How should Cyprus' giant gas discoveries be commercialised?

Finding gas is the easy part. What now?

1 minute read

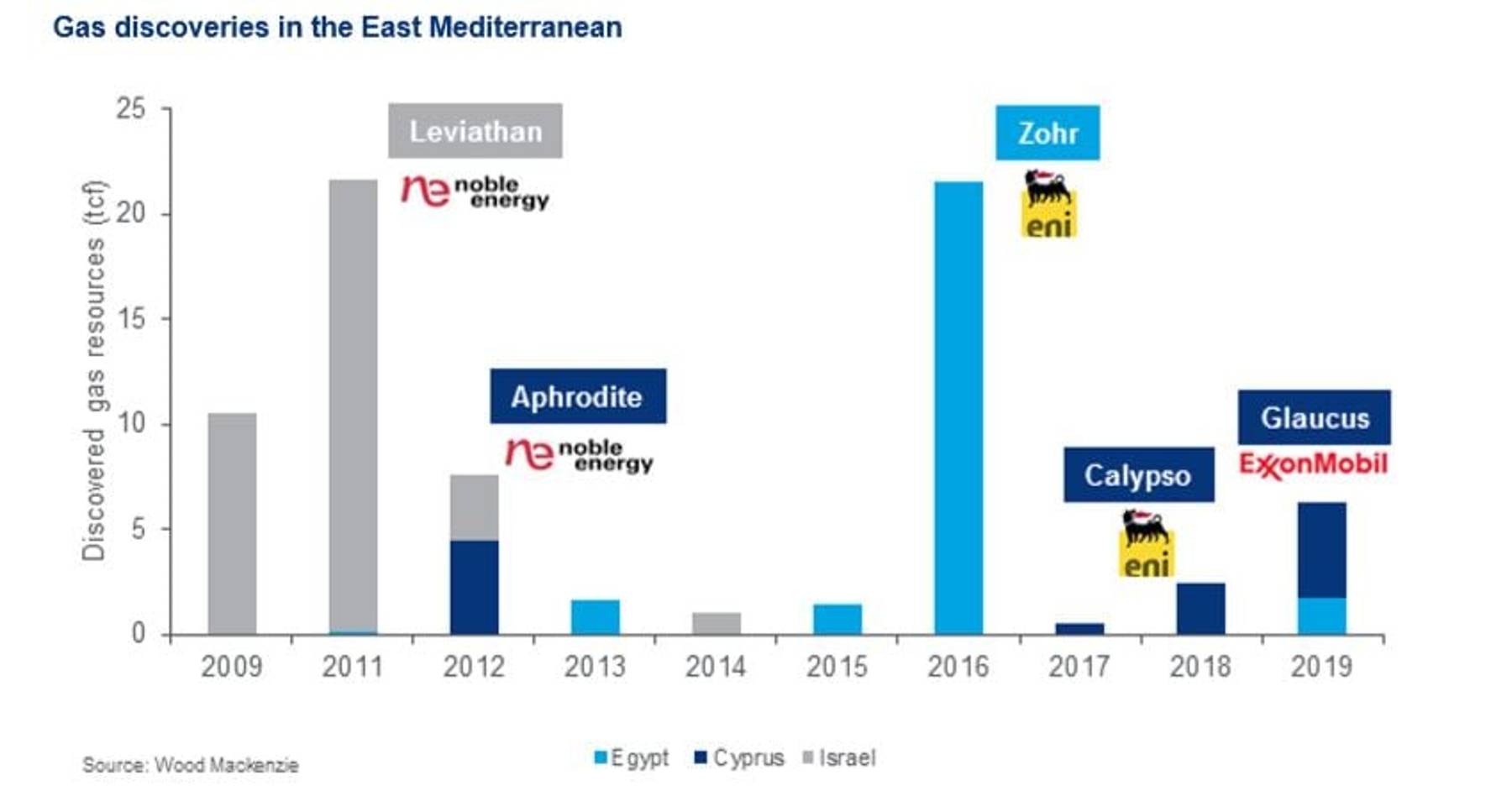

Cyprus has been a bright spot for exploration over the last seven years, with a string of giant gas discoveries including ExxonMobil’s Glaucus and Eni’s Calypso. In total, we estimate 11 tcf of recoverable gas resource has been discovered.

Finding gas appears to have been the easy part. Can these discoveries be commercialised?

The next 18 months will be critical in answering that question.

{kind=link}

There are four main routes to commercialisation: which do we think is the most viable?

Cyprus is a small market, not sizable enough to support a large project. There are four main options to consider.

Option 1: Pipeline to Egypt

Exporting gas via Egypt’s under-utilised LNG facilities is the most obvious solution. It offers the lowest cost with the fastest time to market and potentially the best netbacks. But Egypt has also seen big results from exploration with its own giant discoveries – the most notable of these is the Zohr field. How much capacity will be available to Cypriot resource-holders?

Get Malcolm's expert view on Egypt's gas market and infrastructure

Malcolm has assisted a number of international customers, including majors, NOCs and independents, with international growth strategies, unconventional gas studies and portfolio reviews. Talk to Malcolm about East Mediterranean energy markets.

For details on how your data is used and stored, see our Privacy Notice.

Malcolm Forbes-Cable, Vice President, Upstream Consulting and Supply Chain Lead

Option 2: Cyprus onshore LNG

This is a potentially compelling option, provided there is enough gas. A two-train LNG plant will need around 12-15 tcf of recoverable resource – at least three times the size of Glaucus.

Option 3: FLNG

FLNG is a smaller-scale solution that requires less gas than traditional onshore projects. It would do away with the need for collaboration – an advantage in big gas projects. However, questions remain about whether FLNG is cost-competitive.

Option 4: The EastMed pipeline

The EastMed pipeline has enjoyed government support and has garnered plenty of headlines. But we question its commerciality.

The next 18 months will be critical

All options are on the table. Much will depend on what else is discovered when ExxonMobil and Eni resume drilling next year. With two large Cyprus discoveries in the last two years, is there more where that came from?

Tension between Cyprus and Turkey could complicate matters. And if Egypt continues its successful exploration run, Cypriot resource-holders will need to jostle for position to access the country’s LNG facilities.

How will the next 18 months play out for Cyprus? With so much uncertainty, it pays to have objective insight. Find out more about our Upstream Service.