Refinery-petrochemical integration disrupts gas-based cracker feedstock advantage

Gas-based feedstocks are the traditional investment driver for steam cracker investments, but with feedstock availability becoming more challenging the economics are under scrutiny

4 minute read

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan Gelder

SVP Refining, Chemicals & Oil Markets

Alan is responsible for formulating our research outlook and cross-sector perspectives on the global downstream sector.

Latest articles by Alan

-

Opinion

The Hormuz shock: what the data reveals about global oil markets in 2026

-

The Edge

Has the oil price bubble burst?

-

Opinion

Horizons Live: Strait talking | Webinar replay

-

The Edge

How quickly can Gulf oil exports recover?

-

The Edge

UAE’s exit rattles OPEC’s grip on the oil market

-

The Edge

Ceasefire in the Middle East

The traditional investment thesis for steam cracking has mainly focused on securing advantaged, low-cost gas-based feedstock to secure a first-quartile competitive position. However, feedstock availability is becoming more challenging and integrated refinery-petrochemical sites – prevalent in Europe and Asia and emerging in the Middle East – could offer a viable alternative.

This article explores the drivers of competitive position – and why the volatility of the refining sector demands regular, site-specific assessments to support capital investment decisions.

To dig even deeper into this topic, fill in the form to access a case study on Shell’s Pulau Bukom refinery and its preparations for the energy transition.

Gas-based feedstocks offer a competitive advantage

Ethylene can be produced from a variety of routes and feedstocks. Steam cracking remains the dominant source of supply, with lighter feedstocks offering higher selectivity to ethylene and lower operating costs. Gas-based feedstocks, such as ethane, represent the lowest cost option. Prices are either regulated low in the Middle East or are closely linked to the cost of natural gas (by extraction economics) in North America. Ethane also has the highest selectivity to ethylene.

