Discuss your challenges with our solutions experts

Will 2019 be another tumultuous year for the North American polyester industry?

6 key issues to focus on for 2019

1 minute read

In 2018, the North American polyester and upstream intermediates markets experienced major changes. Various plant outages tightened up the supply/demand balances, ownerships changed, PET resin pricing power shifted to producers, new fibre capacity was announced, and China's waste ban was implemented. All of this occurred in an uncertain and shifting economic and trade environment of the Trump Administration.

A collection of market events in 2018 were predictable but many were big surprises to the region's polyester chain. As we have seen in 2018, the North American polyester industry is full of surprises. Can we say from today's perspective that 2019 will simply be a repeat of 2018, or are new changes on the horizon? Below are the key issues to focus on for 2019.

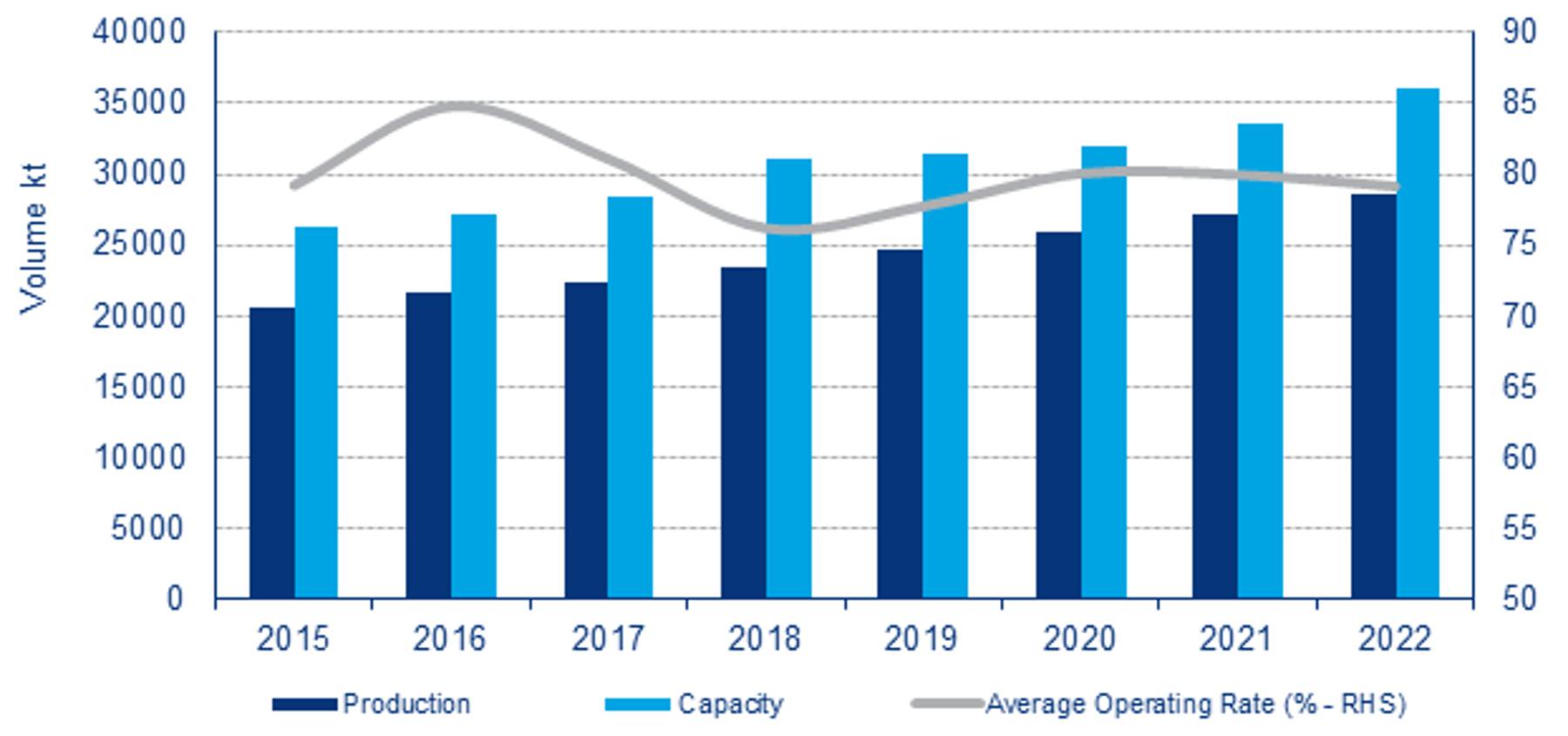

1. PET resin capacity constraints

There are no new PET resin capacity expansions expected to be added to the North American region in 2019. The Corpus Christi new PET resin plant is not expected to be operational until the second half of 2020 at the earliest, given the delays associated with the FTC review of the Corpus Christi Polymers 3-way JV. As a result, the regional PET resin supply/demand balance for 2019 and into 2020 is expected to stay very tight, with many of the same market dynamics that we have seen in 2018 repeated in 2019/2020.

{kind=link}

2. Tight PTA supply

Along with a tight regional PET resin market, the region's PTA supply/demand balance is also expected to remain very tight in 2019 and into 2020. As this segment of the industry ages, unplanned outages are likely to occur, especially when the plants are running hard. We can expect to see some creative juggling of PTA capacity between North American and Europe in order to meet domestic PTA requirements.

Is there enough PTA to go around?

Find out when you attend Wood Mackenzie's 2019 Americas Polyester Conference in Houston from February 27 to February 28.

Dr. Michael Bermish will be looking at the mid-term outlook for North American PTA supply and demand.

3. Global surplus of MEG

A global MEG surplus is projected for 2019 and a significant multi-million tonne surplus for beyond 2020. One million tonnes of new US MEG supply is to be added by Q1 2019 but only 27 kt of demand growth in 2019. The US adds another 1.6 million tonnes in 2019-2021 and a further 2 million tonnes after 2022. This is the beginning of an extended down cycle. Imports from Canada are likely to decline but US exports must increase. Swaps with the Middle East could reduce imports, saving duty, freight and storage MEG contracts will be more competitive reflecting export alternative values to China.

