Sodium-ion batteries: disrupt and conquer?

The sodium-ion battery market looks set to reach GWh-scale production levels this year

3 minute read

Contemporary Amperex Technology Co Ltd (CATL) sparked the interest of the battery industry in July 2021 when it unveiled its first-generation sodium-ion (Na-ion) cells. The breakthrough technology promised an efficient alternative to lithium iron phosphate (LFP).

Several other cell manufacturers have joined CATL in establishing a Na-ion supply chain, ready to mass-produce cells this year. The dramatic rise in lithium and other battery raw material prices over the last two years has only accelerated interest.

So, how much market disruption do we expect? Could lower pack costs spark widespread substitution of Na-ion into Li-ion applications? Where are the key market opportunities? And can Na-ion production scale quickly to meet demand?

In Sodium-ion update: a make-or-break year for the battery market disruptor, we drew on insight from our Electric Vehicle and Battery Supply Chain Service to explore the outlook for the Na-ion market.

Fill in the form for a complimentary extract and read on for an introduction.

Na-ion versus Li-ion: cell capabilities

Nickel-based chemistries are in a league of their own in terms of storing energy, which is why they dominate the EV market. However, they lack the cycle life that LFP and Na-ion can achieve. LFP has a lower cell energy density, but the use of cell-to-pack architectures brings LFP pack energy density much closer to that of nickel-based packs.

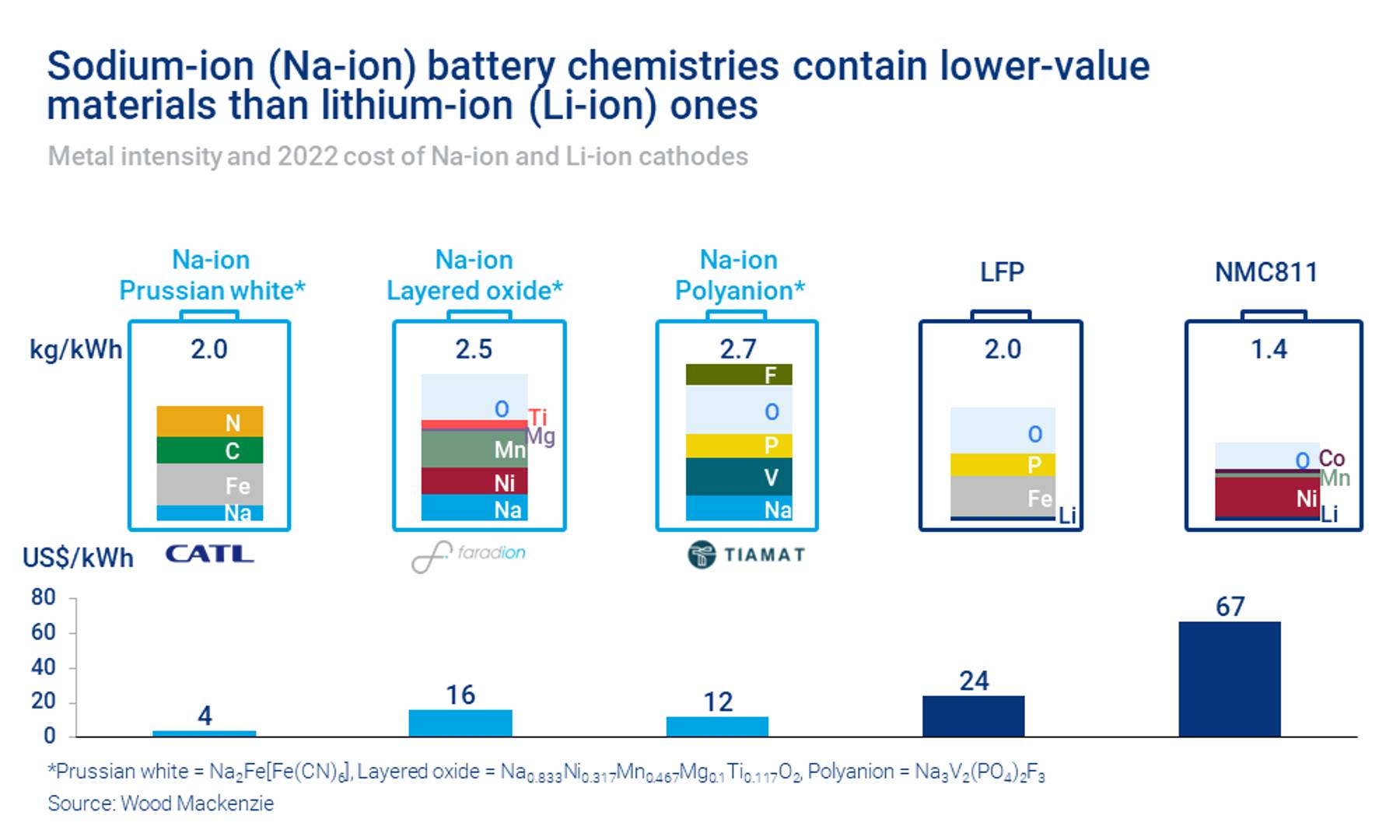

The attraction of Na-ion lies in its composition rather than its performance. Despite being heavier per kWh of storage capacity, Na-ion chemistries contain lower-value materials than Li-ion ones.

The three main Na-ion cathode types – Prussian white, layered oxide and polyanion – each use lower-cost materials than Li-ion cathodes. Prussian white’s bulky structure leads to a low energy density, but high power capability. Layered oxide and polyanion cathodes promise higher energies, but are more difficult to reach.

Despite their lower energy density and cycle life, Na-ion batteries are safer and perform better in a wide operational temperature range. They work on a similar principle to Li-ion cells and are expected to be at least 20% cheaper than LFP due to the fact that they are lithium-free.