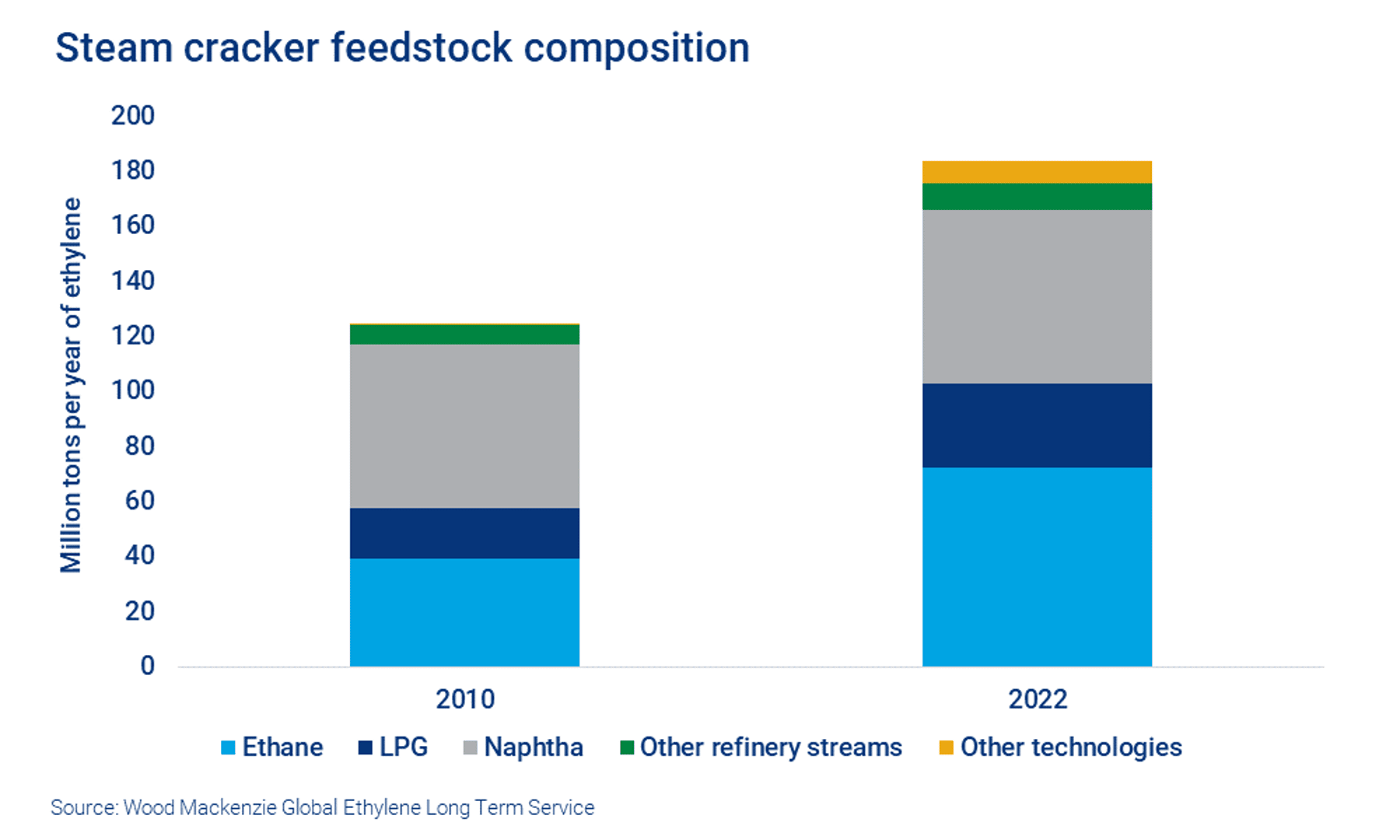

This powerful combination has resulted in ethane-based steam cracking growth far outpacing the growth in overall steam cracking capacity since 2010.

In fact, ethane and LPG based crackers are largely responsible for the growth in steam cracking capacity over this period. This feedstock, which is both low cost and more selective to ethylene, provides an advantaged cost of production when compared to naphtha-based crackers.

