IMO 2020 is about to get real

1 minute read

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin Thompson

Vice Chairman, Energy – Europe, Middle East & Africa

Gavin oversees our Europe, Middle East and Africa research.

Latest articles by Gavin

-

The Edge

Is Europe’s gas market inching towards a winter crisis?

-

Opinion

Is Nigeria’s deepwater roaring back?

-

Opinion

Why US Henry Hub natural gas prices are set to rise | Webinar replay

-

The Edge

Will falling populations reshape energy demand?

-

The Edge

Has the oil price bubble burst?

-

The Edge

Is Argentina’s giant shale play the next Midland Basin?

As I write this edition of the APAC Energy Buzz from my desk in Singapore I can see ships. Lots of ships. No surprise given that Singapore is amongst the largest and most important bunkering ports in the world, but it does help focus the mind on the scale of the sector and, as we approach January 1 2020, the impending impact of new International Maritime Organisation (IMO) fuel oil sulphur limits for global shipping.

Beginning in just under one month, the IMO requires all ships to switch to marine fuels with a sulphur content no greater than 0.5 wt% from the current limit of 3.5 wt% to reduce levels of atmospheric sulphur oxide emissions. To comply, shippers have options to switch to marine gasoil (MGO) or very low sulphur fuel oil (VLSFO), to continue using high sulphur fuel oil (HSFO) for vessels retrofitted with on-board scrubbers or to use to LNG as a bunker fuel.

IMO 2020 has been some time coming. The IMO’s MARPOL policies to tackle maritime air pollution date back to the 1990s, and IMO 2020 itself was announced in October 2016. At Wood Mackenzie, we’ve produced deep analysis on how IMO 2020 will affect crude suppliers, traders, refiners and end-user prices, as well as shippers. But with less than one month to go, it’s the immediate impact of IMO 2020 on Asia that’s been on my mind and so I sat down with my colleague Sushant Gupta, research director for oils to discuss.

Are shippers fully prepared for IMO 2020?