However, greater cell and pack material costs could result in Na-ion being more costly.

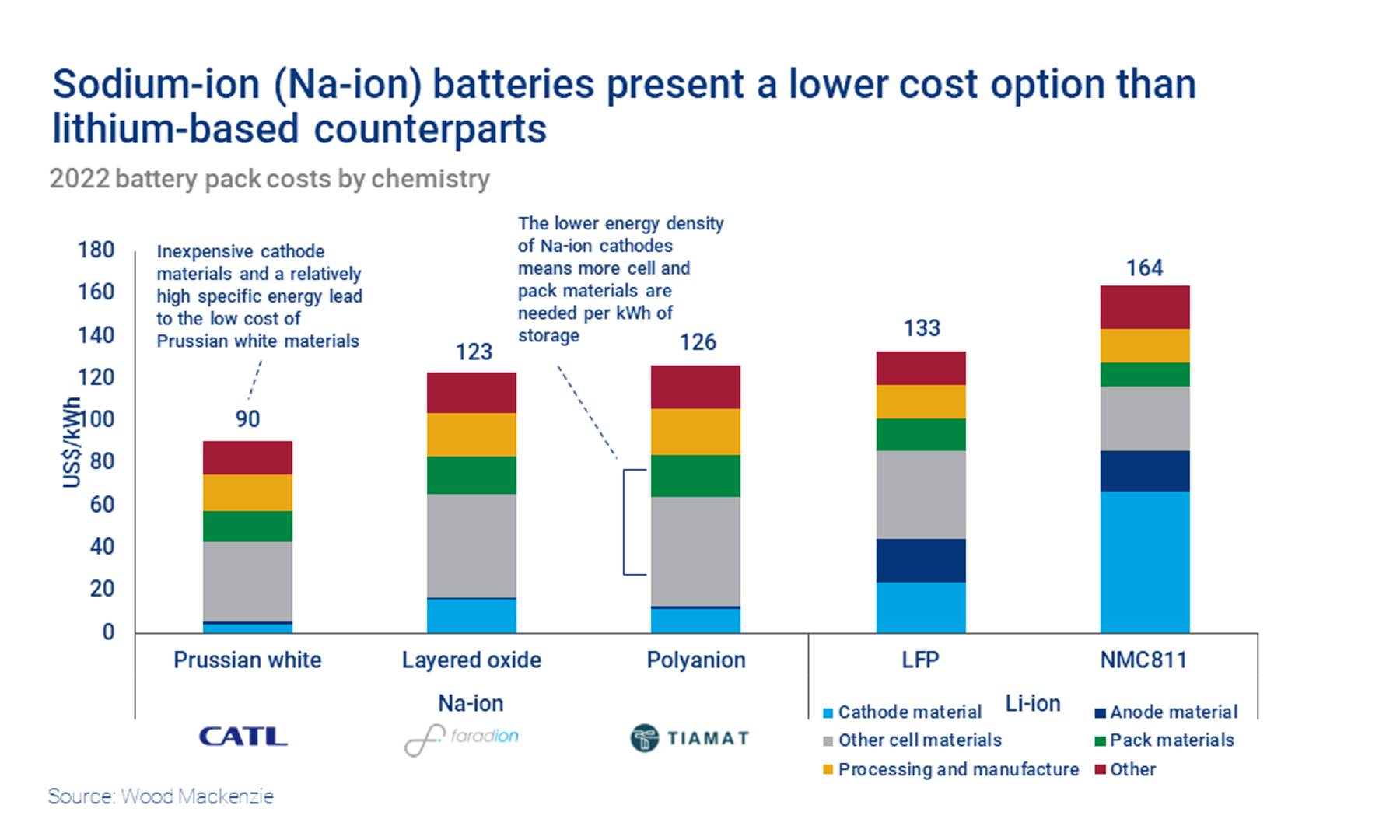

Cost comparison between Na-ion and Li-ion packs

Raw materials play a key part not only in the performance of the batteries, but also in terms of costs. In LFP cells, for example, materials account for 30% of battery pack prices.

Na-ion cells are likely to be less sensitive to rising lithium, cobalt and nickel costs. If all material prices grew 10%, Na-ion material costs would only increase 0.8%. LFP costs would rise 3.2%.

The lower pack cost of a Na-ion battery will be a leading reason to substitute Na-ion batteries for Li-ion applications. Na-ion manufacturing uses the same processes used in Li-ion gigafactories, so production capacity could scale up quickly.

{kind=link}

{kind=link}

Potential market opportunities for Na-ion batteries

The energy storage system (ESS) market presents one of the best opportunities for Na-ion demand. Greater safety and a longer lifetime make Na-ion prime for the stationary storage sector, especially with requirements for daily or hourly charge/discharge cycles and less stringent requirements for low mass and volume units.

Na-ion-based electric vehicles (EVs) would lack the range of their Li-ion counterparts, though, exacerbated by their additional weight. This makes the emerging two- and three-wheeler markets with low range and regular charging better suited to Na-ion technology, while Na-ion’s high power capability could be more appropriate for heavy-duty applications.

Importantly, Na-ion is a drop-in technology to Li-ion current production lines. Gigafactories can be retrofitted to produce Na-ion cells relatively quickly.

The Na-ion market outlook

We forecast just under 40 GWh of base case Na-ion cell production capacity by 2030. A further 100 GWh of production capacity is possible if Na-ion cells see success by 2025.

Which producers have committed to large-scale Na-ion production? How established is the supply chain? What are the bull and bear scenarios for demand?

Get our view in the full report. Fill in the form at the top of the page for a complimentary extract.