A red-hot Australian M&A market

The Australian M&A market is bubbling over, but what are they key drivers?

3 minute read

Angus Rodger

Vice President, SME Upstream APAC & Middle East

Angus Rodger

Vice President, SME Upstream APAC & Middle East

Angus leads our benchmark analysis of global Pre-FID delays, and deep water developments.

Latest articles by Angus

-

Opinion

Southeast Asia faces its deepwater gas 2.0 moment

-

Featured

Upstream-oil-gas-2026-outlook

-

Opinion

Can Andaman Sea resources avert Thailand’s gas crisis/crunch?

-

The Edge

Why upstream companies might break their capital discipline rules

-

Featured

Upstream oil & gas regions 2025 outlook

-

Opinion

How to make upstream licensing work

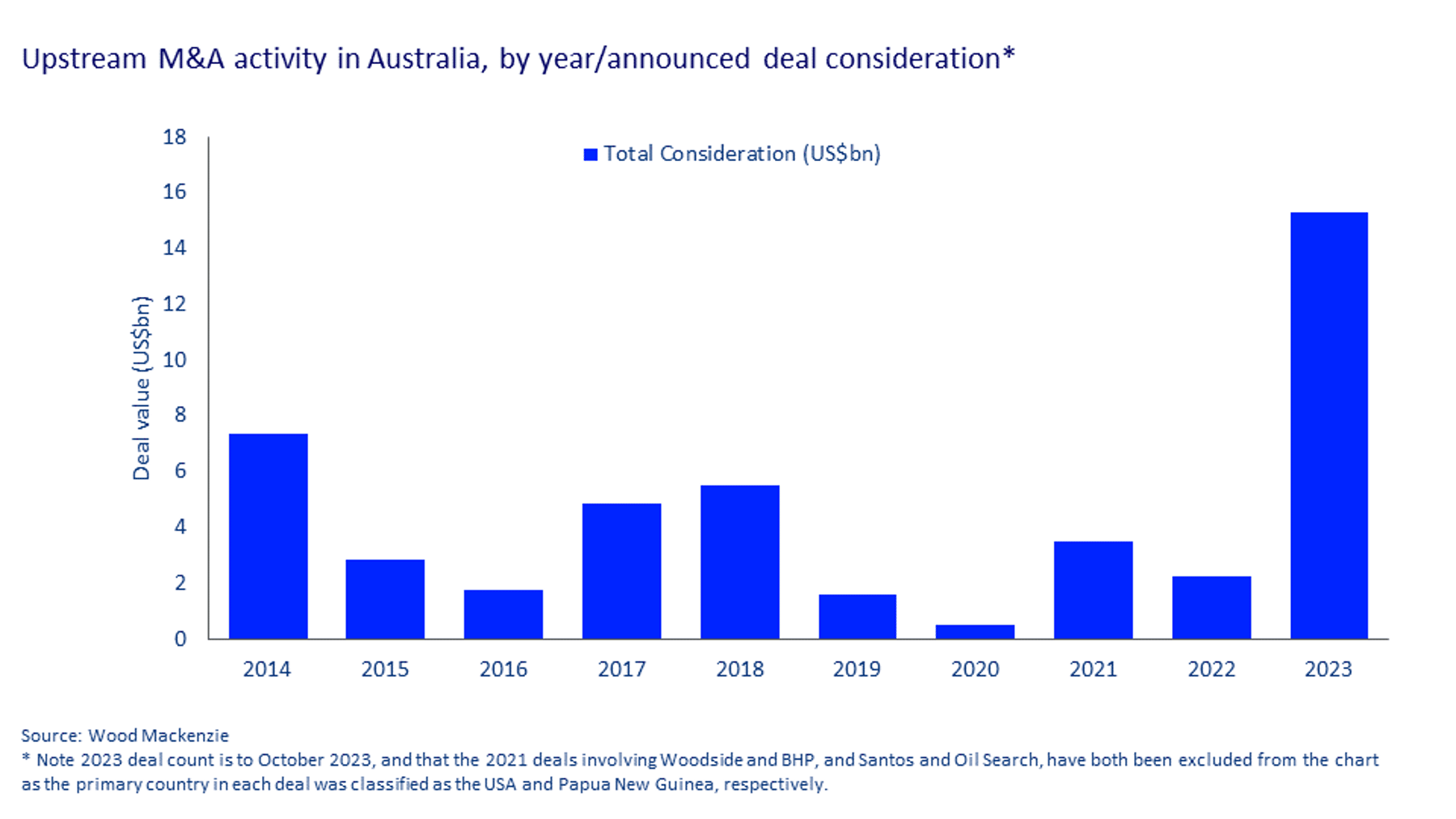

Our latest insight dedicated to Australian E&P companies highlights how 2023 has been a standout year for merger and acquisition (M&A) deals, despite a background of regulatory instability.

The last 12 months have generated the most unstable legal and fiscal landscape seen in Australia for over a decade, but it hasn’t stopped 2023 from delivering a record volume of upstream M&A.

By October, we had seen over US$15bn spent on upstream transactions. For context, that is more spent than in all of the Australia-focused deals of the previous five years combined.

What makes this particularly interesting is the tumultuous background conditions. Normally when the risk index starts ticking upwards, it puts a brake on M&A activity. However, we have seen the opposite happening in Australia this year, where despite the conditions, the M&A market is bubbling over.

Recent M&A activity in Australia

We have witnessed PE-players EIG and Brookfield swoop for Origin Energy, and a bidding war in Perth for Warrego Energy that was eventually won by mining giant, Hancock Energy. Taiwanese firm CPC also bought a chunk of Dorado (its first deal in a decade) and BP acquired Shell’s interest in the mammoth Browse development.

{kind=link}

Most Australian deals focused on LNG and domestic gas, such as ConocoPhillips buying an additional stake in APLNG, and Saudi Aramco acquiring an interest in EIG vehicle, MidOcean Energy. We believe more are on the way. It is also interesting to note that Aramco made its first move towards becoming a global LNG player in an Australia-focused deal.

