The Emergence of New Ethylene Powerhouses

Since the start of the decade when crude oil/gas prices ratios were higher and global ethylene demand was lower, the global ethylene industry has rebalanced and has even entered periods of tightness over the past few years, prompting fresh investment in new ethylene capacity. What can we expect from this current investment cycle?

1 minute read

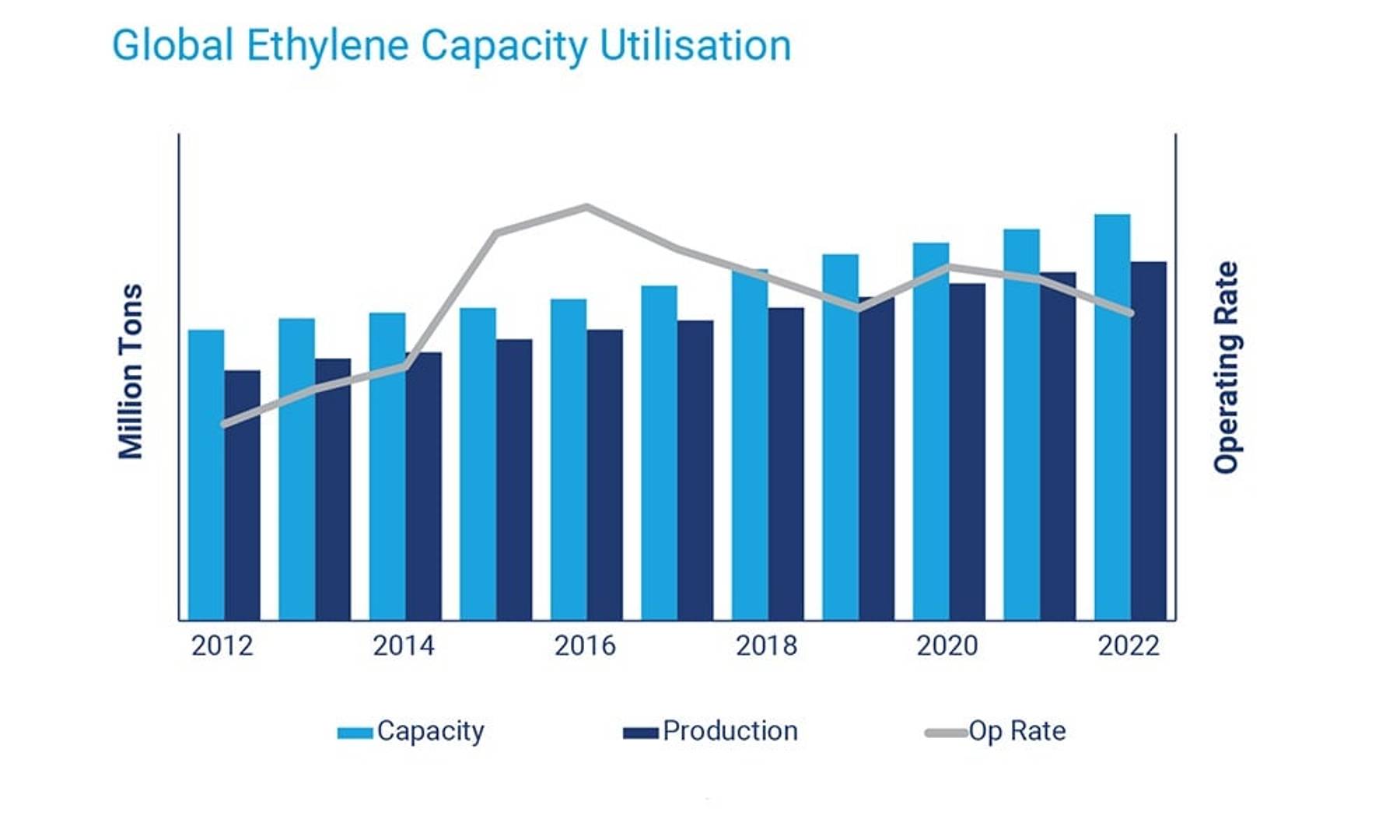

New ethylene production will come predominantly in the United States and Asia Pacific (particularly China), and to a lesser extent Europe and the Middle East. We currently expect that the global ethylene industry will be in a declining trend to 2019 and that operating rates will remain above 88% through 2022 — despite large ethylene capacity additions taking place globally.

