremely cold weather this winter or reduced Russian flows could put Europe on a different trajectory. Di Odoardo added: “Should Nord Stream flows not resume following September maintenance, European inventories might still end up at 26% by the end of this winter, although they might only be able to get to 81% ahead of next winter.”

The biggest risk though, will be the weather. If the northern hemisphere has an extremely cold winter, increasing need for heating across Europe and Asia could add up to 30 billion cubic metres (bcm) to winter demand and risk reducing European storage inventories down to 4% by March and up to only 63% ahead of the start of following winter, inevitably resulting in demand curtailments.

Impact on prices

Penny Leake, Wood Mackenzie research analyst for European gas added: “In addition to uncertainty over gas supply from Russia, power market tightness - due to low nuclear, hydro and wind output - and the risk of electricity disruption are putting additional stress to gas prices futures this winter.”

“Under normal weather conditions we anticipate a rebalance of the power market after winter, which, combined with an improved gas market balance, might see gas prices dropping by more than 35%, trading closer to levels Europe had in late July 2022.”

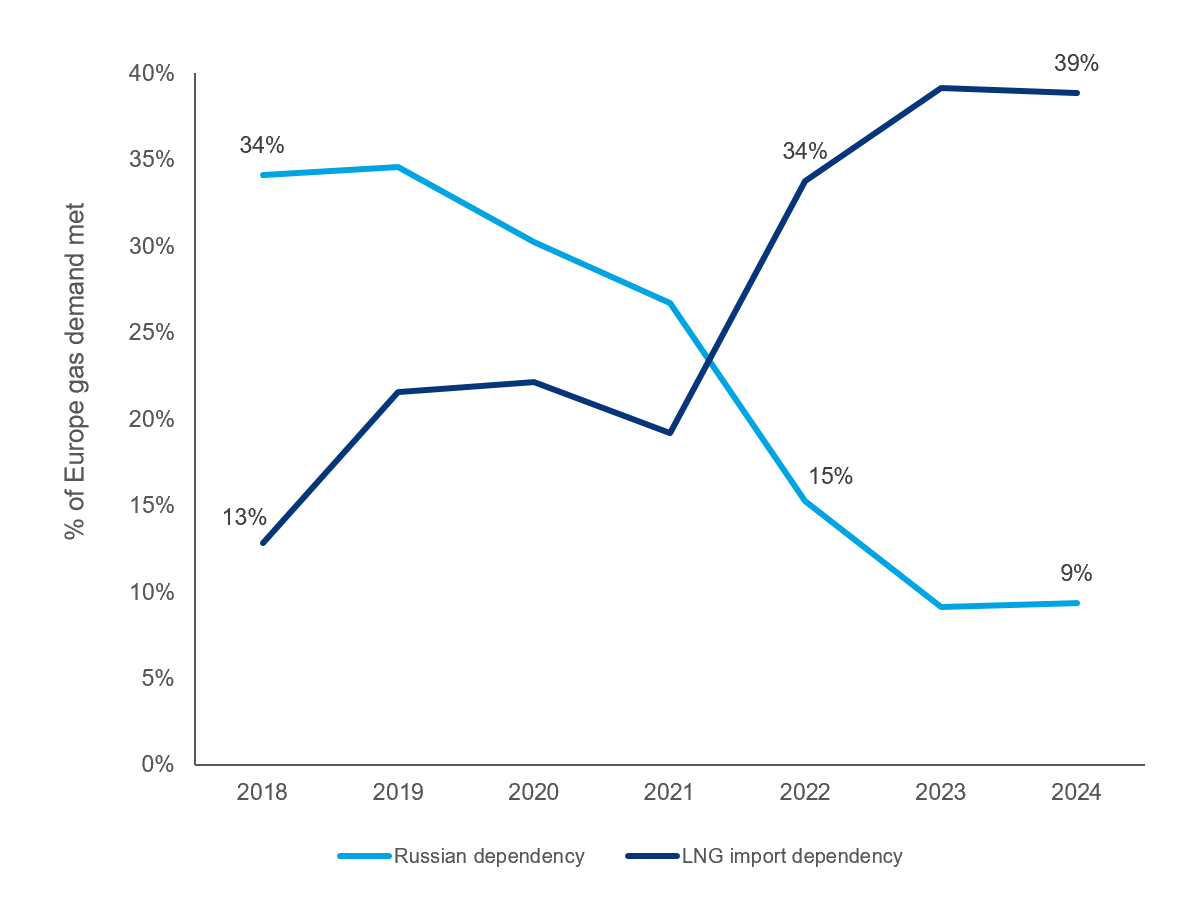

“However, Europe’s hope to get through this and next winters is predicated upon record LNG imports - expected to reach a 40% market share in Europe next year, while Russia reduces below 10%- requiring high gas prices and Europe remaining the LNG premium market globally.”

Europe import dependency: Russian pipe vs LNG