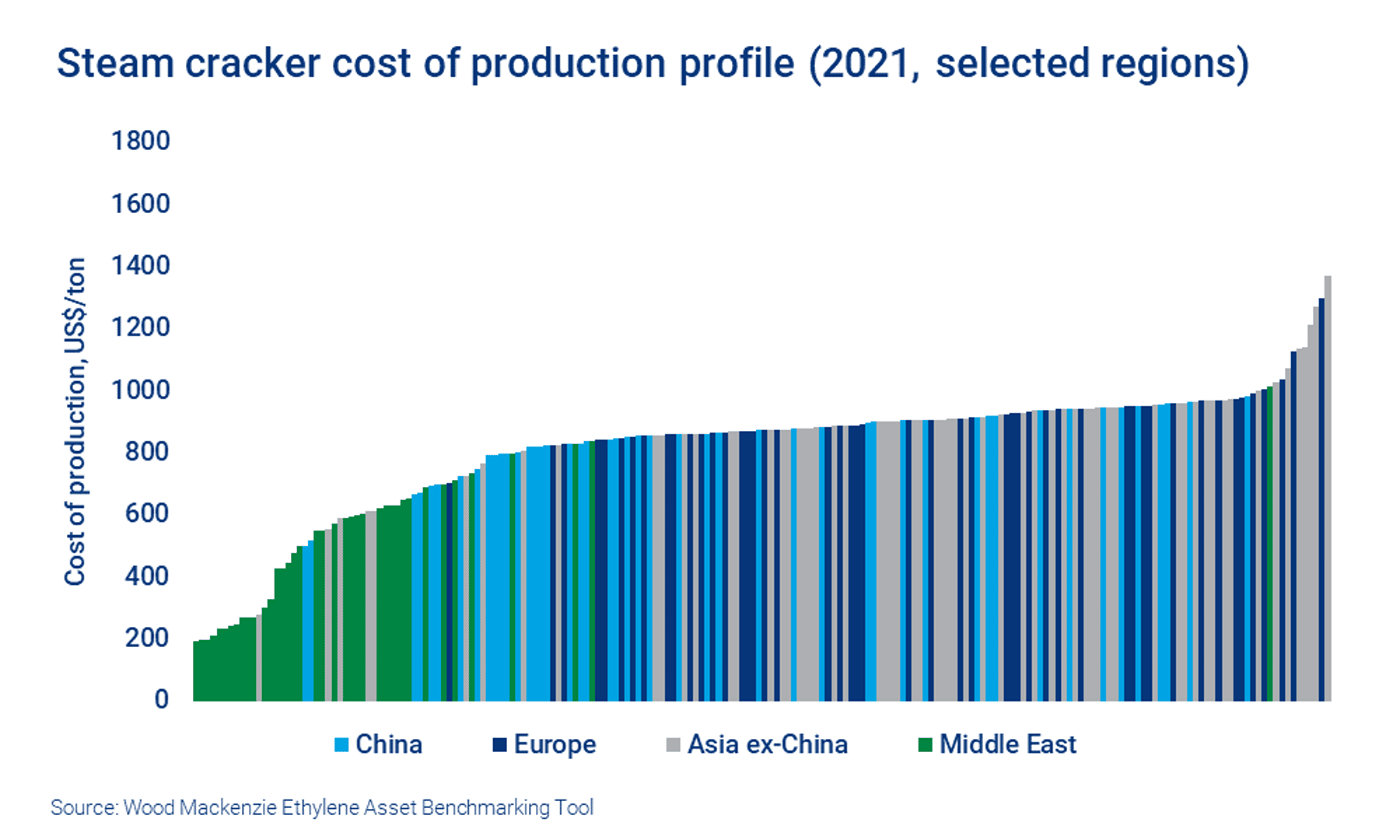

Recent history has been tumultuous to say the least with the global pandemic in 2020 and Russia’s invasion of Ukraine in 2022. On that basis, 2021 may be a more typical market landscape to assess competitive dynamics as the global economy recovered from the pandemic. The chart below shows the 2021 cost of production advantage for Middle East sites when compared to other regions. Steam crackers in Europe and Asia (excluding China), which are primarily naphtha-fed form the high-cost part of the curve, so will be the facilities that achieve poor margins as their economic fundamentals set the regional ethylene price.

To date, the market signal has been clear: gas-based feedstocks are key drivers of competitive advantage. This has driven significant capital expenditure over recent years, but the US and Middle East gas-based investment wave is now largely complete.

For the Middle East, the challenge is one of feedstock availability, with only Qatar’s growing exports of LNG likely to provide sufficient gas-based feedstock for further ethylene capacity additions. The lack of gas-based feedstock is forcing Middle East producers to look at alternatives and follow the path established by Europe and Asia, which largely relies on liquids and so develop integrated refinery-petrochemical facilities.