The activity also supports the argument that despite the political headlines, Australia remains a top-tier investment destination. This message has also come through consistently in our discussions with bankers and the companies involved in these deals. For investors, Australia may be slightly less attractive than it used to be, but it is still far less risky than most other countries on their radar.

Another notable example of this is the recent Japanese transactions. While Tokyo has been unusually vocal regarding the Australian government’s regulatory changes, it did not stop two back-to-back upstream deals in August.

Firstly, LNG Japan (a 50/50 Sojitz and Sumitomo joint venture) took a 10% share in Woodside’s Scarborough gas project for US$500 million. This was followed by TotalEnergies and Japan’s INPEX acquiring PTTEP’s 100% interest in the 3 tcf Cash/Maple fields, which will likely be tied back to the Ichthys field.

Anticipated deal landscape and potential challenges

We also see more deals on the way, featuring companies of all sizes and assets in basins from across the country. We expect operators to target equity sell-downs of some key assets, such as Scarborough, Crux, Narrabri and Dorado. Alongside that we expect non-core and mature assets offshore WA to come up for sale, and M&A activity in the Perth basin to continue.

The picture is not entirely rosy. The stage is set for further government intervention in domestic gas markets. We will cover this in more detail in the next part of this series, which is focused on opportunities and challenges in the Australian upstream sector. We are also seeing ongoing delays and confusion around securing approvals for federal offshore environmental plans, which is affecting every aspect of offshore operations.

Nonetheless, with world-class LNG assets and gas prices rising in both the east and west coast gas markets, the country’s rich opportunity set looks likely to continue to spark interest.

Australia’s need for new gas investment has never been more urgent, but navigating the environmental, legal, regulatory, and fiscal landscape has never been more challenging or unpredictable.

In part 2 of the series, we explore “Market outlook - opportunities for East coast gas.”

Australia & Oceania independent upstream solutions

Find out more about how we are helping the exploration and production sector in Australia and Oceania navigate current upstream challenges and opportunities.

Find out more