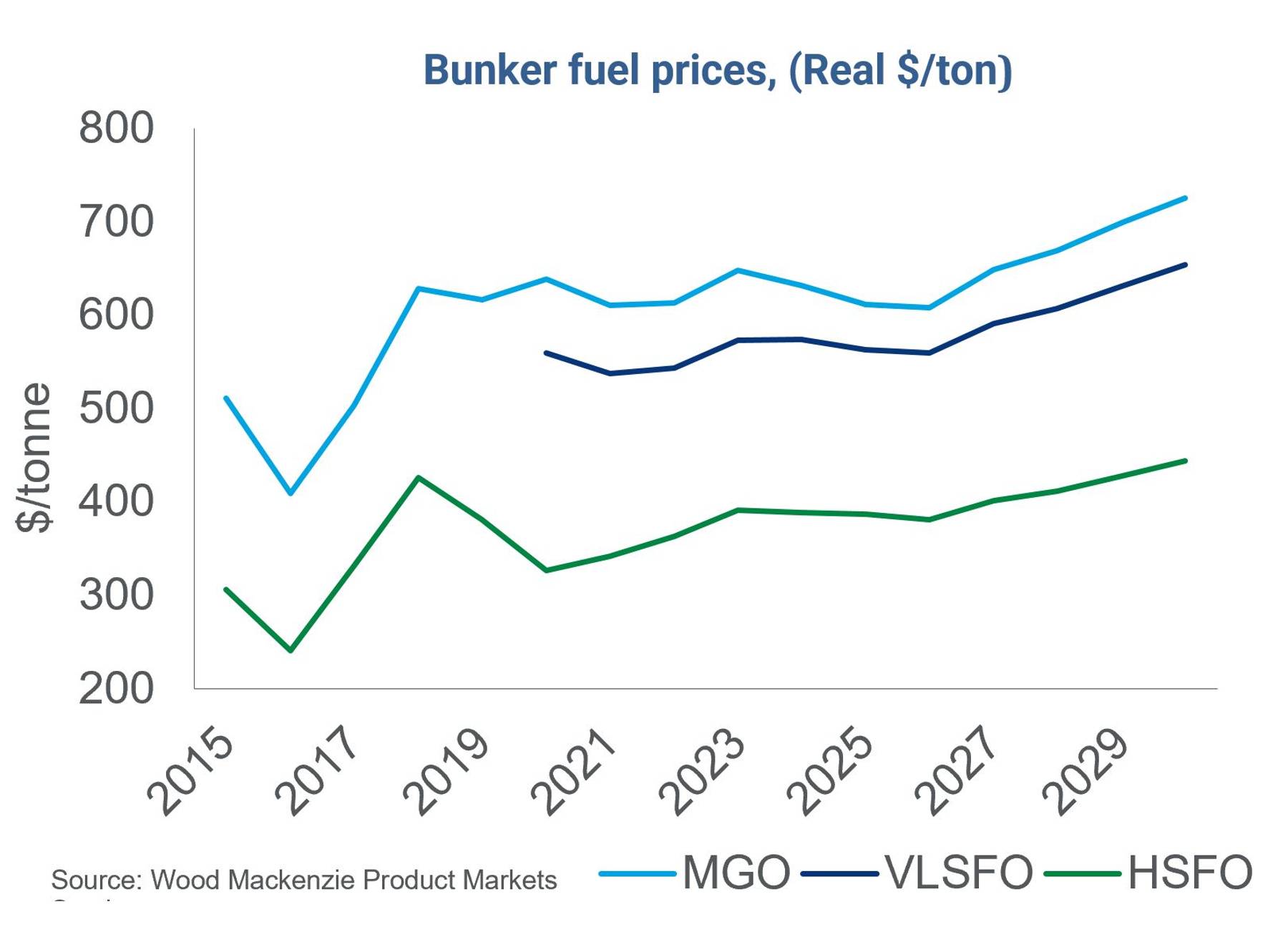

It’s only been over the past eight to nine months that shippers have been getting serious, and the quick-fix option of installing scrubbers remains relatively limited. As the chart below highlights, the number of vessels with scrubbers installed in 2020 will account for only around 15% of marine fuel demand.

Globally, shipping currently consumes around 3.5 million barrels per day (b/d) of high sulphur fuel oil. Come January 2020, we expect this demand to fall to around 1.3 million b/d, with a roughly 50:50 split between scrubbed and unscrubbed HSFO demand. Unscrubbed HSFO demand falls to zero over the coming years as more scrubbers are deployed. Demand for MGO (similar to diesel) will jump by around 1 million b/d in 2020 and then remain fairly flat at around 2.4 million b/d through the mid-term.

An interesting point on scrubbers is while they may provide a “sugar rush” for shippers looking to continue using HSFO, should the IMO in future turn attention to NOX and CO2 emissions then scrubbers will be of less value (though MGO would also face CO2 emission challenges - a potential win for LNG as a bunker fuel).

Can we expect full compliance on January 1, 2020?

No. Full compliance is going to be challenging, particularly in the early days of IMO 2020. Globally, compliance will likely be lowest here in Asia, with some ports better prepared than others (we can expect full compliance in Singapore, as well as at ports in Japan and South Korea for example). This is unlikely to be the case across the region however and some ports could see IMO 2020 as an opportunity to boost market share. Some shippers may also want to take advantage of a wider HSFO price discount to increase competitiveness through non-compliance (but not for long).

There are also technical and operational issues that will impact immediate compliance. For example, a ship will not have to detour if compatible fuels aren’t available at a destination port. Safety concerns regarding the compatibility of new blends of VLSFO could be a valid ground for an exemption. And if a ship already has scrubbers on order (and can verify this) then there is a likelihood of an exemption. But by March 2020 the IMO’s Carriage Ban will prohibit all vessels without scrubbers from carrying 3.5% HSFO in their bunker tanks, leading to stricter compliance.

So what level of compliance might we realistically see in Asia from early 2020? Sushant reckons something like 80-85% compliance is probably realistic, to begin with. But this is set to improve, and quickly.

What does IMO 2020 mean for refiners in Asia Pacific?

Globally we believe that refiners can deliver something like 1.4 million b/d of <0.5% VLSFO next year. To achieve this, refiners will maximise the production of VLSFO – either by segregation of intermediate product streams or by segregation of crudes and running their crude units in batch mode. To supply the 1 million b/d of additional MGO for shipping, refiners will need to run an additional 1.7 million b/d of crude to meet this higher gasoil demand.

This inevitably affects prices and margins for both crude feedstocks and refined products. Recent price volatility following the September 14 attacks in Saudi Arabia has blurred the impending impact of IMO 2020 to some extent, but I think we can expect widening differentials between both sour and sweet crudes and diesel and fuel oil through December and into 2020. Good news for complex refineries in the region operated by the likes of Sinopec, PetroChina and Reliance which can take discounted sour crudes and produce transportation fuels. Those refiners capable of processing more heavy and sour crudes will also benefit from the additional heavy feedstock freed up from the HSFO bunker market.

{kind=link}

{kind=link}

Is LNG a beneficiary of IMO 2020?

It all depends on your perspective. In the long run, LNG sellers will benefit from the IMO regulation on marine fuels as it drives a 23% annualised growth in demand for LNG in marine bunkering, reaching 22 million tonnes per annum by 2030. But that’s some time off; in the short-term buyers in Asia stand to benefit given the majority of their contracted LNG is indexed to the Japanese Crude Cocktail (JCC), a mix of medium and sour crudes. An increasing differential for sour crudes to Brent will make JCC-indexed LNG cheaper and reduce margins for LNG sellers, with Japanese buyers set to benefit the most from JCC’s devaluation to Brent.

So as we head into the new year I expect IMO 2020 will have a material impact on Asian shipping and fuel supply. While this might not be immediate as in other regions, the move towards near-full compliance will happen relatively fast. With reducing atmospheric sulphur oxide emissions the current target, I wonder where the IMO may focus next?

APAC Energy Buzz is a monthly blog by Asia Pacific Vice Chair, Gavin Thompson. In his blog, Gavin shares the sights and sounds of what’s trending in the region and what’s weighing on business leaders’ minds.