Refinery-petrochemical integration offers a viable alternative

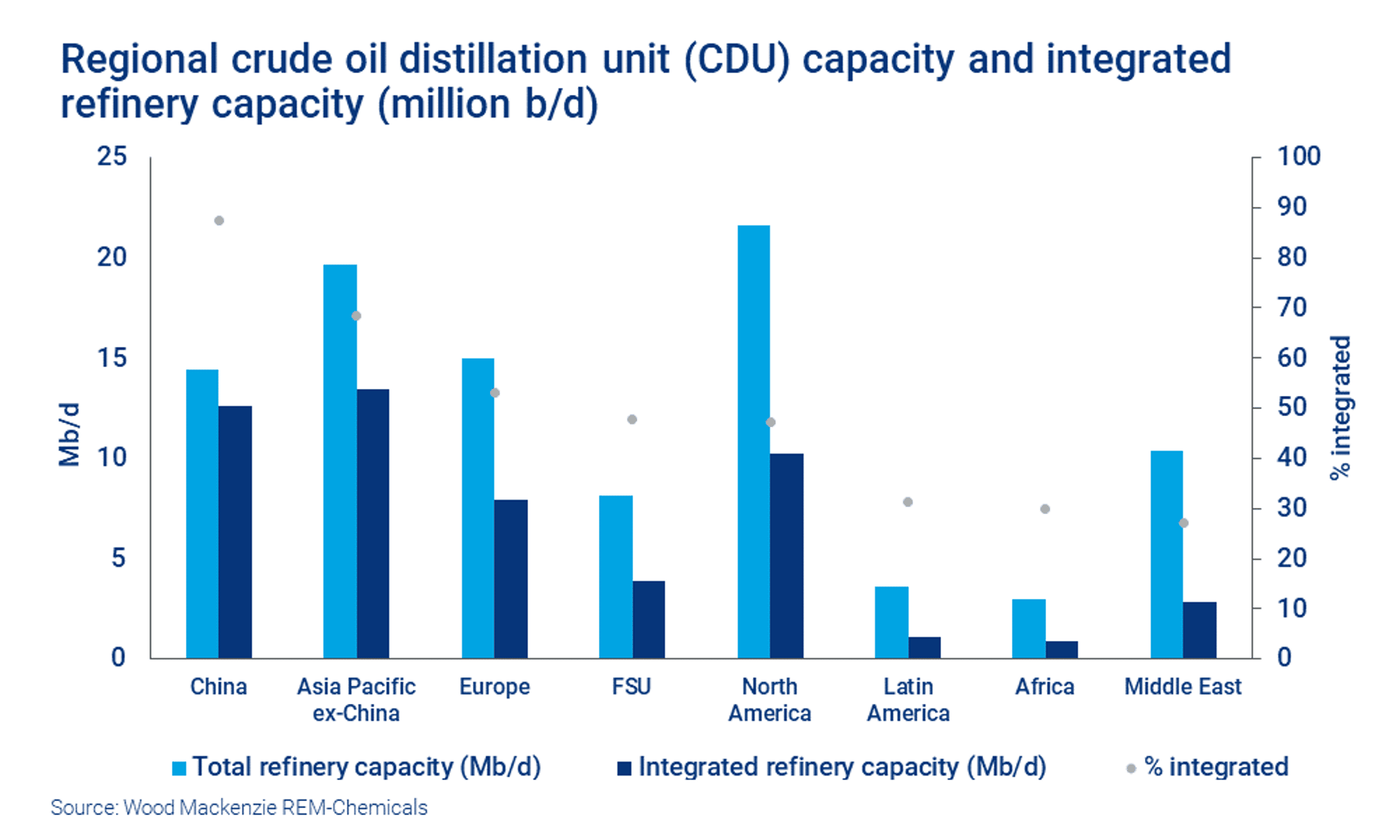

Asian refining capacity has grown tremendously this century, but very few stand-alone refineries have been built. The region’s growing demand for both transport fuels and petrochemicals has resulted in Asia leading the world in terms of integrated refining capacity.

These integrated refinery-petrochemical facilities are well positioned for the energy transition and the associated mega-trend of declining future demand for transportation fuels while petrochemical demand continues to grow. The integration lowers the costs of adaption to the changing demand profile compared to stand-alone refinery and petrochemical sites.

