Can metals supply keep up with electric vehicle demand?

Battery raw materials could face supply crunch by mid-2020s

1 minute read

In every electric vehicle (EV) battery, there’s a complex chemistry of metals – cobalt, lithium, nickel and more. The electrification of transport is transforming the demand and supply of those battery raw materials.

In fact, we expect to see double-digit growth for battery raw materials over the next decade. And our latest research suggests they could face a supply crunch by the mid-2020s, increasing the pressure on the battery raw materials supply chain.

What does the long-term outlook for battery raw materials mean for electric vehicle penetration, the metals supply chain and those who invest in it?

Read the latest research from our Battery Raw Materials Service.

What's driving demand?

- Total passenger electric vehicle (EV) car sales, including hybrid electric vehicles (HEV), were up by over 24% last year

- Global electric car sales (with a plug) will account for 7% of all passenger car sales by 2025, 14% by 2030 and 38% by 2040

- Battery pack sizes continue to trend larger through the medium term

- NMC 811 cells are being produced on a greater scale resulting in increased nickel demand at the expense of cobalt and lithium

- Most automotive manufacturers plan to go completely electric by 2050

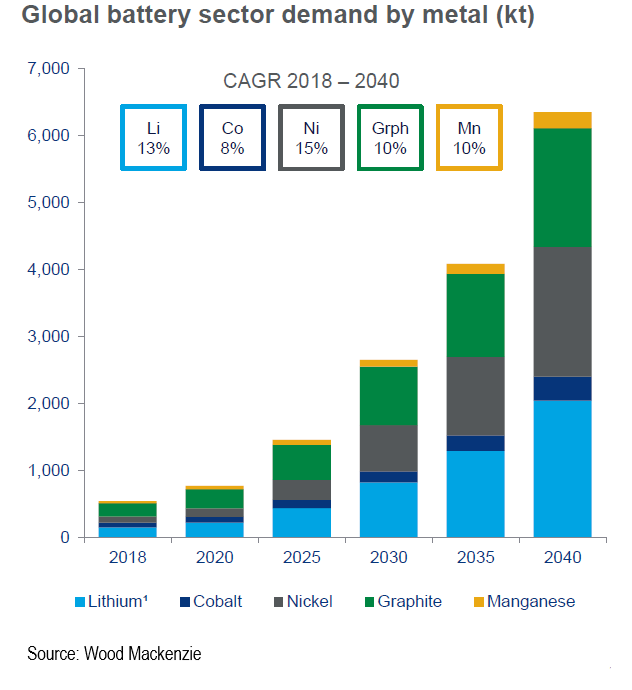

What’s the long-term outlook for battery raw materials?

We’ve raised our demand estimates since our H2 2018 report as a result of the factors above. Here’s our latest long-term outlook for lithium, cobalt, nickel, graphite and manganese.

Retreat in lithium prices underway

Spot prices for lithium carbonate have fallen by just under US$7,000/t since June 2018.

We are seeing the same weakness in the realised prices of the majors and their expectations for H1 2019. And this is in an environment where the major brine producers in South America have failed to ramp up capacity. Clearly, the first responders to the lithium boom – Australian hard rock mines – have the capability to quickly deliver the required tonnages.

Meanwhile, the bottleneck in Chinese conversion capacity that was supporting prices is giving way as China emerges as a net exporter of lithium chemicals to the region.

It has only taken a few years for the battery sector to become the largest demand driver for lithium. Lithium’s use in every lithium-ion battery type means it will have double-digit annual growth, making up over 80% of total lithium demand by 2030.

Cobalt prices have plummeted this year

Like lithium, cobalt prices have softened over H1 2019. The low prices may defer some mine projects and are likely to see reduced artisanal output from the DRC. However, the industry must still contend with an oversupply of intermediates until 2024. And the existence of swing supply in China is likely to keep a lid on any major price upside. Although cobalt looks challenging in the long-term, the adoption of high-nickel batteries in EVs means the emerging deficits look more achievable than previously expected.

Indonesia key for nickel

Although the battery sector share of nickel demand is much smaller than other metals, getting the quantity of nickel that EVs will need by the mid-2020s will be a challenge. A low nickel price has hindered any project development and with lead times often up to 10 years, investment needs to happen now.

While high-nickel ternary batteries will mean higher corresponding demand for nickel, like cobalt, our long-term deficits are becoming more feasible. Much of this is due to growing capacity in Indonesia, to serve both the stainless steel sector and emerging battery demand.

Business as usual for graphite

For graphite, there is little change in fundamentals. While the scale of demand is huge, we don’t expect any supply-side challenges in terms of natural graphite flake due to the growing supply out of East Africa. Synthetic graphite presents more of a challenge, given potential disruption to needle coke feedstock as a result of the new IMO 2020 regulations and growth in China’s steel sector.

Manganese central to NMC batteries

The manganese industry is overwhelmingly driven by the steel sector, something unlikely to change no matter how many EVs are on the road. While a steady supply of manganese sulphate will be crucial for NMC battery producers, we do not foresee any supply-side issues in this space.

What does this mean for investors in battery raw materials?

Despite strong growth in demand on the horizon, there’s not yet much for investors to get excited about. Meeting demand is not a challenge for key metals at present. In many cases supply is chasing demand. Increase electric vehicle penetration to 10% and above, and it is a different matter altogether. Are the current falling prices and weak sentiment setting the world up for a crunch down the road?

Unless battery technology can be developed, tested, commercialised, manufactured and integrated into EVs and their supply chains faster than ever before, it will be impossible for many EV targets and ICE (internal combustion engine) bans to be achieved – posing issues for current EV adoption rate projections.

Could battery raw materials face a supply crunch?

Stream our webinar to stay on top of the changing conversation as our analysts share key insights from our latest long-term outlook on battery raw materials.