4. New polyester staple capacity

In 2019, the North American region's polyester staple market is expected to see its first new capacity addition in many decades. There are two new capacity additions, one geared to the low-denier polyester staple market and one geared to the low-melt polyester staple market. These new capacity additions coupled with new punitive anti-dumping duties and new high tariffs imposed on China (25% as of January 1, 2019) are expected to displace a significant portion of polyester staple imports. This has not been seen in many decades and could be the beginnings of a new paradigm for this segment of the polyester industry.

5. Regional RPET market changes

As of January 1, 2018 China imposed an import waste ban which has effectively eliminated rPET baled bottle exports from the US to China. China has been, by far, the largest importer of rPET baled bottles from the US, primarily from the West Coast. Currently, there are no significant substitute destination available for rPET baled bottle exports. This action by China has significantly altered the US West Coast recycling market dynamics and this will persist through 2019 and beyond. On the East Coast, the rPET market is being impacted by a tight virgin PET resin market, which has pushed many converters and thermoformers to look at the rPET market as an alternative and somewhat cheaper raw material. This will likely continue into 2019 and 2020 until additional capacity is added to the virgin PET resin market segment.

6. The overall regional economic outlook and the Trump administration

In 2018, US economic growth accelerated, boosted by the Trump Administration's Tax Reform bill. With incomes growing and the unemployment rate currently sitting below 4%, consumers' discretionary spending on textiles/apparel and single-serve beverages was strong in 2018. US economic growth is expected to slow in 2019 as the effects of the Tax Reform bill wanes, 'the Fed' continues its policy of normalising interest rates and the Trump tariffs begin to eat into global trade. This could be a constraining factor on consumer spending on polyester-related products next year.

Find out more about the North American polyester market at 2019's Wood Mackenzie Americas Polyester Conference in Houston on February 27 & 28. Register your interest here.