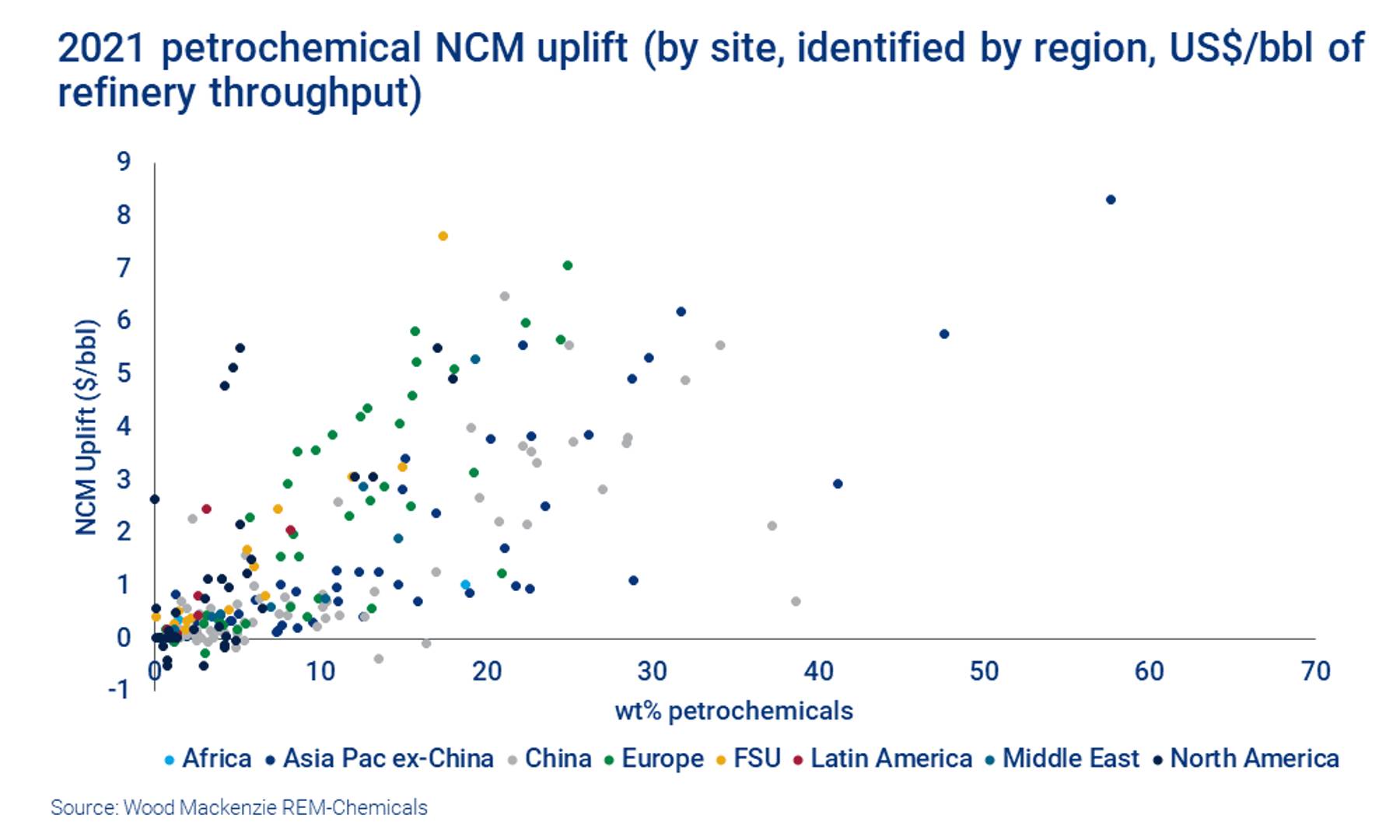

There is value in producing petrochemicals. In 2021, the value uplift from petrochemicals was material to the refinery net cash margin (NCM) on a US$/bbl of crude basis (assessed against fuels-only refineries). The chart below, which draws on our REM-Chemicals benchmarking service, shows that integrated sites in Europe benefited strongly due to the differing net trade positions of petrochemicals relative to transport fuels. This also shows the general trend of improving NCM uplift with growing yield of petrochemicals.

In 2021, petrochemical-integrated refinery sites enjoyed high utilisation rates and strong profits. Refineries didn’t need support in 2022 as pandemic demand recovery and fears of supply loss from the Russia/Ukraine conflict changed global crude and product trade flows, delivering unprecedented refining margins. However, China’s lockdowns and petrochemical capacity additions resulted in weaker petrochemical margins, particularly in the second half of the year when the global economic growth was stalling.