Recent high operating rates are driven by a limited amount of ethylene capacity additions in the last 4-5 years relative to the demand growth observed. This places the industry in a good position as it enters this next trough in the ethylene industry cycle, which we expect to be relatively shallow and brief compared to previous down cycles.

{kind=link}

{kind=link}

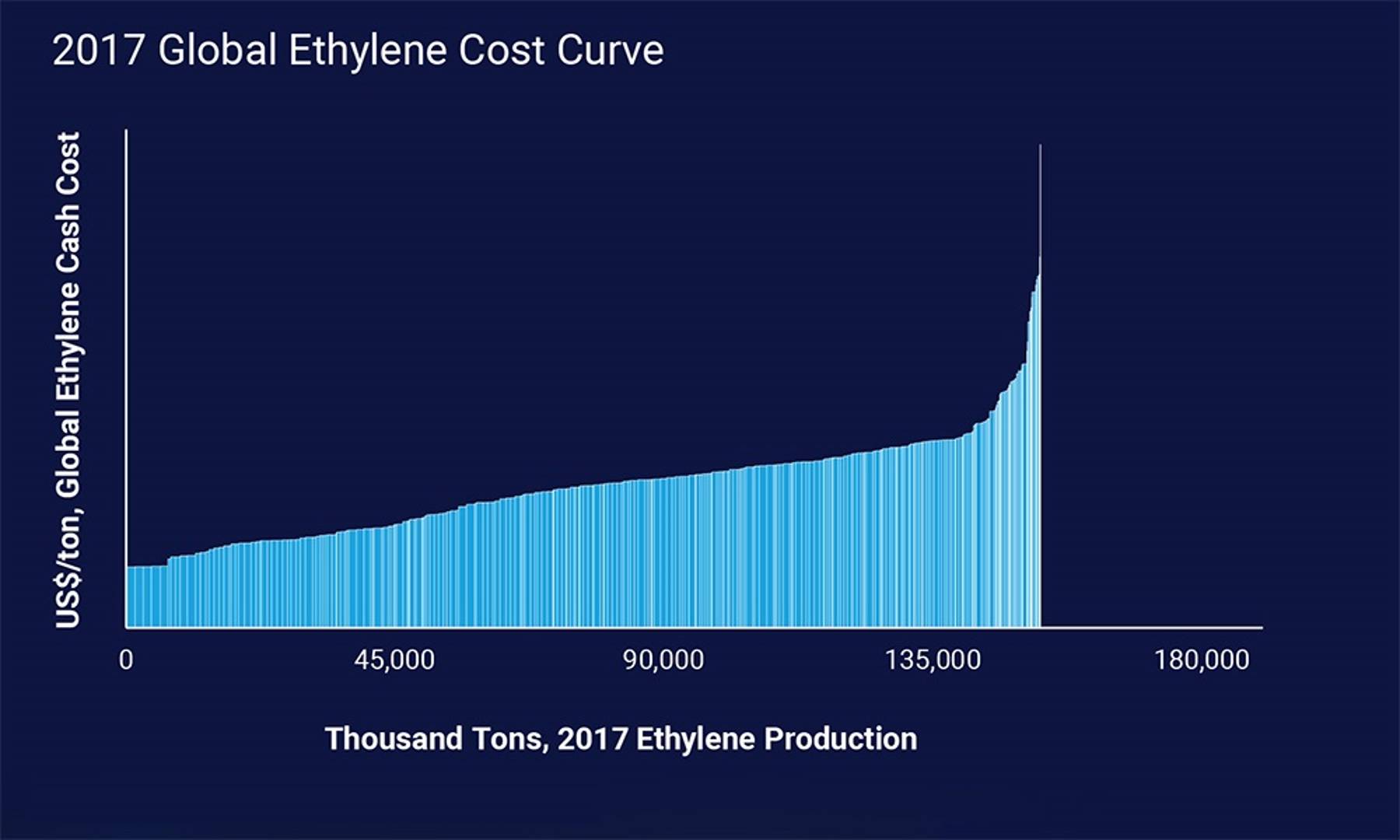

Our 2018-2019 price forecast for Brent crude oil (nominal dollars basis) is now US$55-60/bbl, while our 2020-2022 price forecast for Brent crude oil approaches US$80/bbl (Nominal). How will this effect the global ethylene cost curve and prices? What do these margin curves look like on a regional basis and where will the new projects be located?

Find the answers by completing the form to download our insight.