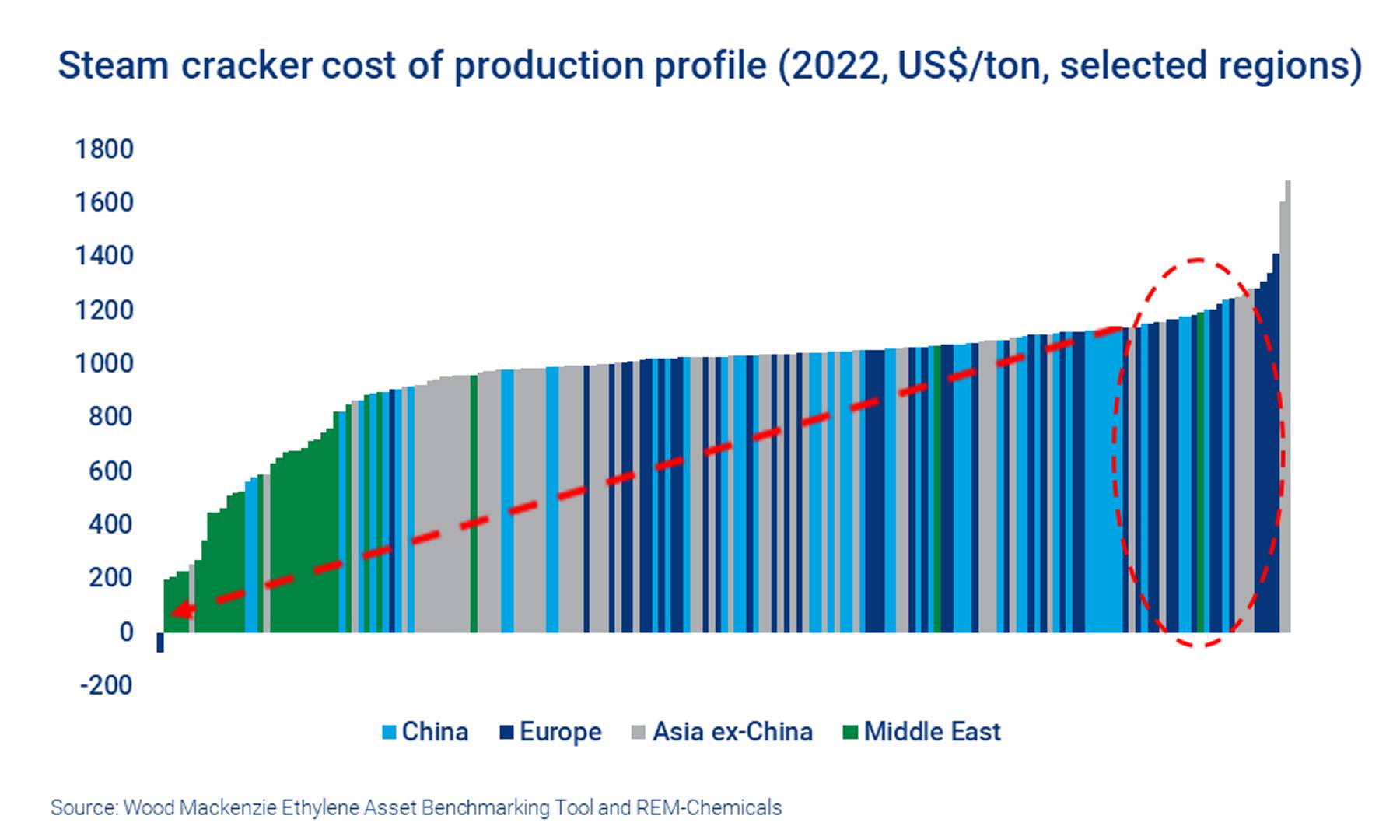

Even in this market environment, integrated complexes were competitively advantaged, but this derived from strong refining margins. The chart below shows the cost for 2022 of production profile for the same cohort of steam crackers. 2022 was far less profitable for naphtha-based steam cracking, however, particularly in Asia, as overcapacity limited utilisation and reduced margins. The chart also shows the impact of integration on a third-quartile European site.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

In addition, the cost of production methodology remained unchanged, but the high refining margin resulted in co-product credits exceeding feedstock costs. So, the effective cost of production for ethylene from that site was negative in 2022. The integrated sites achieved high utilisations despite the weakness in chemical margins.

We recognise that this is a novel approach for the petrochemical sector to reconsider its cost of production analysis, as it often excludes the impact from refining. It does, however, highlight how refinery-integrated petrochemicals became inconvenient by-products of the strong refining margin environment during 2022 and reflects the strong market incentive for refiners to maximise throughputs during that period.

Wood Mackenzie is certainly hoping for a less tumultuous period over the next few years. Refining margins are expected to ease as new refining capacity is commissioned and Asian cracker margins strengthen as demand recovers. Refining margins, however, are projected to remain healthy.

This market environment is more balanced across refining and petrochemicals than recent years, so the drivers of competitive position become more nuanced and site-specific. As such, we consider it essential for business intelligence teams to understand and establish the behaviours of integrated refinery sites, both individually and as a cohort, to assess the implications on their asset utilisation and overall business performance.

Interested in the refineries of the future?

Fill in the form at the top of the page to access a case study on the reconfiguration of Shell’s Pulau Bukom refinery.

Want to benchmark integrated refinery-petrochemical assets and empower your decision-making?

Get a REM-Chemicals demo